- U-turn on tariffs brings slight optimism in China

- Oversupply prompts corrections in Turkish scrap

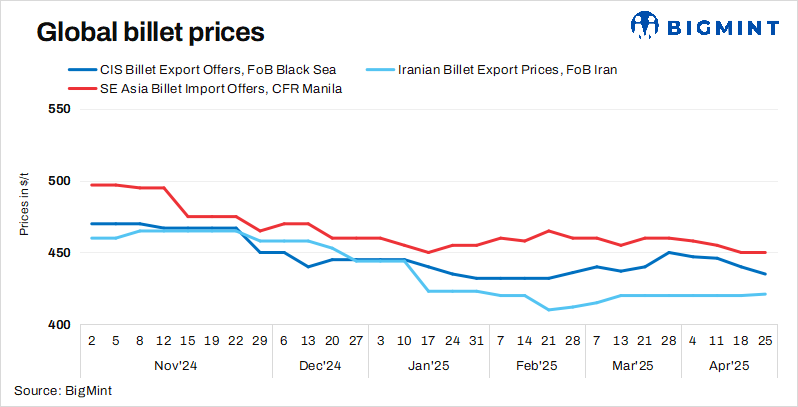

The global steel billet market in week 17 of CY’25 remained under pressure despite some signs of recovery. Prices showed mixed trends w-o-w across key markets, weighed down by a steep drop in scrap tags.

In China, prices saw a slight increase, driven by hopes of a potential shift in US-China trade tariffs. Meanwhile, demand in Southeast Asia was sluggish, especially in the Philippines, where market activity was limited. In the Middle East, competitive Chinese offers put downward pressure on local demand. Overall, sentiment was mixed, with geopolitical uncertainties and supply-side issues tempering any optimism, even as prices showed occasional upticks.

On the other hand, deep-sea imported scrap prices dropped by $20/t w-o-w to $324/t CFR Turkiye, their lowest since mid-2022. Turkiye’s steel market continued to face headwinds, with rebar sales showing only slight improvement amid ongoing pressure from weak demand and falling prices. Prices declined, as mills refrained from any major restocking due to persistent oversupply and a sluggish finished steel market (primarily rebars). Heading into May, the scrap market is expected to remain under pressure from oversupply, weak buying interest, and cautious sentiments despite some signs of improving demand for finished steel.

Market highlights

SE Asian imported billet prices fell w-o-w amid rising concerns over trade tensions and potential tariffs on Chinese steel exports. However, prices in the Philippines held firm w-o-w at $450/t CFR Manila on 25 April. Both traders and end-users alike remained in a wait-and-watch mode amid difficulties gauging the price direction.

The Vietnamese market remained largely subdued, with no significant bulk deals reported during the week. Export offers for Vietnam’s blast furnace (BF) grade billets held steady w-o-w at $450/t FOB on 25 April, reflecting limited buying interest and cautious sentiment across the region.

BigMint’s Russian billet index FOB Black Sea slipped by $5/t w-o-w to $435/t as of 25 April.

In Iran, market activity was relatively slow, with billet prices holding steady w-o-w at $420/t FOB on 25 April. Finished steel prices edged lower this week, weighed down by a weakening exchange rate and subdued demand, according to sources. Rebar prices also softened as buyer sentiment remained cautious amid lingering uncertainty surrounding the Iran-US trade negotiations.

Iran’s Khouzestan Steel Company (KSC) concluded a deal for 30,000 t at around $420/t FOB, while most other suppliers held back offers, awaiting the outcome of the upcoming Arfa tender, which is expected to close next week. Some sellers, however, were seen targeting higher levels of around $425/t FOB.

Chinese billet prices edged up by RMB 40/t ($5/t) w-o-w. Steel billet prices in Tangshan, China, rose by RMB 40/t ($5/t) w-o-w to RMB 2,980/t ($409/t), including 13% VAT, on 25 April. The market showed signs of a rebound this week amid growing speculation over a possible reversal in US-China trade tariffs. Daily trade volumes improved from the previous week, with prices witnessing a modest mid-week recovery, briefly touching RMB 3,000/t ($409/t) as sentiment turned cautiously optimistic.

Meanwhile, SHFE rebar futures (October 2025 delivery) climbed up by RMB 25/t ($3/t) to RMB 3,101/t ($426/t), indicating persistent market caution in the face of sluggish trading and muted downstream demand.

Leave a Reply