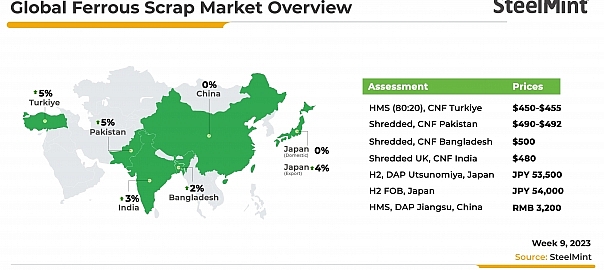

The global ferrous scrap market remained largely positive despite limited trade activities. The Turkish market seemed to be on hold with tariff revision for the steel sector, offers remained high while trade was subdued.

The Indian market was slow with bid-offer disparity being observed and players were in wait-and-watch mode before the Holi holiday week. Bangladesh’s ferrous scrap market saw some deals from Australia and the UK at a mixed price range to cater to immediate requirements as LC openings have become easier. On the other hand, Pakistan remained out of the market amid currency volatility.

Japan’s ferrous scrap export prices remained stable ahead of the Kanto tender, with buyers waiting for the tender results. Prices in Vietnam remained supported on global trends. China’s Shagang Steel did not revise its bids this week same as Japan’s Tokyo Steel.

Turkish scrap market on hold: Turkiye‘s import ferrous scrap market was on hold and mostly silent at the start of this week. However, mills opted to evaluate the situation for finished steel demand and supply.

After a meeting on 2 March, steelmakers planned a second meeting with the government on 7 March. The market expects subdued trading until the outcome is clear.

SteelMint’s daily assessment for HMS 1&2 (80:20) from the US stood at $450-455/t CFR Turkiye. Prices increased by $10-15/t w-o-w.

Pakistan’s scrap prices at 6-month high: Imported scrap prices skyrocketed to a six-month high in Pakistan fuelled by global price trend. However, market sentiments remained bearish. SteelMint’s assessment for imported shredded scrap in containers is $490-492/t CFR, $15-20/t w-o-w.

Bangladesh ferrous scrap offers increase w-o-w: Bangladesh‘s imported scrap market witnessed a recovery in trade activities and some deals for containerised and bulk scrap were seen. Despite the LCs issue and continuous price hikes, buyers are booking for April and May, SteelMint learnt from sources.

Containerised offers for UK-origin shredded scrap are at $500-505 /t CFR, down by $6-10/t w-o-w.

Fresh offers for US-origin bulk HMS were heard at $490-95/t CFR Chittagong, up $25-30/t w-o-w.

Indian ferrous scrap market slows down: Indian ferrous scrap prices remained high as offers from sellers increased by $20-25/t w-o-w on high demand following quick buying by Turkiye last week.

The domestic steel and scrap markets in India saw no major movement from the point of view of prices prior to the holiday week. Buyers were on hold amid payment settlement issues.

SteelMint’s assessment for imported shredded scrap in containers stood at $480/t CFR, up by $15-20/t w-o-w.

Japanese scrap export prices rise w-o-w: Japanese scrap sellers raised their offers prior to the Kanto tender – the price-setter in the domestic and export markets.

Buyers are waiting for the Kanto Tetsugen scrap export tender expected to conclude on 9 March. Taiwan has just returned from a two-day Peace Memorial holidays on 27-28 February, following which Japanese suppliers increased their offers to take advantage ahead of the Kanto tender.

SteelMint’s assessment for Japan’s H2 scrap export offers stands at JPY 54,000/t FOB ($398/t), up by JPY2,000/t ($15/t) w-o-w.

Vietnam’s scrap market supportive w-o-w: Prices for imported scrap in Vietnam surged may be due to bullish sentiments in Turkiye. However, buyers in the country could not source enough raw materials amid weak fundamentals in the finished long steel market.

Current offers for US-origin bulk HMS 1&2 (80:20) scrap were at $465-470/t CFR Vietnam last week, up $10/t w-o-w. Most suppliers are holding offers, waiting for a further hike on the back of active transactions by Turkish mills.

Leave a Reply