- Japan’s aluminium premiums expected to decline in Q4CY’25

- Indian zinc prices edge up as LME stocks continue to decline

At the close of trading on 5 September 2025, base metals prices on the London Metal Exchange (LME) showed mixed trends w-o-w, with zinc witnessing the highest gain of 1.53% to $2,861/tonne (t). Meanwhile, LME warehouse stocks exhibited contrasting trends, with zinc witnessing the steepest decline of 20.60%.

On the LME, three-month aluminium prices stood at $2,601/t, down by 0.91% w-o-w, while zinc increased by 1.53% to $2,861/t. Copper prices were at $9,898/t, up by 1.03% w-o-w, and lead was down by 0.50% w-o-w at $1,985/t. Nickel stood at $15,235/t, up by 0.89% w-o-w.

India’s imported aluminium scrap prices saw mixed trends w-o-w, despite range-bound LME prices.

BigMint assessed Tense scrap from the US at $1,960/t, largely stable w-o-w, while US Taint Tabor HRB (2-3%) was down $5/t, at $2,155/t.

Global primary aluminium output remained stable at 36.4 mnt in H1CY’24, up a minor 1.4% y-o-y, amid macroeconomic challenges and trade frictions

Imported copper scrap prices in India saw a positive trend w-o-w, following a slight gain in LME futures to $9,898/t. Meanwhile, domestic copper scrap prices were stable w-o-w.

According to BigMint’s assessment, Birch Cliff scrap was assessed at $9,260/t, down by $30/t w-o-w, while US motors mix stood at $1,170/t (both CFR Mundra), largely stable w-o-w.

India’s copper pipes and tubes imports increased 21.4% y-o-y in 7MCY25 to 77,080 t, while wire imports were steady, rising just 1% y-o-y to 97,168 t versus 96,007 t last year.

Zinc

India’s zinc scrap and dross market remained steady this week, with prices moving in a narrow band.

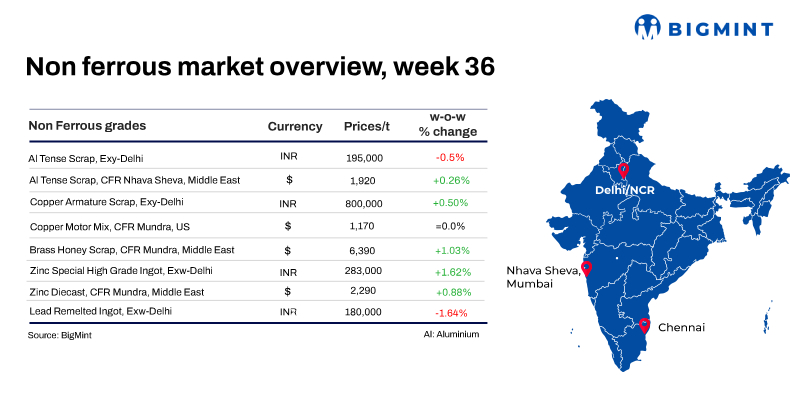

Domestic zinc spot prices edged up by 1.6% w-o-w to INR 283,000/t exw-Delhi. HZL zinc prices were up by 2.8% w-o-w to INR 295,400/t exw-Rajasthan.

LME zinc inventories continued their sharp decline during the week, falling to 54,050 t on 6 September from 56,500 t on 29 August. This sharp destocking indicates tightening global supply of readily available zinc and provided strong support for prices.

Lead

Domestic primary lead ingot prices stood at INR 202,000/t, down by INR 1,000/t w-o-w, while re-melted ingots stood at INR 180,000/t, down by INR 3,000/t w-o-w.

Globally, supply remained uneven. Smelter curtailments in South Korea’s Seokpo smelter (58-day shutdown) and reduced production at Nyrstars’ European plants tightened regional availability. In contrast, China’s secondary lead output rose 6% y-o-y to 4.67 million tonnes (mnt) in January-July 2025, with August run-rates expected to push growth to 7% y-o-y, offsetting overseas supply disruptions.

Other updates

Indian aluminium extrusion industry struggles as imports surge

India’s aluminium extrusion industry is facing a crisis, with 28 units shut and nearly 5,000 jobs lost in the past two years due to cheap imports and the impact of free trade agreements (FTAs), ALEMAI warned. Despite having a 3 million tonne per annum (MTPA) capacity, the sector is running at just 1.2 MTPA as imports cross 1.5 MTPA annually. The association has urged the government to exclude extrusion products from FTAs, boost billet production, and support MSMEs, stressing that without safeguards, smaller players will collapse while larger producers benefit.

Japan Q4 aluminium premiums expected to decline

Global aluminium producers proposed Q4 premiums of $98-103/t to Japanese buyers, down 5-9% from Q2’s $108/t. This follows a sharp 41% cut in Q3 amid weak demand from automotive and construction sectors. Improved global supply and volatile LME prices strengthened buyers’ bargaining power, pressuring producers to accept lower premiums despite soft market fundamentals.

Leave a Reply