The global market for imported ferrous scrap exhibited a mixed trend in offers this week. In South Asia, offers saw an increase of up to 2-3% across markets, driven by sellers maintaining a firm stance amid higher collection costs and active purchases from the Turkish scrap market.

However, from a demand perspective, Indian and Pakistani buyers remained subdued due to the availability of better alternatives in the domestic market, coupled with sluggish sentiment in the finished steel market exacerbated during the Ramadan period. Meanwhile, Bangladeshi buyers were relatively more active showing preference for containerised scraps over bulk due to issues related to unavailability of Letters of Credit (LC) for imports.

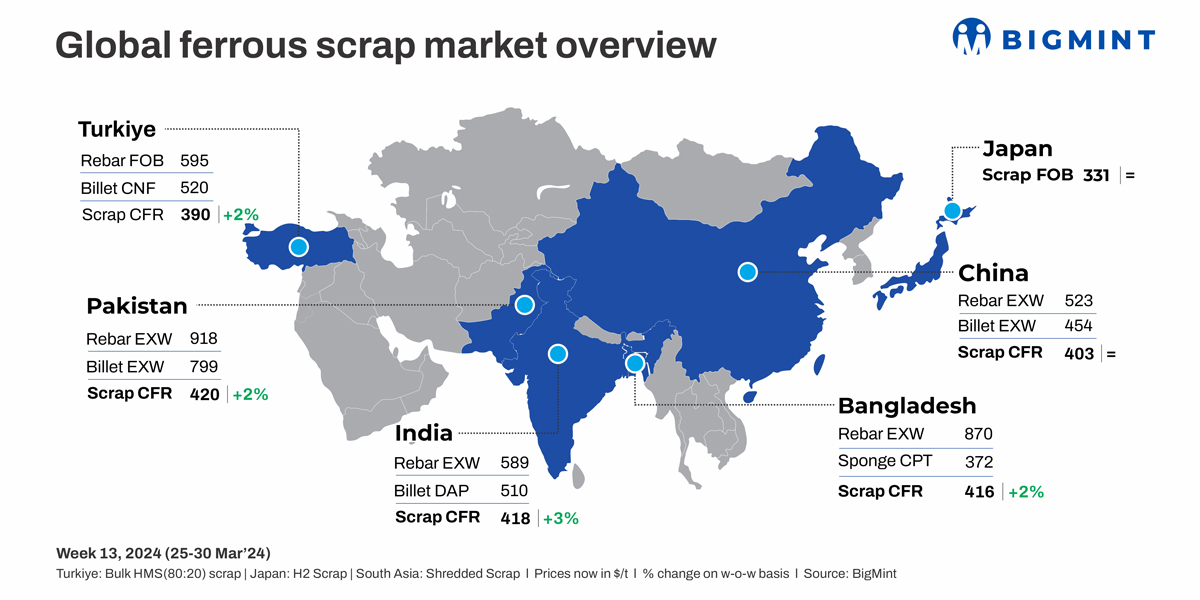

Japanese H2 scrap export offers remained unchanged for the second consecutive week, reflecting weak regional demand. China’s Shagang Steel reduced its scrap procurement price by $7/tonne (t) for the sixth time in a month.

Turkiye: Turkish steelmakers resumed deep-sea scrap market activity last week, aiming for late-April shipments. Approximately five additional cargo bookings were expected for April shipments. Prices have remained firm so far over last one week, with seven to eight deals being concluded from Europe, the US, and the Baltic region at a price range of $384-389/t CFR Turkiye. US-origin HMS (80:20) bulk scrap stood at $390/t CFR, up $9/t w-o-w, while US East Coast bulk HMS (80:20) was at $367/t FOB, up $11/t w-o-w.

Benelux scrap export prices saw a slight uptick, reflecting a stronger Turkish scrap market. Despite target levels reaching $400/t CFR, recent trades were settled at around $390/t CFR due to resistance from Turkish mills. Short-sea scrap market sentiment was bullish, with Balkan-origin HMS (80:20) targeting $370/t CFR. Turkish rebar export offers stood at $595/t FOB, with the scrap-to-rebar spread narrowing to $205/t FOB as compared to $213/t last week.

India: Indian buyers exhibited minimal interest in purchasing fresh scrap from the international market due to bid-offer disparities as well as the availability of more cost-effective domestic alternatives such as local scrap and sponge iron. Moreover, with the week-long holiday during the Holi festival, key participants were in a holiday mood, further dampening market activity.

On a weekly average, shredded scrap offers from Europe and the US were at $416/t CFR and $408/t CFR, marking an increase of $9/t and $7/t respectively. Additionally, HMS (80:20) scrap offers saw a marginal uptick of $10/t to $398/t CFR this week. The rise in offers was due to the firm stance taken by suppliers due to higher collection costs and active buying from Turkiye, the top scrap importer.

Throughout the week, approximately 1,200-1,300 t of shredded scrap were bought from the US within a price range of $405-408/t CFR. Around 1,000 t of HMS (80:20) scrap was secured from Yemen and West Africa at $365-375/t CFR.

Pakistan: In Pakistan, the demand for imported scrap declined due to reduced demand for finished steel, compounded by payment delays and the ongoing Ramadan period. According to market participants, many small industries have ceased operations, and those still functioning are operating at less than 50% capacity. Typically, Ramadan is a slow period, but this time the situation has spun out of control.

On a weekly average, shredded scrap offers from Europe were evaluated at $419/t CFR, marking a $6/t increase compared to $413/t last week.

Notably, around 1,000-2,000 t of shredded scraps were booked during the week from the UK/Europe at $418-420/t CFR Qasim.

Bangladesh: In Bangladesh, despite Ramadan and a sluggish local steel market, the imported ferrous scrap market saw increased activity. Around 7,500-8,000 t of containerised deals were sealed from various origins like Singapore, Hong Kong, Australia, and Europe. BigMint’s assessment for Europe-origin shredded scrap (containers) rose by $3/t to $412/t, while HMS (80:20) containers increased to $400/t.

Bangladeshi importers secured a bulk shipment, including 18,000-20,000 t of Japanese H2 and 8,000-9,000 t of Singapore-origin HMS. US-origin HMS (80:20) bulk scrap rose by $5/t to $395/t CFR Chattogram. Domestic mills showed limited interest in UK/EU offers, preferring US-origin HMS, Hong Kong HMS bundles were offered at $390/t CFR. and the bulk HMS bids at $385-388/t.

Japan: Japanese export offers for H2 scrap remained steady for the second consecutive week, despite subdued interest from major importing nations.

According to BigMint’s latest assessment, Japanese H2 scrap export prices held firm at JPY 50,200/t ($331/t) FOB Tokyo Bay.

In the domestic market, Japan’s Iron and Steel Association reported a decline in average prices for H2 in three regions. Prices dropped JPY 300/t w-o-w, with prices in Kanto falling by JPY 400/t to JPY 48,800/t. Prices in Chubu were assessed at JPY 45,900/t (down JPY 600/t), and in Kansai at JPY 47,600/t (down JPY 200/t).

Vietnam: Vietnamese buyers exhibited limited interest in acquiring Japanese scraps due to discrepancies between bids and offers. Offers for H2 scrap from Japan were reported to be in the range of $370-375/t CFR Vietnam, whereas bids from buyers were hovering around $365/t CFR.

As per market participants, Vietnamese mills are actively purchasing local scrap, which offer quicker delivery, and they also have high inventory levels, thus diminishing the necessity to procure large volumes of imported scrap.

South Korea: South Korean mills continued to remain absent from the seaborne market as a result of subdued rebar and scrap sales, alongside reduced factory operating rates contributing to limited procurement activity in the South Korean domestic scrap market.

Furthermore, Japanese suppliers have ceased providing offers to Korea in light of the market conditions prevailing in South Korea.

This week, the combined steel scrap inventory held by the top eight South Korean steel producers stood at 873,000 t. This marked a modest increase of approximately 1,000 t compared to 872,000 t last week.

China: Shagang Steel has announced a downward adjustment in purchasing rates for ferrous scraps across all classifications, starting 28 March 2024. The updated rates show a decrease of RMB 50/t ($7/t). This marks the sixth successive price reduction for the month.