- Geopolitical uncertainties lead to cautious sentiment

- Ample production causes price corrections in China

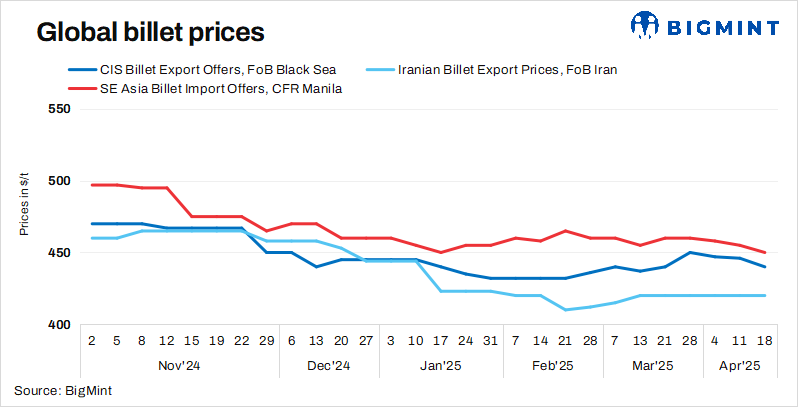

The global billet market remained under pressure in week 16 of CY’25, as subdued downstream demand, particularly for rebars, continued to weigh on buying activity. Market participants across key regions displayed caution, with geopolitical uncertainties and trade-related headwinds further dampening sentiment. As a result, major regions saw a fall in prices, pressured by a fragile market environment. Sellers increasingly adjusted offers downward in response to limited spot interest and muted procurement activity.

Meanwhile, scrap availability remained high at key Turkish docks, with major suppliers holding sizeable cargoes ready for shipment. However, mills such as Isdemir, Erdemir, and Asil Celik remained largely inactive in the spot market, correcting their scrap purchase prices by about $3-6/t due to persistently weak rebar demand and tight steel margins. Even though mills require scrap for May production schedules, the lack of end-user interest in finished steel dampened buying urgency. Amid this backdrop, US-origin HMS 80:20 bulk scrap was assessed at $345/t CFR Turkiye, reflecting a $25/t w-o-w decline, as sellers faced growing pressure from mills aiming to push prices lower.

Market highlights

SE Asian imported billet prices fell w-o-w amid rising concerns over trade tensions and potential tariffs on Chinese steel exports. Regional buyers remained cautious due to weakening Chinese prices and shifting trade dynamics. However, raw material tags also declined, contributing to a fall in the prices of steel. Offers for 150 x 150 mm, 5SP billets to the Philippines were heard at $445-450/t CFR Manila as of 18 April, down $5/t from the previous week. Additionally, billet offers were at $450/t CFR Manila, according to sources. The Taiwan market also saw price reductions due to weak downstream trade flow dynamics.

Vietnam’s billet market saw fewer offers, with most traders refraining from providing material. Vietnam’s blast furnace (BF) grade billet export offers fell by $10/t w-o-w to $450/t FOB on 18 April. Additionally, BigMint’s Russian billet index FOB Black Sea dipped $6/t w-o-w to $440/t from 11 April.

The Iranian billet market resumed following the Eid and Nowruz holidays, with participants gradually returning to the trading floor. Prices remained unchanged w-o-w at $420/t FOB on 18 April, with most suppliers holding back offers for pending tender results.Sellers targeted prices of $425/t FOB. Players awaited the tender results of KSC and Arfa Iron and Steel Co., each of which offered 30,000 t.

Chinese billet prices fell by RMB 30/t (4/t) w-o-w. Steel billet prices in Tangshan, China, dropped by RMB 30/t ($4/t) w-o-w to RMB 2,940/t ($403/t), including 13% VAT, on 18 April. The market remained fragile amid high crude steel output and ongoing rumours of a potential tariff hike from the US, keeping sentiment mixed. Daily trade volumes hovered at around 110,000-130,000 t, while inventories hit a two-month low. Prices remained largely range-bound throughout the week, fluctuating between RMB 2,970-2,940/t. Meanwhile, SHFE rebar futures (October 2025 delivery) declined by RMB 55/t ($8/t) to RMB 3,076/t ($421/t), signalling caution in the market amid sluggish trading and limited downstream demand.

Leave a Reply