- PELLEX, coking coal tags inch up w-o-w

- IF-route rebar prices show mixed trends

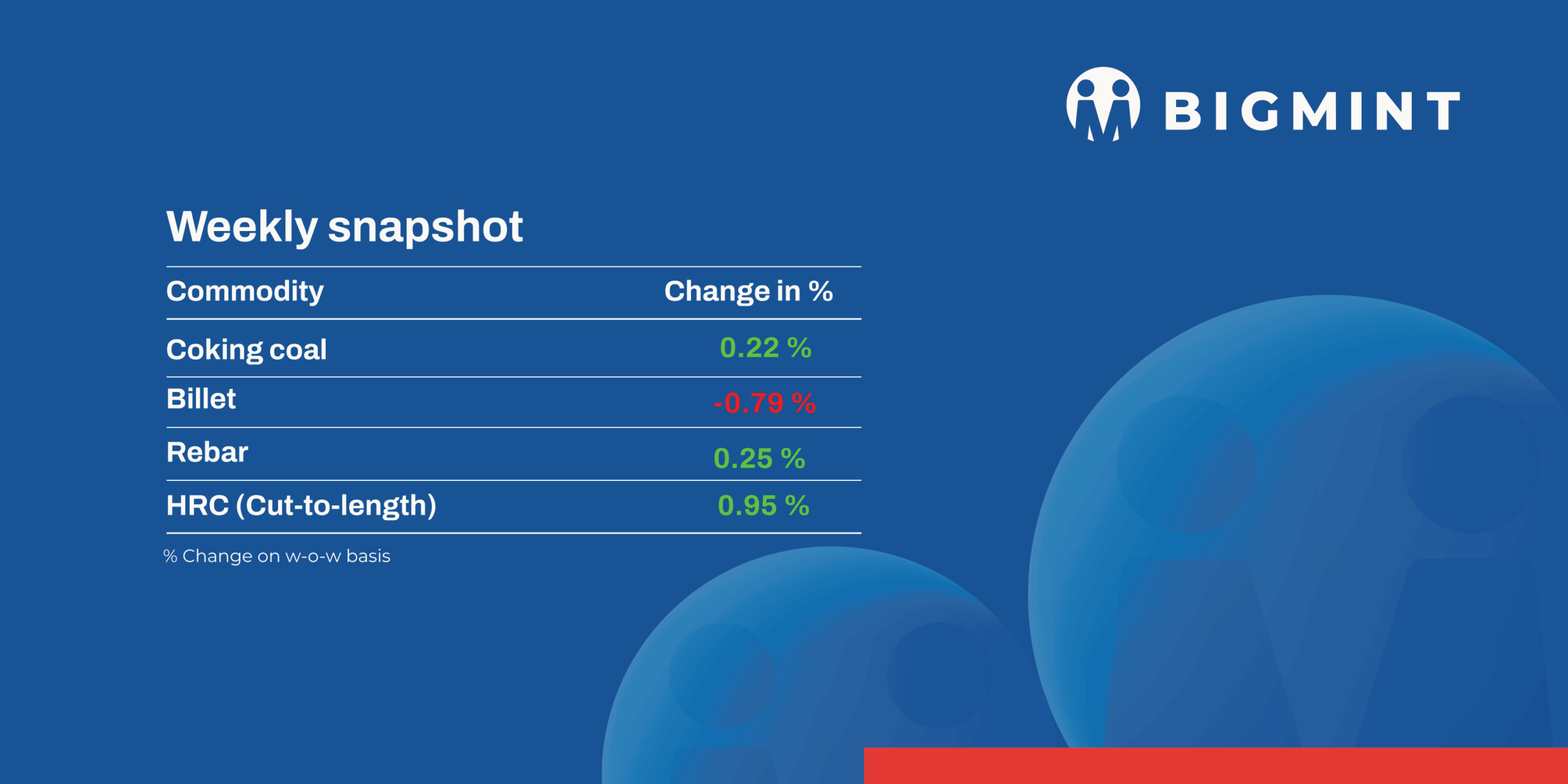

Domestic steel and raw material prices witnessed mixed trends during Week 31 (2 August-8 August 2025). Meanwhile, primary mills raised list prices of hot-rolled coils (HRCs), cold-rolled coils (CRCs), rebars by up to INR 2,000/t, suggesting a market rebound may be in store.

Iron ore, pellet

- PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, inched up by INR 50/tonne (t) w-o-w to INR 10,100/t ($115/t) DAP Raipur on 8 August. Raipur-based producers maintained their offers for Fe 63% (+/-0.5%) at stable levels of INR 9,900-10,000/t ($113-114/t) exw. Deals for around 100,000 t were concluded over the last few days by local pellet suppliers.

- NMDC Chhattisgarh conducted an auction for 17,200 t (10-40 mm, Fe 67%) of iron ore DRCLO from its Bacheli mines on 7 August. The entire volume was booked at INR 7,520/t (INR 620/t premium) against the revised base price of August INR 6,900/t. Prices were on FOR basis, inclusive of royalty, DMF, and NMET.

- NMDC auctioned 344,000 t of iron ore from its Kumaraswamy mines in Karnataka on 6 August. The entire quantity was booked, fetching premiums of up to INR 800/t. Notably, 112,000-t lumps (10-40 mm, Fe 58.93-60.91%) were sold at INR 4,483-5,323/t against base prices of INR 4,178-4,753/t. 232,000-t fines (Fe 56.21-60.83%) were booked at INR 2,892-4,146/t against base prices of INR 2,892-3,986/t. Prices include royalty, DMF, and NMET.

Coal

- South African RB2 thermal coal offers held firm w-o-w at INR 8,100/t exw-Gangavaram, while RB3 eased by INR 50/t to INR 7,000/t. Offers reflected September delivery sentiment, as August cargoes are mostly booked. Around 5,000 t of RB3 were traded at INR 7,200/t from Mangalore and 8,000 t at INR 7,000/t exw-Paradip. Stocks fell 3.4% to 14.27 million tonnes (mnt). Export offers were up by $0.5-1.5/t w-o-w; domestic coal and sponge iron markets showed mixed signals.

- Domestic coal prices remained firm w-o-w as SECL supply stayed constrained amid monsoon disruptions. BigMint assessed 5000 GCV at INR 5,000/t exw-Bilaspur, unchanged from last week, while 4500 GCV rose INR 100/t to INR 4,500/t. SECL’s reduced e-auction frequency and positive response in recent auctions lent support to prices despite weak overall demand. Traders expect continued firmness until supply conditions improve post-monsoon.

- BigMint’s PHCC index rose $5/t w-o-w to $199/t CNF Paradip as of 8 August 2025, backed by a recent deal for 25,000 t of Australian Goonyella cargo. Market sources placed Australian PHCC at $197-200/t and Canadian at $180-185/t CFR. Indian met coke prices stayed supported, while Chinese prices firmed up on strong steel demand. Seaborne PHCC offers held at $183/t FOB amid tight vessel availability and sustained Asian buying.

- India’s met coke market shows early signs of bullishness, supported by rising coking coal and Chinese met coke prices. Domestic blast furnace (BF) grade coke stayed flat at INR 29,000/t in the east, while western prices inched up to INR 30,000/t. Tight supply, delayed imports, and higher seaborne coal costs lifted sentiment. A weaker rupee and steady pig iron rates further supported prices. An uptick is likely in the near term until imports arrive in September.

Ferrous scrap

- India’s imported scrap market remained slow, with shredded EU origin prices slipping 1% w-o-w to $364/t from $368/t this week, as mills opted for domestic scrap due to better cost-efficiency and weak finished steel demand. Only limited deals were concluded, with most buyers hesitant to accept higher imported prices.

- Australian HMS 80:20 was discussed in the range of $335-340/t CFR, but with most cargoes headed to Southeast Asia, availability for India remained limited.

- European shredded was heard to be workable at $365/t, but bids stayed near $360/t. According to market participants, local end-cutting scrap at INR 33,000/t ($377/t) FOR offered better landed costs. Additionally, currency volatility and freight costs discouraged fresh bookings.

Ferro alloys

- Silico manganese: Indian silico manganese prices (60-14) dropped by INR 975/t ($11/t) w-o-w to INR 70,400-71,300/t ($803-814/t) in the key regions of Durgapur, Raipur, Raigarh, and Vizag. Domestic silico manganese sellers faced weak demand and surplus supply, with limited export interest due to uncertainty over EU safeguard duties and unclear implementation timelines.

- Ferro manganese: Indian ferro manganese (HC 70%) prices remained steady with a slight rise of INR 100/t ($1/t) w-o-w to INR 70,700/t ($807/t) exw in Durgapur. However, prices, exw-Raipur, were unchanged w-o-w at INR 70,700/t ($807/t). Despite weak demand, ferro manganese prices stayed flat, supported by stable supply and rising costs of high-grade manganese ore.

- Ferro silicon: Indian ferro silicon prices declined by INR 2,400/t ($27/t) w-o-w to INR 95,000/t ($1,084/t) exw-Guwahati. Meanwhile, Bhutanese prices increased by INR 3,400/t ($39/t) to INR 95,000/t ($1,084/t) exw. Prices declined after Bhutan announced an exw rate of INR 95,000/t ($1,082/t) for the month, and Meghalaya-based plants resumed operations.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices rose by INR 500 ($6/t) w-o-w to INR 100,500/t ($1,147/t) exw-Jajpur, supported by limited supply and a modest recovery in demand, though stainless steel demand remained weak.

Semi finished

- Indian semi-finished steel prices showed a fluctuating trend, as per BigMint’s assessment. Domestic billet prices were down by INR 50-200/t in most regions while shooting up by INR 50-500/t in others. Sponge iron prices also showed mixed trends, with most locations recording a drop of INR 100-400/t, while Mandi Gobindgarh and Bellary witnessed an uptrend of INR 100/t.

- Indian direct reduced iron (DRI) export offers increased by $4/t w-o-w to $338/t CPT Raxaul, while CPT Benapole ones increased by INR 1/t to $332/t.

- NMDC’s steel plant in Nagarnar, Chhattisgarh, auctioned 10,000 t of steel-grade pig iron on 7 August, with the entire quantity getting booked at an average price of INR 32,400/t (by road). However, management approval is still pending. Bids increased by INR 950/t from the previous auction on 17 July for 10,000 t, in which the entire quantity was booked at an average of INR 31,450/t (by road).

Finished long steel

- IF-rebar: India’s induction furnace-route rebar prices witnessed mixed trends. Buying activity was largely limited to immediate requirements. However, manufacturers preferred to either adjust trade discounts or reduce prices to encourage sales. Inventory levels stood at around 8-12 days, although this varied region-wise. Additionally, the lifting of previously booked materials was smooth. Market participants expect the market to remain range-bound in the near term.

- On a w-o-w basis, rebar prices varied in the range of INR 100-700/t across regions, as per BigMint’s assessment.

- Trade reference prices of Fe 500 grade rebars manufactured via the IF route for 10-25 mm size were assessed at INR 39,600-40,000/t exw-Raipur and INR 43,700-44,300/t exw-Jalna.

- Trade reference prices of heavy structural steel for base size 150-mm channel stood at INR 42,500-42,900/t exw-Raipur.

- Trade reference prices of wire rod hovered at INR 41,000-41,500/t ex-Raipur.

- BF-rebar: Indian primary mills increased rebar prices by up to INR 2,000/t ($23/t) for early-August 2025 deliveries as against prices prevailing in end-July, sources informed BigMint. Post-revision, list prices stood at INR 48,500-50,000/t ($552-569/t) on landed basis.

- Trade-level BF rebar prices increased by INR 800/t ($9/t) w-o-w to INR 48,800/t ($557/t) exy-Mumbai, as per BigMint’s assessment on 8 August 2025. Prices are exclusive of GST at 18%.

- In the projects segment, prices increased w-o-w to INR 48,000-49,000/t ($548-559/t) FOR Mumbai.

Flat steel

- Leading Indian steel manufacturers have officially raised the list prices of HRCs and CRCs by INR 1,000-2,000/t ($11-23/t) for August 2025 sales as compared to the net sales price of end-July 2025.

- BigMint’s India hot-rolled coil (HRC, S275) export index rose by $5/t w-o-w to $540/t (FOB main port), supported by improved global market sentiment and higher Chinese export offers.

- Chinese HRC export offers rose by $12/t w-o-w to $490/t against $478/t a week ago. The rise in prices is attributed to the increase in SHFE futures, as well as expectations of tighter steel supply and large-scale project investments. This upward movement in Chinese prices has lent support to Indian domestic sentiment as well.

- India’s bulk imports of HRCs touched 484,879 t in July 2025, a rise of 50% against 322,329 t in June based on vessel line-up data. Around 222,696 t of additional cargoes are expected by the second week of August.

- India’s bulk exports of HRCs touched 127,396 t as of July, declining by 8% m-o-m against 138,868 t in June based on vessel line-up data with BigMint. Moreover, around 51,620 t of additional cargo are expected in August.

Leave a Reply