- Prices into Turkiye fall as mills resist high costs

- India’s shredded scrap fell on weak demand, ample supply

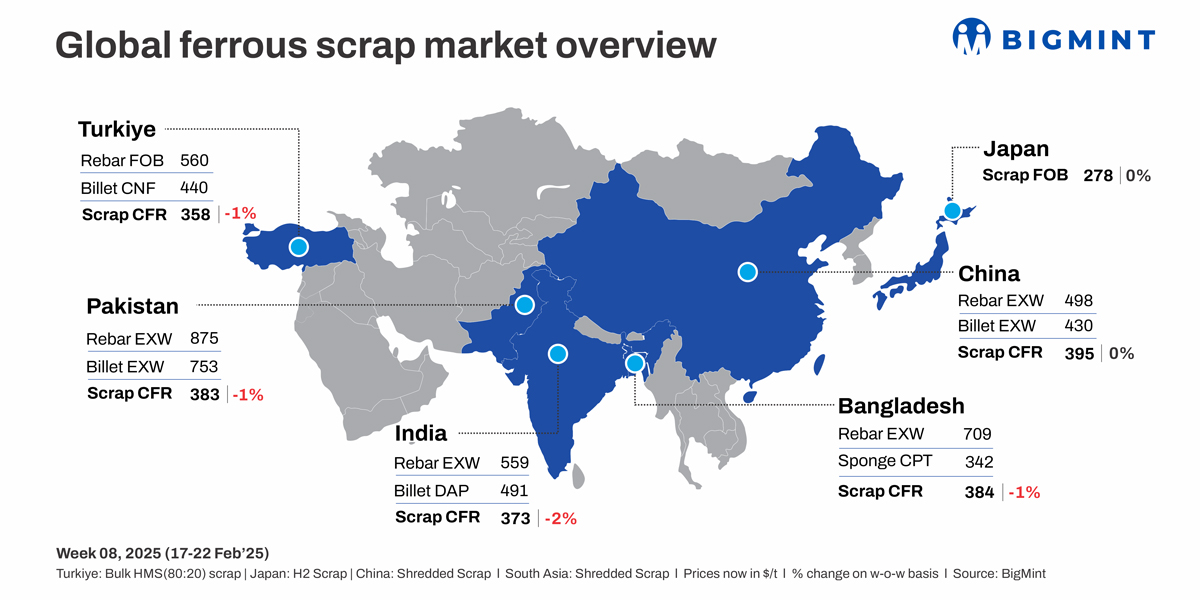

Global ferrous scrap offers fell as weak steel demand, high import costs, and cautious buying limited trade activity. Turkish mills resisted higher prices, pushing HMS 80:20 to $358/t CFR. South Asia saw subdued demand amid sluggish construction. Japan and Taiwan maintained firm prices, while Vietnam saw slight gains. US export offers dropped by $2/t w-o-w.

Turkiye: Turkiye’s imported scrap market remained under pressure as mills resisted higher prices amid weak finished steel demand and competitive billet prices. US-origin HMS 80:20 was initially offered at $360/t CFR, but buyers pushed for lower levels and settled at $358/t CFR.

Despite some restocking activity for March-April shipments, overall demand remained sluggish. European recyclers faced high collection costs, while Turkish mills preferred Baltic and EU-origin scrap over expensive US shipments. Kardemir cut rebar prices by $20/t, reflecting continued market caution ahead of the EU anti-dumping measures.

Mills continued seeking cost reductions, keeping scrap demand steady but lacking momentum.

India: India’s imported scrap market remained subdued as ample domestic availability, weak steel demand, and currency fluctuations kept buyers cautious. Shredded scrap offers from the UK/Europe fell to $373/t CFR Nhava Sheva a down 2% w-o-w, while HMS (80:20) ranged between $345-355/t CFR, Traders expect limited recovery unless global prices stabilize or local demand improves, with potential movement post-March.

Market sentiment remained bearish, with bid-offer mismatches and weak finished steel demand limiting activity. Premium scrap supply was tight, while buyers awaited clarity on US tariffs set for 12 March. Sellers held firm, but buyers pushed for lower prices.

Around 4,500-5,000 t of scrap were booked, including 3,000-3,500 t of HMS (80:20) from Latin America, Mozambique, Australia, West Indies, and Madagascar at $350-375/t. Additionally, 1,000-1,200 t of Blue steel scrap from Brazil and the UK traded at $385-392/t, while 500-600 t of Bundle scrap from Yemen was secured at $310/t.

Pakistan: Pakistan’s imported scrap market remained subdued as UK-origin shredded scrap declined 1% to $383/t CFR. Offers from the UK/Europe stood at $380-390/t CFR Qasim, but buyers placed lower bids at $373-382/t CFR, leading to minimal trade activity amid weak liquidity, sluggish steel demand, and cautious buying ahead of Ramadan.

Market participants anticipate limited demand recovery unless liquidity conditions improve and domestic steel sales strengthen. Delayed government payments and cash flow constraints further pressured rebar sales, with prices ranging from PKR 235,000-245,000/t.

Bangladesh: Bangladesh’s imported scrap market remained slow although 27,000-28,000 t of imported scarp was booked. The weak steel demand, sluggish construction activity, and a lack of new government infrastructure projects kept buying interest limited. With ample mill inventories and slow liquidity, buyers remained hesitant to commit to fresh deals, leading to minimal market activity.

PNS offers from Hong Kong and Singapore stood at $385-390/t CFR Chattogram, while HMS (80:20) from Brazil was heard at $365/t CFR. Some containerized trades for Singapore-origin PNS occurred at $382-385/t CFR, but overall sentiment stayed cautious.

With Ramadan nearing, traders took a wait-and-see approach. UK-origin shredded scrap fell 1% to $384/t CFR, reflecting weak liquidity and subdued demand.

Japan: H2 scrap offers rose slightly due to currency shifts, tight supply, and firm seaborne prices. Tokyo Steel raised Kansai plant prices by JPY 1,000/t, while other plants remained unchanged. H2 export prices edged up to JPY 41,500/t ($276/t) FOB Tokyo Bay, with buyers cautious amid global trade uncertainties.

Vietnam: Vietnam’s imported scrap market rose as Japanese H2 offers hit $320-$322/t CFR amid port congestion and supply tightness. US deep-sea offers fell to $355-$360/t CFR, while Australian-origin dropped to $350-$355/t CFR. Improved construction demand supported prices, but buyers remained cautious, closely monitoring trade policies and China’s economy.

South Korea: South Korea’s imported scrap market remained weak as buyers stayed cautious. US-origin offers hovered at $345-$350/t CFR, while Japanese H2 stayed firm amid tight supply. Low construction demand and rebar production cuts limited buying interest, with scrap imports dropping 20,000 t w-o-w to 79,432 t, though unloading is expected soon.

US: US ferrous scrap export offers fell by $2/t w-o-w as high import costs and weak rebar demand kept Turkish mills cautious, limiting US deep-sea exports. HMS 80:20 offers stood at $362-365/t CFR Turkiye, while US West Coast offers were $365-370/t CFR Bangladesh and $352-358/t CFR Vietnam.

Taiwan: Taiwan’s imported scrap market continued rising, with US HMS 80:20 at $313/t CFR and Japanese H2 at $320/t CFR. Higher scrap costs led Feng Hsin Steel to raise rebar prices by TWD 200/t. Strong rebar sales supported hikes, but weak Chinese steel prices kept the market outlook cautious.

Leave a Reply