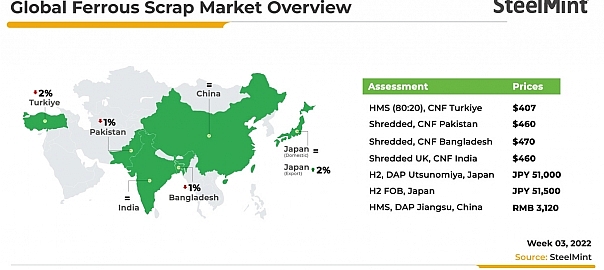

The global ferrous scrap market exhibited mixed trends. On one hand, the Turkish scrap market remained busy, recording low-priced deals, on the other hand, the Pakistan and Bangladesh markets were silent amid liquidity and L/Cs issues. Indian imported scrap trade slowed down even as prices remained supportive. Japanese scrap export prices and Vietnam’s imported scrap prices increased w-o-w.

Turkiye’s ferrous scrap prices down w-o-w: Turkiye’s imported scrap market improved slightly this week and several transactions were recorded. Interestingly, prices decreased by $10–15/t from the previous week in absence of active buying inquiries. A couple of deals for Baltic and Europe-origin were concluded towards the weekend at slightly lower prices.

Scrap collection was comparatively better in the overseas market amid clearer weather from the previous winter. A collection rate improving so does the export offers along with better supply in the domestic market, resulting in lower bids on a healthy supply chain.

SteelMint’s assessment for HMS 1&2 (80:20) from the US stood at $407/t CFR Turkey, down $11/t w-o-w.

Pakistan’s ferrous scrap market silent w-o-w: The imported scrap trade was mostly absent in Pakistan this week due to an unstable national currency in the exchange market and prices came down slightly w-o-w. Meanwhile, an inadequate cash flow amid low foreign reserves was forcing the government to limit the opening of new L/Cs.

SteelMint’s assessment for shredded imported scrap in containers stood at $460/t CFR, slightly down $5/t w-o-w.

Bangladesh trade mute amid L/Cs issues: Bangladesh’s ferrous scrap import market witnessed tight liquidity with certain L/Cs opening restrictions in the last few months which made buyers almost quiet, and only sporadic contracts for small tonnages were reportedly concluded.

Recently, the central bank issued a slight relief of a certain amount of one million dollars to support the steel industry to improve their pipeline and import raw materials.

SteelMint’s assessment for shredded scrap in containers stood at $470/t CFR, down by $6/t w-o-w.

India’s ferrous scrap market sluggish: Indian imported scrap buyers were active in the market but limited deals were concluded throughout the week. Prices were mostly stable at $455-460/t levels as buyers slowed down fresh bookings due to bulk cargo arrivals.

However, mills booked many slots from Middle East-based suppliers.

SteelMint’s assessment for the UK origin shredded scrap was at $460/t CFR Nhava Sheva, unchanged w-o-w.

Vietnam ferrous market silent w-o-w, prices up: As the Tet holidays are around the corner, the Vietnamese market for imported scrap remained quiet. Because most participants were preparing in the Tet (Lunar New Year) celebration, starting from 22 January 22, market sentiment was mostly negative and trading was practically absent. Participants, however, believe that after the holidays, the market will improve.

Prices for imported scrap continued to move up on material scarcity.

SteelMint’s assessment of US-origin bulk scrap was at $440/t CFR and Japanese H2 material at $430/t CFR, up $20/t w-o-w.

Japan’s scrap export prices increase w-o-w: This week, export prices of Japanese scrap increased somewhat. Trade operations were dismal due to slow demand from overseas buyers and the bid-offer gap. However, South Korean mills were only permitted to reserve a certain amount.

Scrap suppliers targeted a price of JPY 52,000/t ($401/t), while Korean steelmakers perceived JPY 49,000/t ($378/t) as a high price, so the gap between the two was known to be large.

SteelMint’s assessment for Japanese H2 scrap export prices stood at JPY 51,000-52,000/t ($394-402/t) FOB, moving up JPY 2,000/t ($15/t) w-o-w.

Leave a Reply