The global steel billet market remains lacklustre amid absence of tenders due to weak market sentiment. BigMint observes that market participants are opting for a wait-and-watch strategy during the monsoon season, weak rebar market, and sluggish buying interest in the global market.

Market highlights

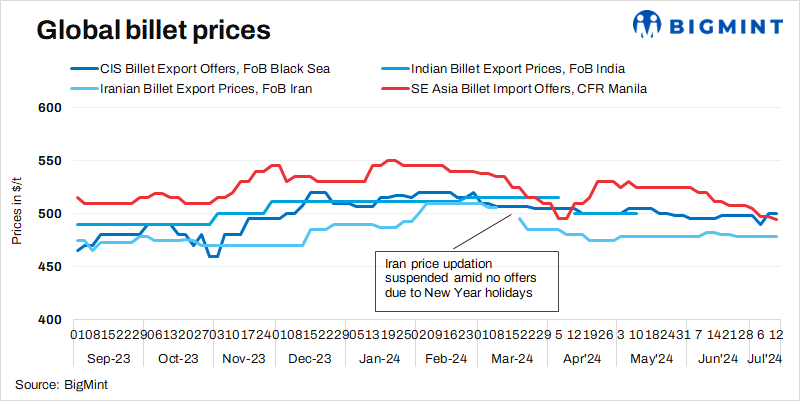

- SE Asia billet import prices fall w-o-w: South East Asia’s imported billet prices stayed supported due to lack of tenders in the region. Meanwhile, market participants have adopted a wait-and-watch strategy due to the lack of price clarity amid weak steel market sentiment. In addition, billet (150x150mm, 5SP) offers are at the range of $495-500/tonnes (t) CFR Manila and bids are around $490/t CFR Manila. According to BigMint’s bi-weekly assessment, billet (150x150mm, 3SP) imported by the Philippines currently stands at $494/t CFR Manila, a decrease of $3/t compared to the last assessment on 5 July.

- Indian billet export prices remain silent: Indian billet export market has remained subdued. The recent tenders floated have remained inconclusive, as domestic billet prices are higher as compared to the global billet prices.

- Vietnam’s billet export offers unchanged w-o-w: Vietnam’s BF-grade billet export offers remained unchanged w-o-w at $490/t FOB. As per sources, domestic market is witnessing weak demand.

- Iranian billet export remains stable w-o-w: Iran’s billet export market continued to remain muted this week amid absence of export tender. As per sources, billet offers are at $480/t FOB. According to BigMint’s bi-weekly assessment, Iranian billet export prices were assessed at $478/t FOB, stable w-o-w.

- China’s steel billet prices decrease w-o-w: Billet prices in Tangshan dropped by RMB 20/t ($3/t) w-o-w to RMB 3,290/t ($454/t) on 12 July. Volatility in raw materials, finished steel prices, rebar futures throughout the week weighed on billet prices. Prices include 13% VAT. SHFE rebar futures (October, 2024 delivery) decreased by RMB 30/t ($4/t) w-o-w to RMB 3,523/t ($485/t) on 12 July.

Leave a Reply