- Black Sea billet trade picks up as Turkish buyers return

- Chinese billet offers edge up despite cautious sentiment

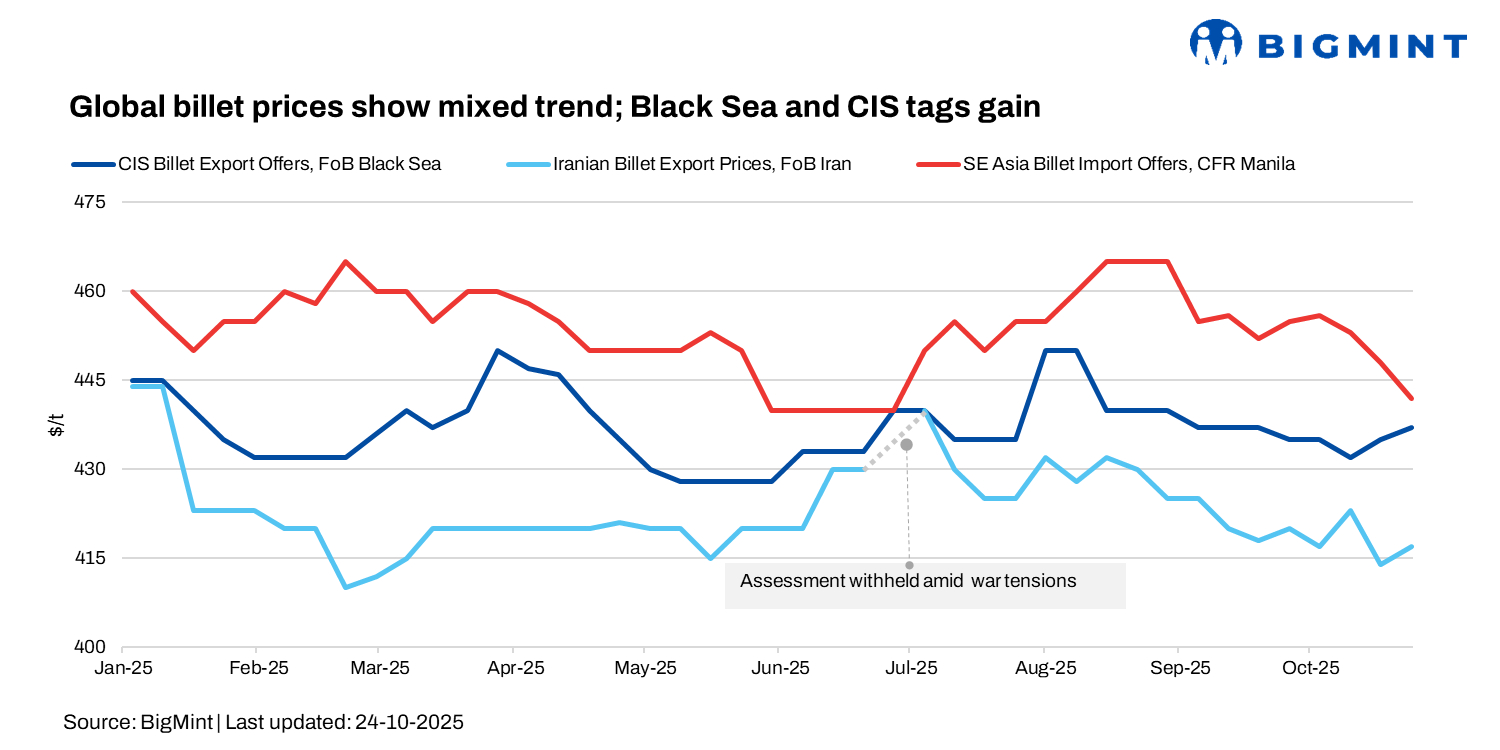

In week 43 of CY’25, global billet markets showed mixed movements. Black Sea Russian-origin billets for early December shipment were offered at $440-445/t FOB, with overall Black Sea export prices nudging up. In Turkiye, mills actively replenished stocks, booking CIS-origin semis at $455-460/t CFR ($435-440/t FOB), while Chinese and Malaysian billets traded in the $455-485/t CFR range.

In East Asia, Chinese 3sp billet bids held at $430/t CFR, with offers edging up to $440-445/t CFR Taiwan, amid cautiously optimistic market sentiment.

Deep-sea imported scrap in Turkiye eased slightly to $350-352/t CFR from $353-355/t last week, as weak steel demand and sluggish rebar sales kept mills cautious.

Market updates

Black Sea: Billet suppliers from the Black Sea region kept their offers steady this week, but trade picked up as Turkish buyers returned, pushing prices higher and making earlier offers more attractive. Overall, the Black Sea billet market saw a modest boost in activity, supported by returning Turkish demand and firmer scrap costs, while other regional export markets remained cautious amid regulatory and logistical challenges.

Russian billets for early December shipment were quoted at $440-445/t FOB, inching up from last week, though some mills remained open to small November cargoes (up to 10,000 t) or minor discounts for firm orders.

A temporary production halt at an exporting mill added to supply tightness, while weak overall buying interest limited further upward movement. Overall, Black Sea export prices were assessed up $2/t w-o-w at $437/t FOB.

Turkiye: Turkish mills actively replenished stocks amid improved market sentiment and rising scrap prices. CIS-origin billets were booked at $455-460/t CFR ($435-440/t FOB), with some negotiations concluding successfully. Major deals for Chinese billet were indicated at $455-457/t CFR, totalling around 70,000 t, while Malaysian billet trades were heard at $485-490/t CFR for roughly 50,000 t.

Domestic Turkish billet offers remained firm at $510-515/t exw, reflecting a cautiously optimistic market outlook.

Egypt, Tunisia: Egyptian buyers remained on the sidelines due to safeguard duties, with acceptable levels estimated near $440/t CFR ($400-410/t FOB). Tunisian buyers sought billets at around $460/t CFR ($420-430/t FOB), with offers under active consideration but no confirmed deals yet.

Taiwan: In the Far East, Chinese 3sp billet bids held steady at $430/t CFR, while offers edged higher to $440-445/t CFR, mirroring cautious optimism in the regional steel market.

Iran: Iran’s billet export market remained largely stable, as suppliers continued navigating currency-related hurdles. Key producers offered $415-420/t FOB for November-December shipments, while smaller mills and traders quoted $395-410/t FOB, keeping a wide price gap.

Esfahan Steel (ESCO) reportedly sold 30,000 t at $420/t FOB, while SISCO and IASCO floated new tenders for upcoming shipments. Industry representatives have urged a review of forex policies, disparities between main producers using the official NIMA rate ($1 = 72,000 toman) and traders transacting at the free market rate ($1 = 108,700 toman).

With mixed pricing and limited liquidity, export billet prices were assessed unchanged at $415-418/t FOB.

Saudi Arabia: Saudi Iron and Steel Company (Hadeed) raised November rebar offers by SAR 25/t ($7/t) to SAR 2,080/t ($555/t) delivered, marking a welcome reversal after months of pricing pressure.

The increase comes after mills lobbied for relief amid weak domestic demand, high costs, and tight margins.

Domestic semis were last seen at SAR 1,780-1,800/t ($475-480/t) exw, while rebar mills sold at SAR 1,880-1,900/t ($501-507/t). Scrap purchase prices fell SAR 15-30/t ($4-8/t) in major cities, easing cost pressure. As per Market Insider, sentiment is improving — mills finally have some breathing space.

China: China’s billet prices remained range-bound at RMB 2,930/t ($411/t), while SHFE January 2026 rebar contracts inched up by RMB 21/t ($3/t) to RMB 3,058/t ($429/t). The market remained sluggish, with weak rebar sales and subdued export activity leading to cautious sentiment.

Mills continued to face pressure from tight margins, with some reducing liquid iron output and planning blast furnace maintenance to balance supply. Despite minor destocking, inventories stayed high, while iron ore prices softened on fresh supply inflows. Prices may stay range-bound next week, moving within RMB 40-50/t, as muted trading and weak downstream demand persist.

Leave a Reply