- Chinese mills withdraw offers ahead of holidays; SEA buyers inactive

- Iran maintains competitive FOB levels; shipment delays cap deals

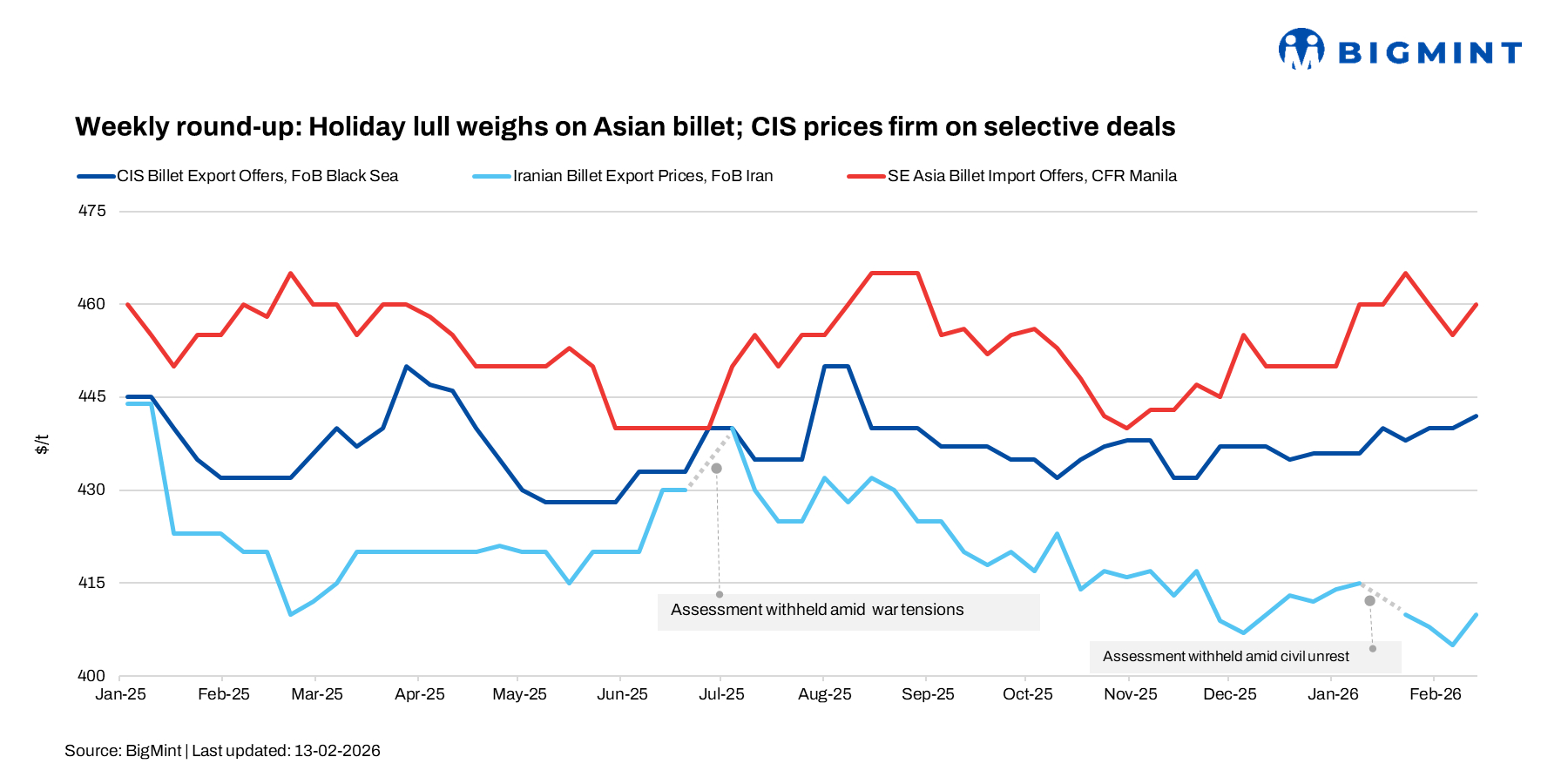

The Asian export billet market turned quiet this week as Lunar New Year holidays in China and Vietnam slowed activity. Chinese mills withheld firm offers, while indicative prices softened slightly. Southeast Asian buyers remained inactive amid weak downstream longs demand and sufficient inventories.

In Turkiye, deep-sea scrap prices edged down w-o-w. US-origin HMS 80:20 was heard at $375-376/t CFR, while EU-origin material stood at $368-371/t CFR, with a booking near $369/t CFR.

Despite tight US collection and limited EU availability, mills resisted higher offers due to weak rebar sales and compressed scrap-to-rebar spreads. Buying stayed need-based, keeping overall sentiment subdued.

China & Southeast Asian market

Indicative Chinese billet offers for April shipment were heard at $440/t FOB, down from $445/t last week. No firm offers were disclosed, as most mills are expected to suspend marketing from tomorrow. “Mills are not willing to take orders ahead of the break,” a Chinese trader said.

In Southeast Asia, open-origin 5sp billet was available at $460-465/t CFR, down $5/t w-o-w, with bids around $455-458/t CFR. Chinese 5sp was offered at $455-460/t CFR Thailand, against bids at $450-452/t.

Last week, around 20,000 t of Chinese 5sp billet was reportedly booked at $455/t CFR Manila. Additionally, 25,000-30,000 t of Iranian 4sp billet was heard to be sold at $445/t CFR Thailand, underlining Iran’s pricing edge in the region. However, earlier market talk of the same Iranian sales to Thailand at $440-445/t CFR remained unconfirmed.

A Thai billet consumer noted that although Iranian origin was about $10/t cheaper, buyers continued to favour Chinese cargoes due to shorter lead times and more reliable shipment schedules.

In Indonesia and the Philippines, Chinese 5sp billet was offered at $460/t CFR this week but attracted no buying interest. “Demand for billets is very slow because the longs market is not good,” a Southeast Asian importer said, reflecting weak downstream steel consumption across the region.

Indonesian Dexin Steel kept its base-grade billet offers unchanged at $455/t FOB for April shipment. However, buying remained muted as prices were considered high. The mill continues to prioritise slab output over billet, supported by better activity in the flats segment.

CIS market

Turkiye’s billet market recorded several transactions despite subdued downstream demand. Domestic producers in Iskenderun offered at $500-505/t exw, up from $490-500/t last week, with small lots of 1,000-3,000 t reportedly sold below offer levels. In imports, around 18,000 t of Russian billet was discussed at $466-470/t CFR Izmir, while another lot was heard at $464-465/t CFR, though both deals remained unverified. Additionally, 50,000 t of Chinese billet was reportedly sold at $470/t CFR, following an earlier booking of 50,000 t at $475/t CFR.

In the CIS export segment, Russian billet for the March-April shipment was held at $445-450/t FOB Black Sea. Sales to Turkiye were discussed at around $445/t FOB equivalent, prompting a $2-3/t increase in the CIS export assessment to $442-443/t FOB, reflecting firm realised levels despite cautious buying.

Iran’s exports market

Iranian billet offers were held at $395-405/t FOB, unchanged w-o-w. Activity was partially limited by the national holiday on 11 February (Islamic Revolution Day), though exporters continued to explore sales.

“Production costs remain underpinned by firm raw material prices and recurring energy supply constraints, limiting mills’ room to offer discounts,” a regional trader said. “At the same time, heightened political tensions and the risk of escalation are weighing on market confidence. Currency volatility and uncertainty around potential negotiations with the US are making planning extremely difficult. Nothing is predictable at this stage, and most participants prefer to wait for clearer signals before committing to fresh positions.”

Middle East

In Saudi Arabia, rebar trading improved as buyers restocked ahead of Ramadan. First-tier mills held offers at SAR 2,200-2,215/t delivered, while smaller producers adjusted workable levels to SAR 2,080-2,100/t to secure volumes. Hadeed set February rebar at SAR 2,260/t delivered, up SAR 70/t m-o-m. Market participants expect demand to fall by around 25% once Ramadan begins. Prices exclude 15% VAT.

In the UAE, mills largely concluded February sales. The benchmark rebar offer stood at AED 2,648/t exw, with transactions at AED 2,375-2,420/t CPT, up AED 25-55/t m-o-m. Retail levels remained firm, though participants cautioned that sustainability will depend on post-Ramadan demand.

Outlook

Outlook

In the coming week, we believe that Asian billet trade will stay muted until mills return from holidays and restocking emerges. Iranian offers may draw selective buying, but geopolitical and shipment risks will limit volumes. In Turkiye, scrap demand is expected to remain strictly need-based amid weak rebar sales. Middle East rebar activity is likely to slow during Ramadan, capping fresh billet appetite.

Leave a Reply