- Urban demand slump impacts India’s PV segment

- Japan’s H1 copper wire shipments hit 52-year low

At the close of trading on 18 July 2025, base metals prices on the London Metal Exchange (LME) saw positive trends w-o-w, with zinc witnessing the highest gain of 2.92% to $2,010/tonne (t). Meanwhile, LME warehouse stocks also exhibited positive trends, with zinc gaining the steepest, by 13.16%.

On the LME, three-month aluminium prices stood at $2,630/t, up by 1.04%, while nickel increased by 0.13% w-o-w to $15,218/t. Copper prices were at $9,779/t, up 1.22% w-o-w, and lead was down by 0.57% w-o-w to $2,022/t.

However, in India, various base metals markets remained range-bound or witnessed a downtrend due to localised factors.

India’s imported aluminium scrap prices remained range-bound w-o-w, supported by an uptrend in LME levels, strong global demand, and ongoing supply constraints. Limited raw material availability and firm price settlements by a leading automaker supported a modest uptrend in select grades.

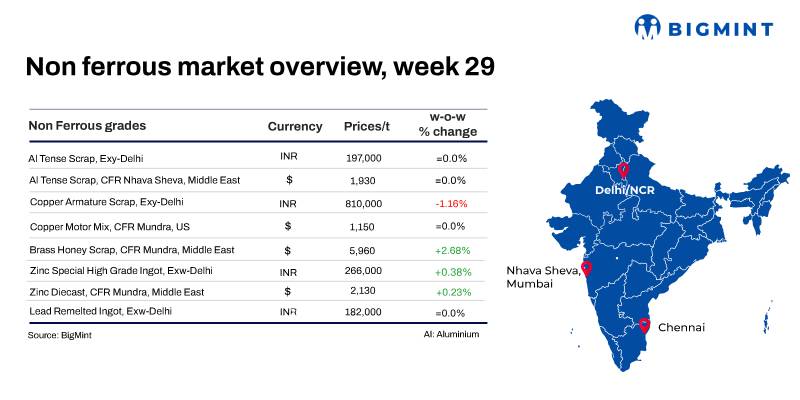

In the domestic market, Tense scrap prices in both Delhi and Chennai remained stable as compared to last week. According to BigMint’s assessment, domestic Tense scrap stood at INR 197,000/t ex-Delhi-NCR and INR 200,000/t ex-Chennai.

Additionally, a major Indian automaker raised its ADC12 settlement prices by INR 850/t m-o-m to INR 229,750/t for August, levels last seen in March 2022. The increase is driven by strong imported aluminium scrap prices and lower alloy imports.

Consequently, the scrap-to-ADC12 spread in July was largely stable at INR 32,000-33,000/t due to firm scrap prices.

India’s bauxite import volumes fell sharply by 76% y-o-y in Q1CY’25, to 0.31 million tonnes (mnt) from 1.29 mnt in Q1CY’24. Despite raw material volatility, India’s primary aluminium production remained steady. Output in Q1CY’25 rose marginally by 1% y-o-y to 1.05 mnt.

Indian copper scrap prices moved down further w-o-w, as LME futures remained lower than the three-month high of $10,005/t recorded on 3 July.

Copper armature scrap was assessed at INR 797,000/t ex-Delhi, down by 1.6% w-o-w, while motors mix stood at $1,150/t, largely stable w-o-w.

Domestic copper market sentiment remained dull, with ongoing monsoon conditions slowing down work across regions. Trading activity softened again, and most deals were concluded for smaller quantities, reflecting a cautious buying approach.

India’s quality control order (QCO) on copper cathodes is likely to reduce domestic availability due to what trade bodies call costly and unnecessary compliance burdens on foreign suppliers, according to the Bombay Metal Exchange (BME).

Secondary continuously cast rods (CCRs) (99.90%) were assessed at INR 851,000/t ex-Delhi, down 2.7% w-o-w. Meanwhile, primary CCR prices stood at INR 883,000/t, down 2% w-o-w.

India’s zinc scrap and dross prices remained range-bound w-o-w. Imported zinc diecast from the Middle East was assessed at $2,135/t CFR Mundra, up by $5/t w-o-w, while domestic zinc ingots stood at INR 267,000/t, up by INR 1,000/t w-o-w.

Prices of zinc ingots from Hindustan Zinc Limited (HZL) stood at INR 272,800/t ex-Chanderiya, up by INR 500/t w-o-w.

Domestic demand remained weak as galvanising activity slowed due to seasonal rainfall, and many secondary producers cited muted end-user demand. Meanwhile, scrap supply, particularly clean dross and high-purity ash, remained tight.

Lead

Domestic primary lead ingot prices remained steady w-o-w at INR 202,000/t, while re-melted ingots also remained stable at INR 182,000/t. Meanwhile, HZL lead ingots stood at INR 201,900/t ex-Chanderiya, down by INR 4,900/t w-o-w.

Other market updates

Japan’s copper wire shipments see first H1 decline since 1973

Japan’s copper wire shipments dropped 5.2% y-o-y to 287,090 t in H1CY’25, marking the first half-year decline in two years and the lowest since 1973. The fall was driven by a more than 10% drop in construction and electronics demand amid labour shortages and project delays. Automotive-related shipments rose 12.2% on higher vehicle production, but exports plunged 47.5% due to a high base effect.

Non-ferrous metals market faces global uncertainty amid tariffs, trade shifts

The non-ferrous metals sector faces continued uncertainty in 2025, driven by US tariffs, trade shifts, and supply chain disruptions, as noted in BIR’s July report. While India sees strong demand and rising scrap prices, China faces raw material tightness amid higher output. Geopolitical tensions are likely to impact Middle East trade, and the UK and Europe may grapple with supply and regulatory challenges.

Auto sales dip in Q1FY’26 as weak urban demand weighs on PVs

India’s total vehicle sales fell 5.1% y-o-y to 6.07 mnt in Q1FY’26, driven by sluggish urban demand and a 1.4% drop in passenger vehicle (PV) sales, which hit a two-year low in June. While utility vehicle sales rose 3.8% and exports across segments surged, domestic two-wheeler and PV markets saw pressure from moderated wage growth and supply chain issues, including rare earth shortages.

Leave a Reply