- Indian imported scrap offers decline amid currency fluctuations

- Imported scrap offers into Turkiye rise on bullish sentiment

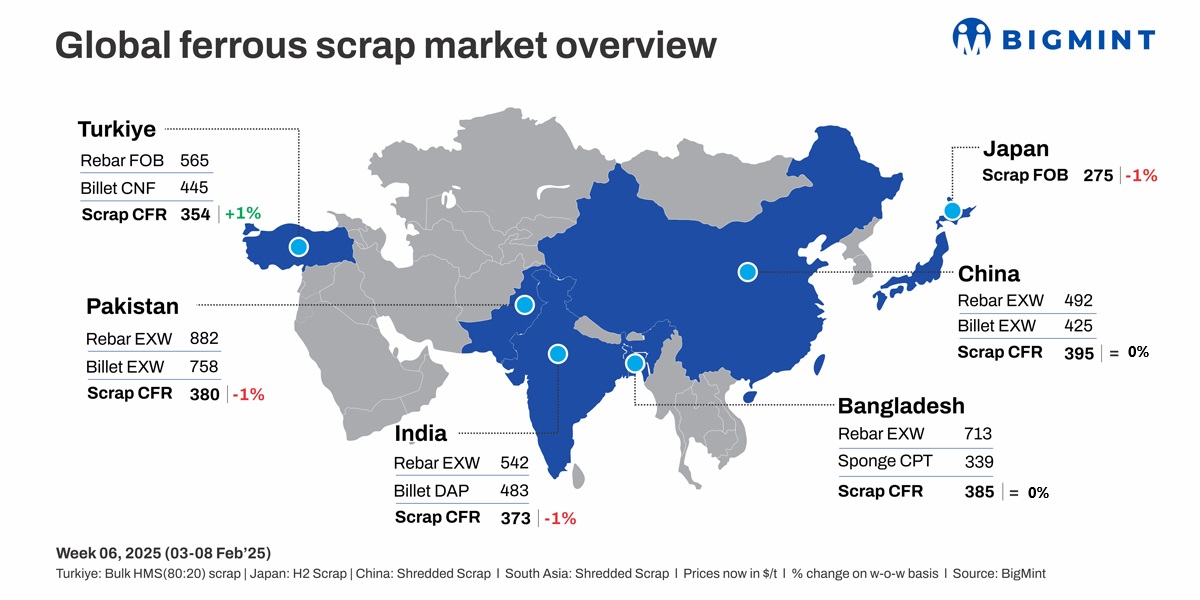

Global ferrous scrap markets witnessed a mixed trend this week. Turkiye’s US-origin HMS 80:20 CFR rose 1% to $354/t amid restocking, while India’s shredded scrap fell 1% to $373/t due to weak demand. Pakistan and Bangladesh saw sluggish trade, with UK-origin shredded at $383/t and $385/t CFR, respectively. Japan’s H2 export dropped to JPY 41,600/t ($274/t), while South Korea’s imports surged.

Turkiye: Turkiye’s imported scrap market saw a 1% increase in US-origin HMS 80:20 CFR prices, rising from $349/t to $354/t over the week. The market was supported by positive US domestic scrap expectations and Turkish mills’ continued restocking, despite fluctuating currency trends and cautious buying behavior.

Price movements were influenced by US-China trade tensions, new US tariffs on Canada, Mexico, and China, and rising collection costs in Europe, which limited competitive offers despite a weaker euro. Deep-sea scrap activity picked up later in the week, with Baltic- and UK-origin deals contributing to the overall price rise.

While Turkish mills remained hesitant due to high scrap costs and expectations of price corrections, sentiment stayed firm. The market is expected to remain rangebound in the near term, with buyers and sellers closely watching global trade developments and post-Lunar New Year Chinese billet offers.

India: India’s imported scrap market remained under pressure as a weaker rupee, rising freight rates, and subdued steel demand dampened buying. Shredded scrap settled at $373/t CFR, down 1% w-o-w. The rupee’s depreciation made imports costly, while weak domestic steel support and an uninspiring Budget hurt sentiment.

Buyers largely stayed on the sidelines, leading to limited deal activity, with bid-offer mismatches persisting.

Suppliers favored Pakistan for better prices, while strong US domestic demand limited exports. Freight rates surged from $1,800/t to $2,400/t, further widening the bid gap.

Approximately 7,000-8,000 t of scrap were booked, including 4,500-5,000 t of HMS (80:20) from South America, Wes Africa, Chile, Mauritius, Australia has booked at $345-360/t and 1,500-2,000 t of shredded scrap from the Australia and Mauritius at $360-365/t, and 1,000-1,5000 t of MS Turning, HMS-LMS mix and Bushling scrap.

Pakistan: Pakistan’s imported scrap market remained sluggish due to weak construction demand and cash flow constraints. UK-origin shredded scrap settled at $383/t CFR, down 1% w-o-w. Prices softened to $380-385/t CFR Qasim, with deals closing at $375-382/t, while UAE-origin HMS held at $365/t CFR. LC-backed mills maintained moderate trade despite financial hurdles.

Traders anticipate a rebound by mid-February as Ramadan restocking begins, though sentiment remains cautious. Limited government projects kept steel demand weak, forcing sellers to adjust prices. Pakistan extended the 10% and 5% Regulatory Duty on flat steel products until March 2025, supporting domestic mills.

Bangladesh: Bangladesh’s imported scrap market remained stable but sluggish over the week, with UK-origin shredded scrap prices holding at $385/t CFR compared to the previous week. Early-week activity was driven by pre-Ramadan restocking, but sentiment turned cautious as weak construction demand and falling rebar prices led mills to slow down purchases.

Rebar prices dropped BDT 2,000/t, with Chattogram mills at BDT 86,000-88,000/t and Dhaka at BDT 82,000-84,000/t. LC constraints limited trade, favoring bulk shipments. Local scrap held at BDT 56,000-58,500/t, shipyard scrap at BDT 54,000-55,000/t. Mills remained cautious despite slight Ramadan restocking optimism.

A new eco-friendly steel plant in Chattogram boosts sentiment, enhancing domestic capacity and reducing import reliance. Near-term demand remains uncertain as buyers monitor market conditions.

Japan: H2 scrap export prices fell JPY 400/t ($3/t) to JPY 41,600/t ($274/t) FOB Tokyo Bay amid weak demand as buyers returned from holidays. Vietnam’s interest remained low, awaiting China’s post-holiday market trends.

Port congestion delayed shipments, pushing some February orders into March. Domestic H2 scrap prices averaged JPY 37,300/t ($246/t) in early February, down JPY 300/t ($2/t) w-o-w, with regional declines except in Kanto.

Vietnam: Vietnam’s imported scrap market remained cautious post-Tet holidays, with buyers monitoring China’s movements before setting bids. Some mills had sufficient stock from pre-holiday restocking, while others expected demand to pick up as January shipments were low.

South Korea: South Korea’s imported scrap arrivals surged to 109,750 t, rebounding from January’s 7,000 t, with 72% driven by plate and special steelmakers. Shaped steel demand remained weak due to sluggish construction activity.

Major buyers included Hyundai Steel, POSCO, and SeAH Besteel, while domestic scrap inventories at key mills fell 11% w-o-w. In response, Hyundai Steel and POSCO raised scrap purchase prices by KRW 10,000/t ($7/t) from 4 February, with further hikes possible if shortages persist.

US: US ferrous scrap export offers rose $6/t w-o-w, driven by higher US deep-sea offers to Turkiye. Exporters target $360/t CFR for HMS (80:20), expecting a $30-40/t surge in US scrap prices for February. Tight supply from cold weather and weak inflows pushed prices up, while US mills continued restocking despite sluggish steel demand.

Leave a Reply