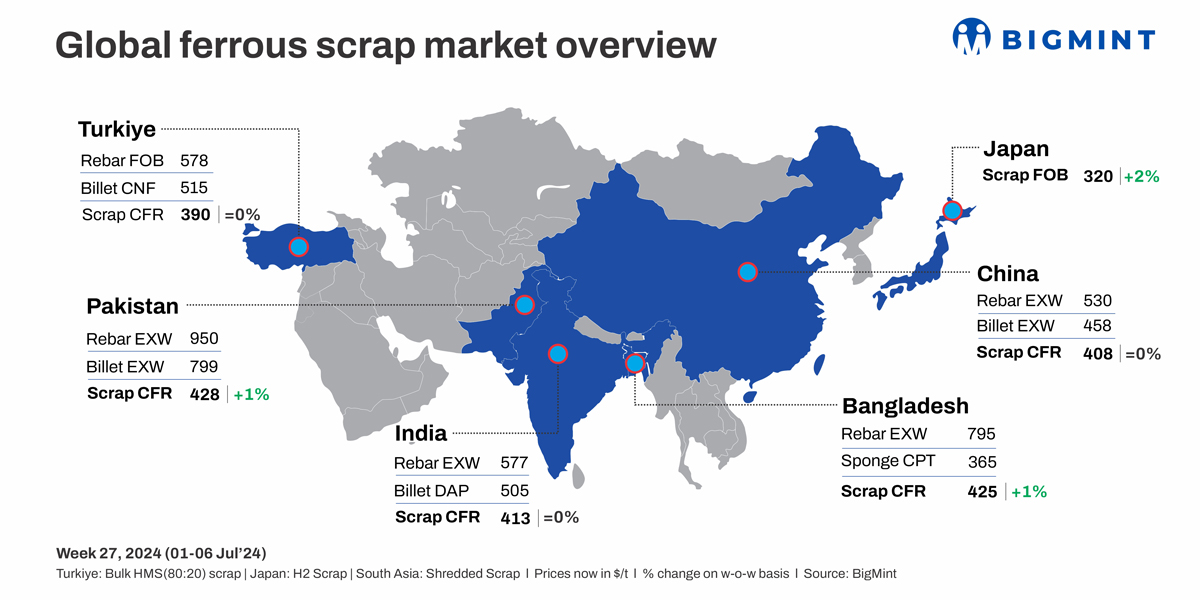

Global ferrous scrap prices showed a positive trend in major markets. In South Asia, Indian buyers went slow with imported scrap bookings due to high prices and cheaper domestic options. Demand in Bangladesh remained moderate, with rebar prices dropping in the rainy season.

Pakistani imported scrap prices rose by $5/t w-o-w, prompting mills to hike rebar offers amid rising costs and taxes. Turkish imported scrap prices from the US held steady, with active bookings seen.

Vietnamese imported scrap prices fell by up to $3/t w-o-w due to weak demand, as some mills preferred cheaper domestic billets. Japanese H2 scrap export offers increased by $6/t w-o-w due to supply tightness owing to reduced generation amid extreme heat.

Turkiye: In early July, mills purchased scrap to maintain production levels while avoiding large stockpiles due to limited rebar sales. Scrap prices faced upward pressure from slow collection, high portside quotes, and a $4-5/t rise in freight costs. European sellers grappled with high collection costs, and Turkish mills dealt with firm input expenses, resulting in mixed price expectations. Consequently, US-origin scrap prices edged slightly higher than European cargoes.

Imported bulk scrap offers from the US increased by $3-4/t w-o-w. The Eid holidays in late June boosted buying activity, stabilising scrap prices at $390-392/t CFR. Turkish buyers acquired 0.6-0.7 mnt of ferrous scrap in June, a decrease of 0.5 mnt from May.

BigMint’s assessments: US-origin HMS (80:20) bulk scrap rose to $390/t CFR, largely stable w-o-w; US East Coast bulk HMS (80:20) increased to $364/t FOB, up $3/t w-o-w. The scrap-to-rebar spread remained stable at $188/t FOB.

India: This week in India, the imported scrap market saw limited activity due to several factors. Buyers hesitated due to softening steel prices, bid-offer disparity, and long delivery times from the UK, currently 45-50 days. Container shortages also pose problems.

Despite decent domestic scrap availability, GST raids on major dealers in south India raised concerns about potential shortage. Offers for US and UK/Europe shredded scrap were at $410-415/t CFR Nhava Sheva, with buyers bidding at $405-408/t CFR.

While there was a slight improvement in the western region, buyers in the south were mute due to subdued steel demand and high freight rates. By the end of the week, the market turned sluggish as buyers opted for cheaper domestic scrap, and mills faced the prospect of reducing output. Traders anticipate a potential uptick in activity after mid-July despite ongoing challenges with freight and shipping costs.

Pakistan: Pakistan’s imported ferrous scrap prices rose by $4-5/t with UK-origin shredded scrap at $426-428/t CFR Qasim. The market faced challenges due to high raw material costs, taxes, and low demand. A market insider predicts prices will rise next week, noting sluggish movement and liquidity issues. UAE offers for shredded scrap were at $430/t, and HMS mixed scrap at $408-410/t CFR Qasim.

BigMint’s assessment for Europe-origin shredded rose by $5/t to $428/t w-o-w. Logistical challenges, including container shortages and Red Sea route diversions, are expected to keep freight rates high.

Domestically, major steelmakers like Amreli Steel, Naveena, Siraj, and Mughal Steel raised rebar offers by PKR 5,000-8,000/t from 1 July due to increased costs and taxes despite weak demand. Domestic scrap prices rose to PKR 160,000-162,000/t, and billet offers were at PKR 220,000-222,000/t exw.

Bangladesh: In early July, Bangladesh saw a slight uptick in imported ferrous scrap prices for bulk offers, while containerised scrap remained range-bound. Multiple bookings from Australia and the US were reported due to better LC openings and higher freight rates from Malaysia and Hong Kong, making Australia a more attractive option.

EU-origin shredded scrap was offered at $423-426/t, and HMS (80:20) at $400-404/t, while US-origin HMS (80:20) bulk offers stood at $405-407/t. Notably, Bangladesh’s ferrous scrap imports rose by 26% in H1 CY’24 to 2.35 mnt. Despite a sluggish domestic steel market, buyers favoured Australian and Singapore-origin scraps, with significant bookings from Australia seen at $405/t CFR Chattogram.

Japan: This week, Japanese H2 scrap export offers increased by JPY 900/t ($6/t) due to tight supply in the domestic market. However, demand from key importing markets remained muted.

The domestic supply tightness was caused by slow generation due to extreme heat and recyclers focussing on fulfilling the previous month’s Kanto tender volume of 25,000 t. Additionally, scrap procurement by Tokyo Steel’s Tahara plant rose after it resumed operations, which had been halted due to ancillary equipment damage.

According to BigMint’s latest assessment, Japanese H2 scrap export offers stand at JPY 51,400/t ($320/t) FOB Tokyo Bay compared to JPY 50,500/t ($314/t) FOB last week.

South Korea: Except for POSCO, South Korean steel mills showed little interest in seaborne scraps due to a slow domestic market. This week, the ferrous scrap inventory of eight major South Korean steel manufacturers increased by 5% to 825,000 t, up from 790,000 t in the previous week. This marks the first time since early May that inventory levels have surpassed 800,000 t, with increases noted in both the central and southern regions.

Vietnam: Vietnamese steel mills showed little interest in procuring scrap from the seaborne market due to a subdued domestic market for both flat and long steels. Additionally, some steel mills have opted to purchase more billets instead of scrap, driven by a prolonged decline in billet prices in the region.

China: Shagang Steel has announced an increase in purchase prices of ferrous scrap after consecutive price declines. The updated prices reflect an increase of RMB 50/t ($7/t). Under the new pricing structure, HMS (6-10 mm) is now at RMB 2,790/t ($384/t), including 13% VAT. Notably, this marks the company’s first price hike in July, after three consecutive price cuts in June.

Leave a Reply