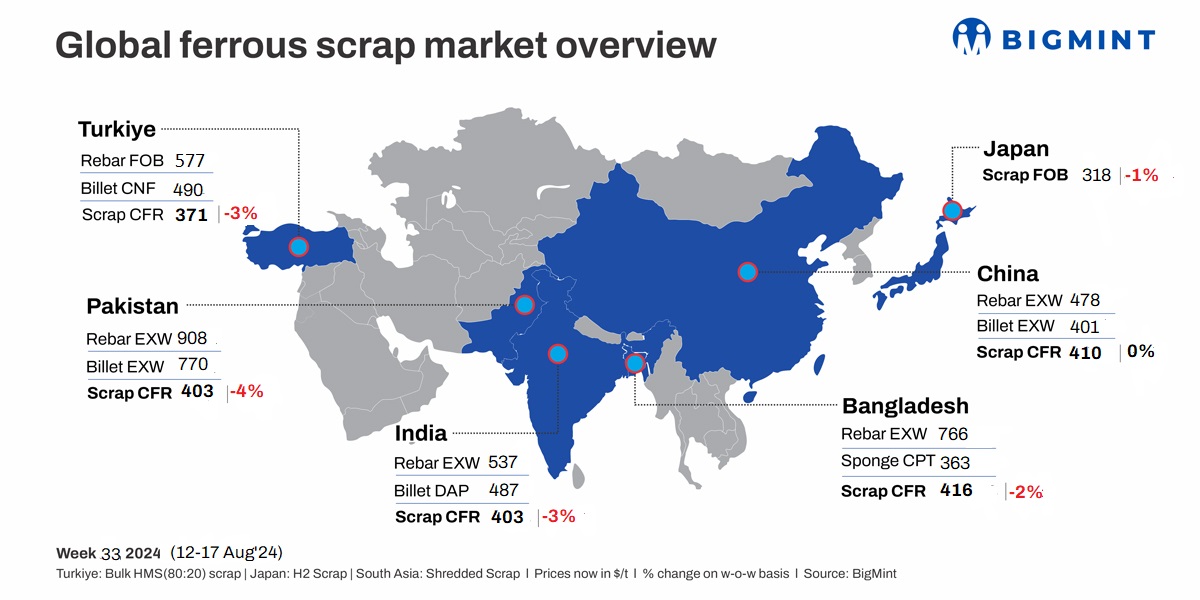

The global ferrous scrap market witnessed a week of declining prices and cautious buying activity, driven by weak demand across major importing nations.

In Turkiye, scrap prices fell as Turkish mills shifted focus to cheaper Asian billets further exacerbating the market’s downward trend. India and Pakistan’s imported scrap markets also faced subdued demand, with buyers hesitant due to weak domestic steel sales and economic uncertainties. In Bangladesh, containerised scrap prices continued to decline amidst a monsoon-affected steel sector, while China’s scrap market remained bearish, marked by Shagang Steel’s fourth consecutive price cut in August.

Meanwhile, Japan’s H2 scrap export offers dropped amid limited interest from key importers.

Turkiye: Turkish imported ferrous scrap prices dropped by $10/t w-o-w, driven by weak steel sales and cheaper Asian billets. Despite re-entering the deep-sea scrap market, Turkish mills saw limited demand due to competition from Asian billet imports.

Turkish steel producers remain mostly inactive in the deep-sea scrap market, closely monitoring for potential price drops. Their focus on cheaper billets and slabs continues to exert downward pressure on scrap prices.

Similarly, under pressure from cheaper billets, BigMint’s assessment for US-origin HMS (80:20) bulk scrap has reached its lowest level for 2024.

As per a recent report, Habas a major steelmaker in Turkiye has made a purchase of 50,000 t of billets from China, delivered to Turkiye at a price of $465/t CFR.

Turkish mills may need to lower finished product prices below $570/t to sustain sales. The ongoing drop in iron ore prices to $92/t has further weakened scrap sentiment. Black Sea and Asian billets are exerting additional pressure on scrap prices.

India: India’s imported scrap market remained sluggish, with demand nearly nonexistent due to a lack of buying interest driven by weak domestic steel sales. Steel mills across the country scaled back production, opting for cheaper domestic alternatives like sponge iron over imported scrap. Offers for shredded scrap from the US and Europe fluctuated between $400-405/t CFR Nhava Sheva, but buyers were largely absent, finding these prices too high compared to domestic options.

HMS (80:20) offers also failed to attract interest, even as prices dropped to around $375-380/t CFR. Mills and traders alike expressed reluctance to engage in imported scrap bookings, citing the unfavourable price gap and ongoing weak steel demand. Some buyers, however, secured small deals in anticipation of tighter supply, but the overall sentiment remained cautious and bearish throughout the week.

Pakistan: Pakistan’s imported scrap market saw limited activity throughout the week, as buyers remained cautious amidst sluggish domestic steel sales and ongoing market volatility. Offers for shredded scrap from the UK/Europe fluctuated between throughout the week, starting with $ CFR Qasim, but most buyers refrained from purchasing, anticipating further price declines.

The situation was further complicated by a major money laundering scandal in the iron and steel sector, where importers evaded taxes and illegally transferred funds abroad. This scandal contributed to a lack of confidence in the market, prompting buyers to adopt a wait-and-see approach. Only a few small transactions were reported, with prices as low as $397/t CFR Qasim. Overall, the market remained subdued, with buyers hesitant to commit to new purchases amidst the prevailing uncertainty and expected price corrections.

Bangladesh: Bangladesh’s imported ferrous scrap market saw a declining trend in containerised ferrous scrap prices this week. Despite recovering market activities, bids remained unchanged and at lower levels due to a monsoon-affected steel sector. Market sentiment remained low, but improvement is expected once banking and financing stabilize post-government formation.

BigMint’s assessment of Europe-origin containerised shredded declined over $10/t w-o-w and stood at $416/t, while HMS (80:20) prices stood at $400/t (declined by $6/t w-o-w).

Japanese H2 was offered at $405-408/t, with bids at $395-398/t. US offers included HMS (80:20) mix at $405/t and shredded at $412-414/t. UAE-origin HMS 1 was offered at $425-428/t Indicative prices from the UK/EU showed shredded at $420-422/t.

Domestic rebar prices are range-bound at BDT 86,000-87,500/t ex-Dhaka and BDT 91,000-91,500/t ex-Chattogram. Ship plate scrap is priced at BDT 71,500-72,000/t exy.

Amid nationwide disruptions, Bangladesh’s electricity demand surged by 7%, leading to a 26.6% increase in thermal coal imports this year.

Japan: Japanese H2 scrap export offers decreased by JPY 500/t ($3/t) this week, bringing the price down to JPY 47,000/t ($318/t) FOB Tokyo Bay. This decline is driven by weak demand from major importing countries. For example, Vietnam has shown limited interest due to a drop in domestic steel and scrap prices, indicating sluggish demand. Korean mills have also focused on domestic scrap procurement.

China: Shagang Steel has recently reduced its ferrous scrap prices by RMB 80/t ($11/t) for all grades effective 15 Aug’24. HMS (6-10 mm) is now priced at RMB 2,390/t ($333/t), including 13% VAT. Notably, this marked the company’s fourth price cut in August, bringing the total decline to RMB 250/t ($35/t).

Leave a Reply