- India market quiet, mills prefer local scrap

- UAE prices up on rising fabrication demand

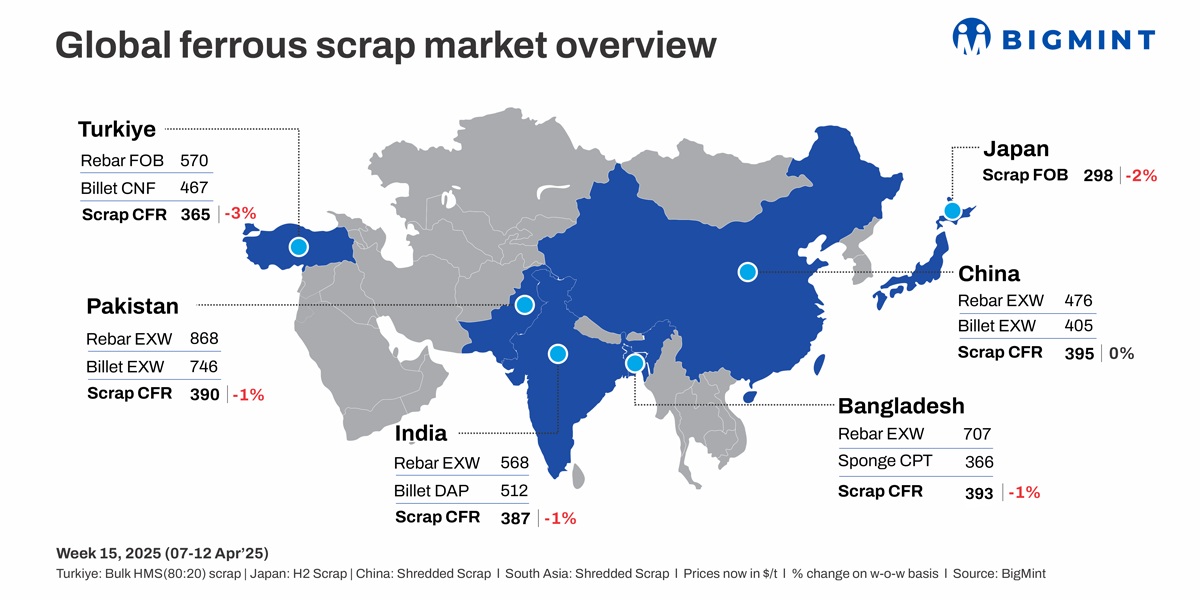

Global ferrous scrap prices fell this week, with markets in Turkiye, Pakistan, and Bangladesh seeing declines due to weak demand and resistance to higher offers. Sluggish steel sales and rising energy costs pressured mills, while tariff uncertainties and soft domestic demand kept market activity limited.

Turkiye: The Turkish imported scrap market stayed under pressure, with HMS 80:20 prices falling 3% w-o-w to $365/t CFR. Mills largely avoided fresh bookings amid weak finished steel sales, and rising energy prices. Despite ample availability, trade activity remained limited as mills lacked urgency to restock.

The bearish tone intensified mid-month as production costs surged due to electricity and gas price hikes, further straining mill margins. Meanwhile, domestic rebar demand stayed sluggish, pushing mills to consider alternative raw materials like billets and short-sea scrap. Sellers, particularly in the EU, resisted deeper cuts due to strong currencies and collection costs, but few offers translated into deals.

Overall sentiment was bearish, with limited mill interest and mounting buy-side pressure driving prices lower. Some participants expect prices to stabilise near $360/t CFR if restocking resumes and billet demand improves.

India: The imported scrap market stayed quiet in early April with minimal activity due to a persistent bid-offer gap and weak buyer interest. Shredded offers held firm at $390-395/t CFR, while buyers remained below $385/t. HMS 80:20 saw similar disconnect, with bids trailing offers by $5-7/t. Shredded scrap from the UK dropped slightly to $387/t CFR India, reflecting mild downward pressure despite firm seller expectations.

Despite strong steel sales, mills preferred local scrap and sponge iron due to cost-effectiveness. Seasonal demand supported steel prices, but scrap buying stayed weak as mills used existing inventories. Uncertainty over safeguard duties and firm offers, supported by local demand and a strong euro, kept buyers cautious.

Around 5,000 to 6,000 t of imported HMS 80:20 scrap arrived in India, priced between $351-370/t from West Africa, Caribbean, Brazil, Ireland, Central America, Chile, Congo and Poland and HMS 1 at $384/t from Bahrain.

Pakistan: Imported scrap market remained subdued throughout the week, with limited activity and buyer resistance to high offers. UK/EU shredded scrap hovered at $390-395/t CFR Qasim, down 1% w-o-w. Domestic demand stayed weak amid slow construction, security concerns in Balochistan, and post-Eid inertia.

UAE-origin scrap offers remained firm, but overall sentiment was soft due to global uncertainty and sluggish recovery. A recent electricity tariff cut offered some margin relief, yet it failed to spur significant buying. Mills stayed cautious, awaiting clearer signals before ramping up procurement.

Mills stayed cautious on scrap purchases amid weak demand and budget uncertainty. Domestic scrap was at PKR 135,000-140,000/t, billets at PKR 200,000-205,000/t, and rebars at PKR 235,000-240,000/t. Imported shredded held at $390-395/t CFR Qasim, with limited post-Eid buying.

Bangladesh: The imported scrap market remained quiet post-Eid, with limited buying amid ongoing LC issues and tight forex liquidity. Offers for shredded hovered at $385-395/t CFR, and Australian HMS 80:20 was at $365-370/t. Despite available offers from the UK, EU, and East Asia, trading was slow as mills relied more on domestic scrap and avoided aggressive restocking. Sentiment remained sluggish, with shredded scrap prices dropping by 1% from $396/t to $393/t.

Domestic rebar prices rose by BDT 500/t amid slightly better sales, reaching BDT 82,000-83,000/t in Dhaka and BDT 85,500-87,000/t in Chattogram. Shipyard PNS and HMS stood at BDT 57,000-57,500/t and BDT 55,500-56,500/t ex-yard, respectively.

Japan: The H2 scrap export market weakened in early April due to sluggish demand, particularly from Vietnam, and currency fluctuations. The Kanto Tetsugen tender dropped to JPY 43,288/t ($303/t), while export offers fell to JPY 42,800/t ($299/t) FOB Tokyo Bay, reflecting the softening market.

Tokyo Steel reduced domestic purchase prices by JPY 500/t due to high inventory levels. Despite regional price variations, the overall market sentiment stayed cautious as global demand remained weak, with uncertainty around steel prices and currency fluctuations.

Vietnam: The imported scrap market stayed quiet as weak steel demand, a softening dong, and tariff uncertainty kept buyers cautious. Japanese H2 slipped slightly, with the Kanto tender aligning at $330-335/t CFR. US bulk offers saw bids below $350/t. Mills stayed on the sidelines, avoiding fresh bookings amid volatile pricing and unclear policy signals.

The UAE: Domestic scrap prices increased, particularly for fabrication and processed HMS, driven by rising demand. BigMint’s processed HMS index rose by AED 26/t ($7/t). Fabrication scrap now trades at AED 1,250-1,290/t ($340-351/t). Despite a firm market, uncertainty over global prices and post-Eid slowdown concerns keep buyers cautious. Export offers for UAE HMS are at $370-375/t CFR Qasim.

The US: Ferrous scrap export prices dropped, with shredded and HMS 80:20 falling by $10/t. Domestic supply surplus and weak demand from key markets like Turkiye and Vietnam pressured prices. Mills in Turkiye, Bangladesh, and Vietnam were cautious amid rising energy costs and tariff concerns. The US market is expected to remain soft, though rising pig iron costs may offer limited support.

Leave a Reply