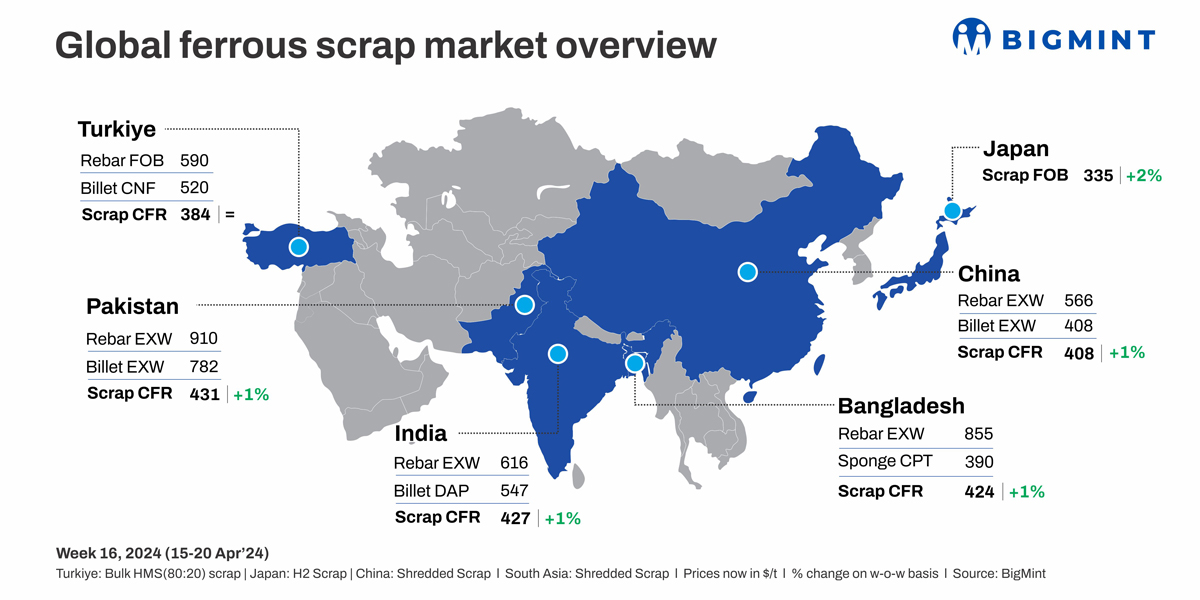

The global ferrous scrap market showed a rising trend in terms of prices, experiencing better demand, especially in South Asia. Indian buyers remained active towards the weekend due to rising scrap prices in the domestic market and supply shortage.

Meanwhile, markets in Pakistan remained subdued as they still remained sidelined following a dull demand in the finished steel market. Following a slow domestic long steel market, Turkish steelmakers continued their regular trade volume this week in the $379-386/t price range from Europe and US on a CFR basis.

In Japan, export offers for H2 scrap saw a rise amid recent trades captured from Vietnam, furthermore, in South Korea, scrap inventories in major steel mills witnessed a modest decline.

Turkiye: This week, Turkiye’s local steel market saw weak demand due to liquidity constraints from higher interest rates. Restrictions on steel exports to Israel further dampened demand. Turkish mills explored UK scrap deals amid favorable exchange rates.

During the Eid holiday, the market heard a couple of deals from the UK at $380/t and $381/t respectively, comprising around 40,000-45,000 t of mixed scrap CFR Turkiye.

BigMint’s US-origin HMS (80:20) bulk scrap stayed at $384/t CFR, while US East Coast bulk HMS (80:20) fell to $360/t FOB. Turkish rebar exports stood at $590/t FOB, The scrap-to-rebar spread narrowed to $206/t FOB from $211/t last week.

This week, an Aegean region-based mill, with 27,000 t mixed scrap comprising 17,000 t of HMS (80:20) at $382/t CFR and 10,000 t of shredded scrap at $399/t CFR Turkiye. The same mill booked UK-origin bulk cargo at $379/t comprising HMS (80:20) on a CFR Turkiye basis.

Another deal was reported from the US involving HMS (80:20) at $386/t, booked by a Mediterranean region-based mill on a CFR Turkiye basis.

India: This week in India, the demand for imported scrap remained better as buyers attempted buying both in containers and bulk after seeing a rising trend in domestic scrap price. Shredded scrap offers from Europe saw an increase, rising by $6/t to $427/t CFR compared to $421/t CFR in the previous week. Similarly, HMS (80:20) offers from Europe also climbed to $402/t CFR, up by $7/t from the previous week’s $392/t CFR.

In noteworthy transactions, approximately 10,000 t of various scrap grades including HMS, shredded, Forging and rolling scrap along with PNS and LMS bundle mix grade was secured from Africa, US , Hong Kong , Brazil and Europe at the range of $400-480/t on a CFR basis.

It is noteworthy that, Indian steel mills have secured bookings of approximately six bulk scrap vessels in April 2024. The vessels, originating in the US west coast, are expected to reach most probably Kandla, Chennai, and Vizag ports, between May and June. The deals were heard at $410-415/t for shredded and $395-400/t for HMS (80:20). Bulk offers have increased by $5-10/t.

As per recent indications, the mood in the market is positive as supply is not strong. Plus, due to the elections (no trade of non-billed) and limited pipeline, Indian buying is good.

Pakistan and Bangladesh: Throughout the week, market activity in Pakistan was minimal due to weaker demand for finished steel followed by an uncertain outlook predicted by steelmakers before future purchasing. Offers from Europe for containerised shredded stood at $431/t increased by $4/t w-o-w. Additionally, in Bangladesh, the price of imported ferrous scrap price increased up to $3/t w-o-w across bulk and containers owing to a firm supplier stance and multiple inquiries from steelmakers in Dhaka and Chattogram.

Japan: This week, Japanese H2 scrap export offers rose by JPY 1,000/t ($6/t) on heightened demand from Vietnam. BigMint’s latest assessment puts Japanese H2 scrap export offers at JPY 51,800/t ($335/t) FOB Tokyo Bay, up from JPY 50,800/t ($329/t) FOB the previous week.

Tokyo Steel lowered domestic ferrous scrap prices by JPY 1,000/t ($6/t) starting April 19, 2024. H2 scrap prices at the Utsunomiya plant are now around JPY 50,500/t ($327/t), while prices at Tahara and Okayama remain unchanged.

South Korea: This week, the ferrous scrap inventory across eight major South Korean steel mills experienced a modest 1% decline, totalling 862,000 tonnes (t) compared to the 868,000 t reported in the previous week. Regionally, the central area, which had lower operational rates due to extended maintenance, saw a decrease, while the southern region observed a slight increase in inventory, attributed to reports of price reductions.

China: China’s State Administration of Taxation announced the full implementation of the ‘reverse charge’ invoicing system for recycling enterprises and small-scale sellers of waste materials by the end of this month. This system allows recycling enterprises to issue invoices to individual sellers when procuring waste materials, alleviating the difficulty in obtaining invoices for purchases. The move aims to ease the tax burden on the recycling industry, providing a compliant deduction voucher for income tax payments.