- Turkish imported scrap prices flat amid limited deals

- Indian buyers show caution, prices remain stable

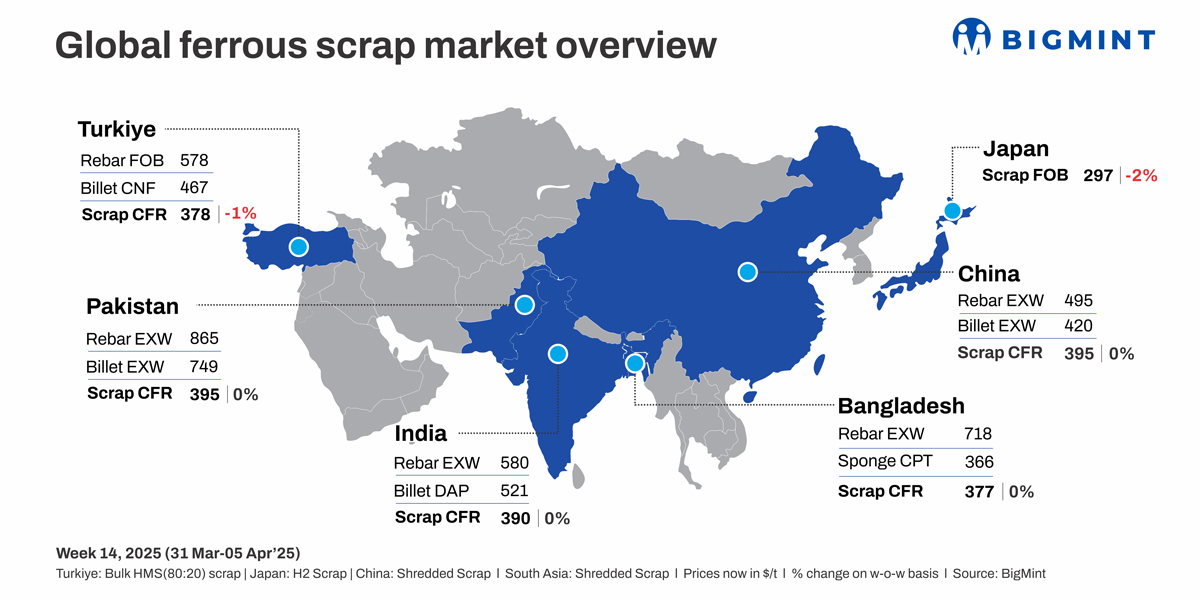

Global ferrous scrap prices remained largely stable this week, with bearish sentiment prevailing across markets. Weak finished steel demand, low rebar consumption, and ongoing Eid holidays have led to subdued activity in Turkiye, India, Pakistan, Bangladesh, and Vietnam. Japan and South Korea saw minor price adjustments amid cautious trading, while market participants awaited clearer signals on global trade policies and economic conditions.

Turkiye: The imported scrap market remained range-bound amid weak finished steel sales and low rebar demand. Mills were hesitant to restock despite strong availability of April shipment cargoes, leading to an oversupply, particularly from European sellers who held out for higher prices that didn’t materialise. US-origin HMS 80:20 prices hovered around $378/t CFR, slightly down from $381/t recorded in the previous week, while EU-origin offers ranged between $373-379/t CFR.

Market activity was subdued due to the Eid holidays, with buyers and sellers adopting a wait-and-see approach amid political uncertainties and US tariff expectations. European recyclers sought higher prices, but Turkish buyers remained cautious, bidding as low as $365-370/t CFR. Sentiment stayed bearish, with limited deals as participants awaited clearer trade policy signals.

India: The imported scrap market remained subdued this week, driven by cautious buying behaviour amid financial year-end closures and regional festivities like Eid and Navratri. Shredded scrap offers stayed at $390-395/t CFR, but buyers quoted $385-388/t. Similarly, HMS 80:20 from the UK/Europe and West Africa saw offers at $360-370/t CFR, with buyers aiming for $355-365/t, indicating a clear reluctance to pay higher prices.

Despite low activity, prices remained stable at around $390/t, as buyers awaited clearer price trends. Market sentiment was bearish, with participants hesitant to commit due to bid-offer mismatches and uncertain market conditions.

Around 17,000 to 18,000 t of imported scrap arrived in India, including 8,000 to 9,000 t of HMS 80:20 priced between $360-385/t, HMS 90:10 at $355-385/t, and 3,700 t of HMS 1 at $382-383/t.

Pakistan: The imported scrap market remained quiet this week, with Eid celebrations keeping buyers away from the market. Liquidity constraints and letter of credit (LC) issues further suppressed trading activity. Shredded scrap offers from the UK/Europe were stable at $395-400/t CFR Qasim, but buyer bids stayed around $390-395/t, reflecting cautious demand.

Domestic scrap prices hovered around PKR 140,000-145,000/t ($499-517/t), with rebar and billet prices holding steady. Mills operated at reduced capacity due to financial constraints, and while activity is expected to pick up post-Eid, high global scrap prices and economic uncertainty may result in slow recovery.

Bangladesh: Imported scrap prices remained subdued with minimal activity as buyers stayed cautious. Shredded scrap offers from the UK/Europe were steady at $395-396/t CFR Chattogram, with bids around $390-395/t, reflecting weak demand. HMS (80:20) offers from the UK/Europe and West Africa stood at $365-375/t CFR, with buyers aiming for $360-370/t, limiting transactions.

Domestic steel prices showed little change, with rebar at BDT 82,000-83,000/t ($676-$684/t) in Dhaka and BDT 86,000-87,000/t ($709-$717/t) in Chattogram, while billets stayed at BDT 72,000-74,000/t ($/t). Mills operated at reduced capacity due to liquidity constraints and LC issues. Post-Eid recovery is expected, but high global scrap prices and economic uncertainty may limit the recovery. Sentiment remained bearish, with shredded scrap prices stable at $395-396/t.

Japan: H2 scrap export offers fell by JPY 800/t ($5/t) w-o-w to JPY 43,500/t ($298/t) FOB Tokyo Bay, pressured by weak demand and lower billet prices. Traders remained cautious ahead of the upcoming Kanto Tetsugen tender.

Domestic FAS collection prices for H2 rose slightly to JPY 41,500-42,500/t ($284-291/t). Tokyo Steel adjusted scrap procurement prices on 3 April, with increases of JPY 1,500/t ($10/t) at Tahara (JPY 42,000/t) and Nagoya (JPY 40,500/t), while other plants saw no changes.

US: The US ferrous scrap export index fell $3/t w-o-w, driven by weak demand from Turkiye, Bangladesh, and Vietnam amid Eid holidays and trade uncertainties. FOB HMS 80:20 and shredded dropped to $355/t and $375/t, respectively. CFR prices were stable in Vietnam and Bangladesh but down in Turkiye. Demand remains muted, with post-holiday recovery expected.

South Korea: South Korea’s combined ferrous scrap inventory at eight major steel mills rose 5.4% w-o-w to 767,000 t, driven by stockpiling amid lower scrap prices. Stocks in the central region surged 14% to 378,000 t after an 3 April price cut, while inventories fell 1.7% to 389,000 t in the south due to limited stocking amid production cuts.

Hyundai Steel’s Pohang plant resumed operations, improving scrap consumption, though weak rebar demand led to reduced production and halted rebar output at Incheon in April.

Leave a Reply