- Asian export prices rise on China futures strength

- Iranian billet holds steady under new forex regime

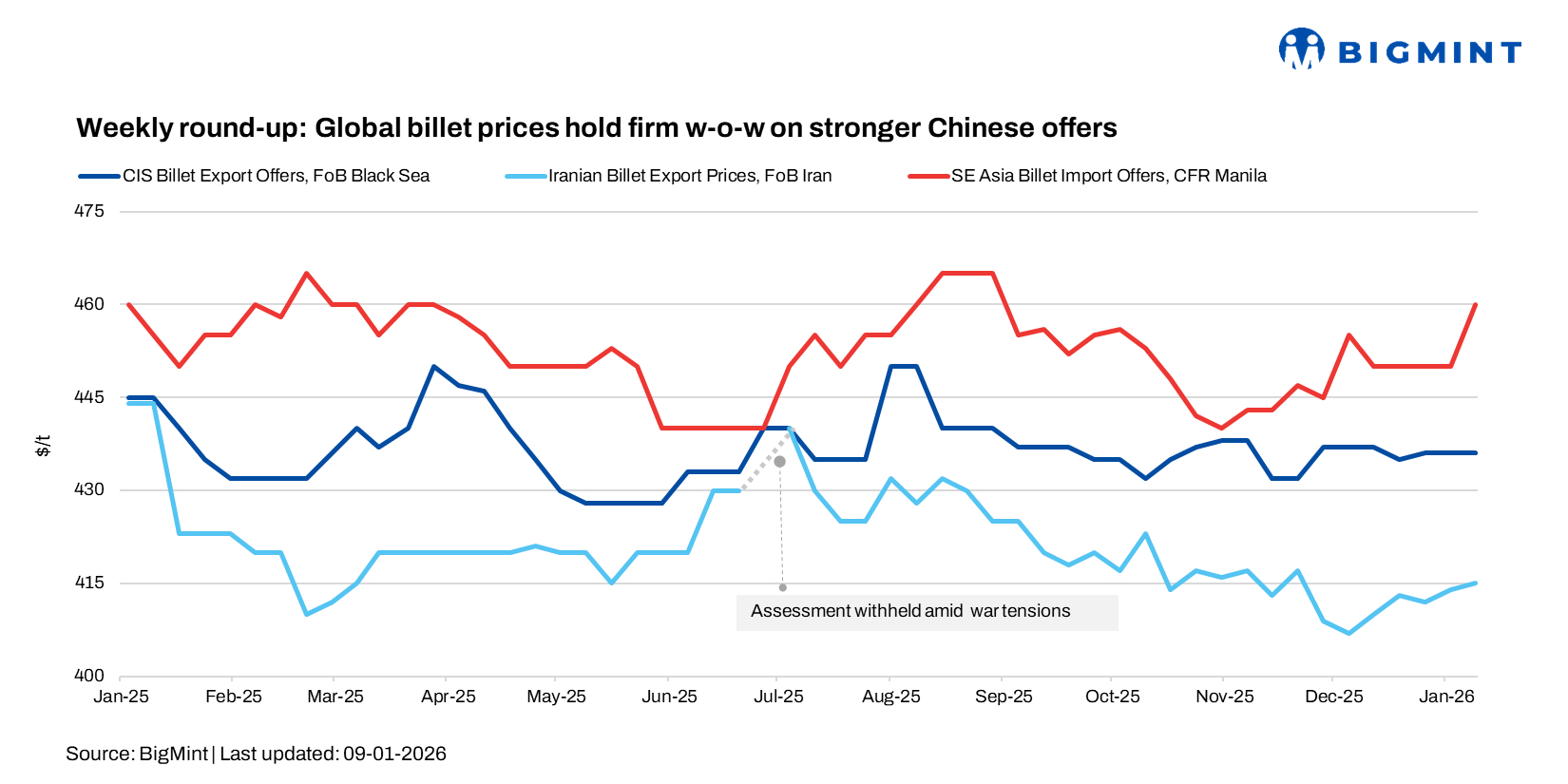

Global billet prices firmed up in the week ended 9 January 2026, though buying interest remained selective, particularly across the CIS, due to lingering year-end holiday slowdowns.

Asian billet export prices strengthened over the past two weeks, supported by improved sentiment in the Chinese steel market and gains in futures, prompting sellers to test higher levels while buyers stayed cautious.

In Turkiye, the deep-sea imported scrap market edged up marginally, underpinned by tight seasonal supply and firm seller sentiment, despite weak rebar demand. Early-week activity was subdued due to holidays, with European HMS 80:20 around $365/t CFR and US-origin material at $370-372/t CFR. By late week, US-origin offers rose to $375-380/t CFR on supply tightness and higher freight costs.

Asian billet market

Asian billet export prices firmed up over the past two weeks, tracking improved sentiment in the Chinese steel market and gains in futures. However, buying interest remained subdued, with most importers adopting a wait-and-see approach and resisting the higher prices.

Chinese mills raised offers for 3sp billet to around $445-448/t FOB for March shipment from $435-440/t FOB two weeks earlier. The increase was largely futures-led, but bids remained scarce as buyers monitored market direction.

In the Philippines, Chinese 5sp billet offers rose by about $10/t to $460/t CFR, though the higher tags failed to attract interest. Similarly, in Thailand, Chinese 3sp billets were offered at $460/t CFR, compared with $450-455/t CFR earlier, while workable bids were heard closer to $450/t CFR.

Chinese billet prices witnessed an RMB 40/t w-o-w rise — ending marginally higher despite mid-week volatility. Prices opened at RMB 2,930/t ($419/t) on 2 January and closed at RMB 2,970/t ($425/t) on 9 January.

CIS billet market

Turkish billet market activity remained subdued amid the usual early-year slowdown. In an attempt to stimulate demand, Kardemir launched a mid-week sales round, cutting billet prices by $5/t from its previous sale three weeks earlier. The mill offered 150×150 mm S235JR billets at $500/t exw and quickly sold around 47,000-48,000 t, highlighting strong price sensitivity rather than a genuine recovery in consumption.

The price adjustment reflects weak finished steel demand, with rebar reportedly trading at discounts of $5-8/t due to a winter-led slowdown. Other domestic billet offers stood near $510/t exw, down from $515-520/t exw in late December, while some mills paused operations for 15-20 days.

In the import market, Malaysian billets were available at about $505/t CFR for March shipment, while Chinese material for February was offered lower at $470-475/t CFR, increasing competitive pressure on local producers.

GCC billet market

Procurement interest in Saudi Arabia’s billet market improved after the holidays, but negotiations stalled as suppliers pushed for higher prices and buyers remained cautious. Chinese billet offers edged up to $473-479/t CFR from $465-470/t CFR, discouraging fresh buying amid weak downstream demand.

Domestic billet pricing remained unsettled, with mills yet to finalise scrap procurement. Cost pressure increased after the benchmark mill raised scrap prices from 5 January: premium at SAR 1,445/t ($376/t), shredded at SAR 1,440/t ($374/t), and HMS 1&2 (80:20) at SAR 1,375/t ($358/t).

In the finished segment, first-tier mills raised January rebar offers to SAR 2,140-2,145/t ($556-558/t) delivered, while smaller mills quote SAR 2,000-2,030/t ($520-528/t). Billet buying is expected to hinge on whether these higher rebar prices hold.

Iran billet market

Despite persistent political and economic headwinds, Iranian billet exporters witnessed improved export incentives following the introduction of a unified exchange rate for currency repatriation. While the market is still adjusting and offer activity remained cautious amid currency volatility, the new framework has lifted export realisations for mills compared with earlier official-rate conversions.

Iranian export billet prices remained stable at around $415-420/t FOB over the past two weeks. Khouzestan Steel Company (KSC) concluded a billet tender at $410/t FOB for mid-February shipment, selling about 50,000 t in late December. In slabs, Mobarakeh Steel targeted $425/t FOB for February production, though sources were uncertain whether reported volumes were fully sold, with additional tenders expected later in January.

Leave a Reply