- Iranian billet export prices rise in recent tender despite gas shortage in the domestic market.

- Lacklustre billet trade activity amid approaching Lunar holidays.

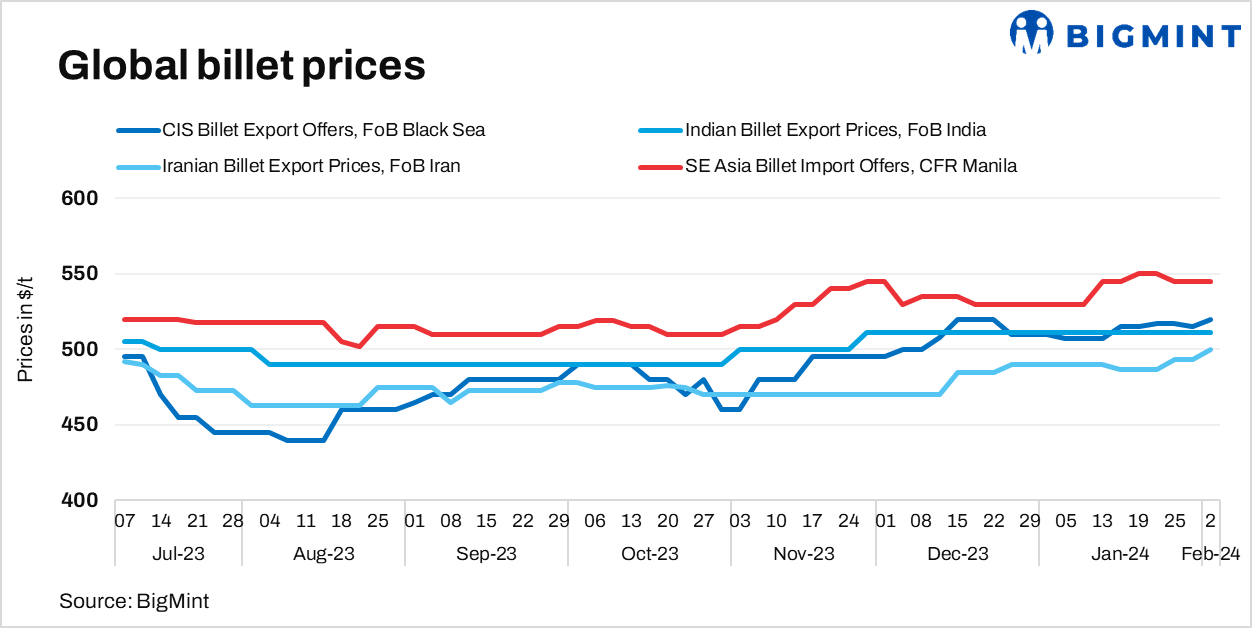

In the global market, billet prices have shown mixed sentiment this week. Billet players were active mainly in Iran amid electricity and gas shortage in the domestic market. Whereas, in the other region, trade activities are lacklustre due to approaching Lunar holidays, less production due to gas shortage in winter and weak sentiment on finished products.

Market highlights:

- Iranian billet export prices inch up by $8/t in recent trades: Iran’s billet export prices have surged in recent export deal with bids being received were at higher levels. An Iranian steel mill has concluded an export tender for 30,000 t of billets concluded at $500/t FOB, sources informed. Other Iranian mill SISCO has concluded an export deal of 20,000 t of billets at $500/t FOB, the shipment is for April. Prices increased by around $8/t against previous deal concluded last week amid shortage of electricity and gas. Meanwhile, Khouzestan Steel Company (KSC) had floated an export tender of 30,000 t for billet, which is yet to be concluded and the shipment is for April.

- Challenges weighing on Iranian steel exports: Industrial companies have been dealing with many challenges in the past years, one of the most important of which is the energy crisis in summer and winter, as per Mining News. During the last few years, severe energy imbalances have caused a drop in the level of production and exports and have faced many restrictions on mining and steel companies. In the current situation, the only solution to the problem and crisis of electricity and gas is investment growth in this sector, which, of course, cannot be implemented in the short term, but requires a long-term, multi-year plan after the removal of external restrictions. But with the current conditions of the economy and the critical situation of the energy sector and existing imbalances, it is unlikely that energy shortages will be resolved, and the steel industry will develop, quoted Mining News.

- SE Asia import billet offers remain range-bound w-o-w: Southeast Asia imported billet offers remained stable this week. Billet players are inactive due to ongoing Lunar New Year holidays, additionally they are pressurised due to weak sentiment of finished products. Notably, absence of trades in the region is seen amid dull buying interest in the global market. The offers for the 5 SP grade imported billet remained constant at $545-555/t CFR Manila w-o-w. However, the bids for 5 SP were reduced by $5/t w-o-w, standing at around $530-540/t CFR on 2 February.

- Thailand’s imported billet offers remain range-bound: Imported billet offers from the ASEAN region into Thailand remained range-bound at $545-555/t CFR Thailand.

- Indonesian steelmaker Dexin Steel has hiked its offering by $5/t w-o-w, currently at $535/t FOB, as per sources. Buying activities are soothing ahead of Chinese New Year holiday and most mills are trading far away from the region in the countries like Turkey and Latin America.

- Chinese billet prices inch down w-o-w: Chinese billet prices inched down by RMB 100/t ($14/t) w-o-w to RMB 3,550/t ($500/t) on 2 February. Billet prices have declined following the downtrend of rebar futures and low consumption of raw material during holidays. Meanwhile, Chinese SHFE rebar futures decreased by RMB 142/t (20/t) w-o-w to RMB 3,825/t ($539/t) today.