- Turkiye’s scrap market bullish amid strong US sentiment

- India’s scrap market remains slow on weak demand

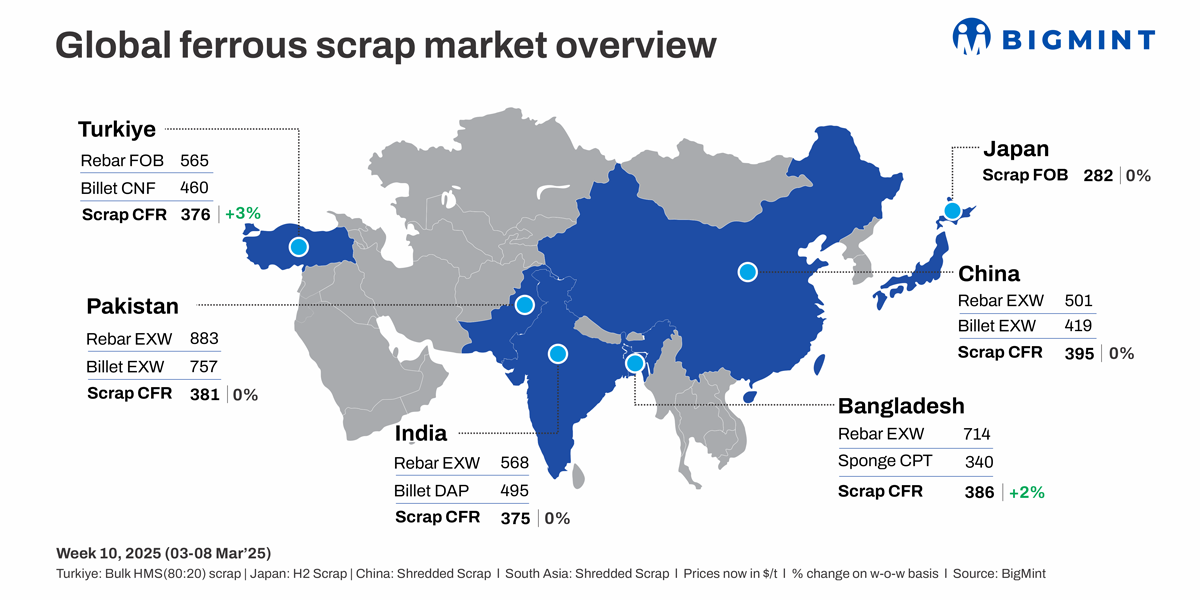

Global ferrous scrap offers remained stable, except for Turkiye and Bangladesh. Turkiye’s HMS 80:20 (US) rose to $376/t CFR, driven by tight supply and firm US sentiment. South Asia stayed sluggish due to Ramadan and liquidity issues, with limited deals in Pakistan, Bangladesh, and India. Japan’s H2 scrap edged up on strong demand, while Vietnam saw mixed activity.

Turkiye: Turkiye’s imported scrap market saw a steady upward trend throughout the week, with HMS 80:20 (US) CFR prices rising to $376/t, up 3% from last week’s $364/t. Mills remained cautious initially due to sluggish rebar sales and Ramadan-related slowdowns, while EU-origin deals were booked at $358-360/t CFR and US/Baltic-origin offers ranged between $360-365/t CFR. However, sellers held firm, citing strong US domestic market expectations and tight supply.

European recyclers raised offers beyond $370/t CFR, driven by a strengthening euro and rising collection costs. Turkish mills resisted higher prices due to squeezed margins but had limited bargaining power as export availability remained constrained.

By the end of the week, buying activity picked up as improving Turkish domestic rebar demand and an interest rate cut supported a bullish outlook. Multiple bookings from the US, EU, and Baltic suppliers reinforced expectations of further price increases in the near term.

India: The imported scrap market remained sluggish throughout the week due to weak demand, tight liquidity, and a widening bid-offer gap. UK/European shredded scrap offers stood at $375-380/t CFR Nhava Sheva, but bids remained lower at $365-370/t CFR, leading to limited deals. HMS 80:20 offers ranged between $350-355/t CFR, with buyers countering at $340-345/t CFR. No firm US-origin offers emerged due to high freight costs and unworkable price levels.

Indian buyers resisted higher scrap offers despite better steel sales, citing ample domestic supply and currency concerns. UK/EU-origin shredded and HMS remained unviable due to high costs. Holi and fiscal year-end further slowed activity, limiting fresh imports.

Approximately 5,000-5,500 t of scrap was booked, including 2,500-3,000 t of HMS 80:20 from the UK, Chile, New Guinea, Europe, and South Africa at $352-362/t. Additionally, 5,00-1,000 t of shredded scrap from Australia traded at $375/t, while 2,50-5,00 t of PNS scrap from the UAE at $380/t.

Pakistan: The imported scrap market remained sluggish as Ramadan dampened buying interest, compounded by weak liquidity, and subdued steel demand. Mills continued to resist higher offers, keeping bids below seller expectations. UK/European shredded was offered at $380-385/t CFR Qasim, but buyers targeted $375-378/t.

Rebar sales remained sluggish, with production at 45-50% capacity. Payment delays, liquidity issues, and Iranian scrap inflows pressured prices. Many melting units in Lahore and Gujranwala operated at lower levels or shut down for Ramadan and Eid, limiting fresh imports.

The UK-origin shredded prices CFR Pakistan stood stable at $381/t compared to $380/t last week. Market activity is expected to remain muted till Ramadan, after which demand may gradually improve.

Bangladesh: The scrap market remained sluggish as Ramadan slowed demand, construction activity, and LC openings. UK shredded stood at $386/t CFR, up 2%, but buyers resisted. Australian shredded was $380-385/t CFR, while Hong Kong PNS and HMS hovered at $375-380/t CFR and $360-365/t CFR.

Deep-sea bulk inquiries were limited as liquidity constraints and weak demand kept sentiment muted. Suppliers focused more on PNS and HMS rather than shredded, but a persistent $10/t price gap between bids and offers hindered deals. Malaysian busheling was offered at $385-390/t CFR, but buying interest remained low.

Despite slight improvements in LC conditions, overall demand stayed subdued. Traders anticipate a market recovery only after Ramadan, as construction and infrastructure activity is expected to pick up gradually.

Japan: H2 scrap export offers edged up w-o-w, driven by stronger demand, rising collection costs, and higher bids. Domestic FAS collection prices rose to JPY 40,000-41,000/t ($271-278/t). Lower Japan-Vietnam freights boosted exports, but some mills remained cautious. BigMint’s H2 scrap assessment increased by JPY 200/t to JPY 41,700/t ($283/t) FOB Tokyo Bay, supported by firm domestic prices and stable supply and demand.

Vietnam: The imported scrap market saw mixed activity as Japanese H2 offers rose to $325-335/t CFR, but bids stayed lower at $315-320/t CFR. A 5,000 t deal at $330/t CFR reflected some demand, supported by government-backed projects.

Deep-sea scrap prices weakened, with US- and Australian-origin offers at $360-365/t and $355/t CFR. Traders monitored China’s policies, anti-dumping measures, and billet pricing trends for market direction.

US: Ferrous scrap export prices climbed up by $11/t w-o-w, driven by tight domestic supply and strong Turkish demand. Firm seller sentiment and limited availability pushed US-origin HMS 80:20 bulk scrap higher across key destinations.

Leave a Reply