- Tier I mills hike HRC, CRC list prices for Jan’25

- IF rebar tags fall w-o-w on muted trade activities

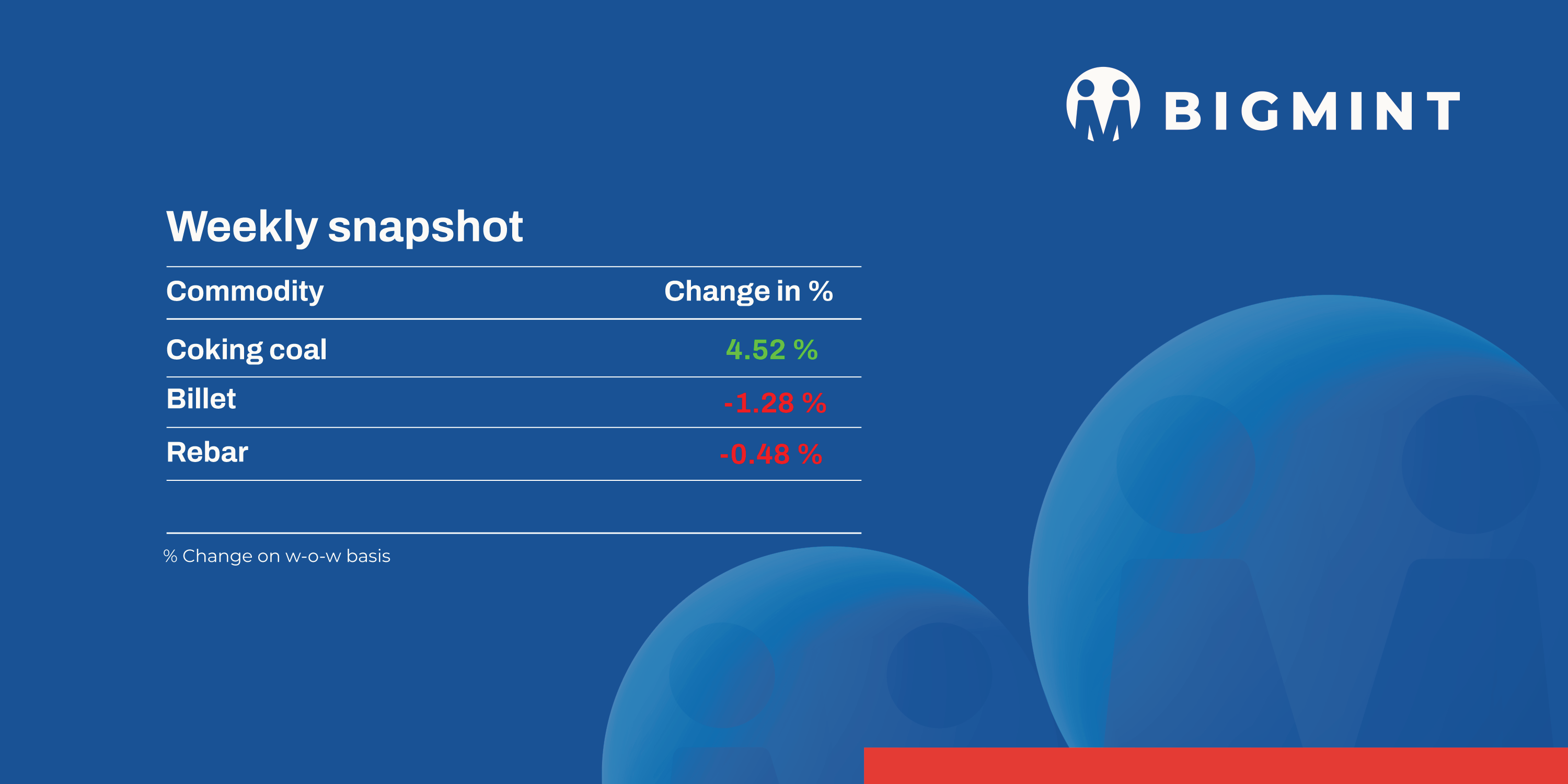

The domestic steel market witnessed a negative trend in prices during week 2 (6 January-11 January 2025). Semi-finished steel prices fell in the range of INR 300-1,300/tonne (t).

Iron ore, pellet

- NMDC reduced list prices of iron ore calibrated lump ore (CLO) and fines by INR 350/t ($4/t), effective 9 January, BigMint learnt from sources. The miner fixed prices of DR CLO (10-40 mm, Fe 67%) at INR 7,070/t ($82/t) and of iron ore fines (-10 mm, Fe 64%) at INR 5,060/t ($59/t) on FOR basis from its Bacheli complex. Prices include royalty, DMF, and NMET charges.

- BigMint’s bi-weekly domestic pellet (Fe 63%) index, PELLEX, decreased by INR 100/t w-o-w to INR 9,450/t DAP Raipur on 10 January 2025. The Raipur pellet market was stable amid weak market sentiments and a lack of buying interest. Trade activity remained at a standstill, largely because of the decrease in NMDC’s iron ore tags and a notable drop in sponge iron and billet prices in the region.

- BigMint’s weekly index for Karnataka iron ore fines (Fe57%) fell by INR 100/t ($1/t) w-o-w to INR 2,950/t ($34/t) ex-mines Bellary (excluding taxes). Similarly, the Fe 62% fines index was assessed at INR 4,950/t ($58/t) ex-mines Bellary, including taxes, down by INR 50/t ($0.5/t) w-o-w. However, some offers were noted at slightly elevated levels of INR 5,000-5,300/t ($58-62/t) due to limited supplies of high-grade ore. However, prices were significantly higher when evaluated against current market trends.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index stood at $60/t FOB east coast, India, on 9 January 2025. The index fell marginally by $1/t w-o-w. No iron ore export deals were recorded this week amid subdued market sentiments and cautious trading by participants. India’s pellet (Fe 63%, 3% Al) export index (FOB east coast) fell by $1/t w-o-w to $94/t on 10 January.

Coal

- India’s portside prices of South African thermal coal dropped this week, amid reduced sponge iron prices and sufficient port inventories. RB2 (5500 NAR) prices slipped by INR 300/t w-o-w to INR 8,950/t, while RB3 (4800 NAR) prices fell by INR 350/t w-o-w to INR 7,300/t, both ex-Gangavaram. Weak buying interest amid lower sponge prices and abundant domestic supplies contributed to the downward price trend.

- India’s domestic met coke prices inched up by INR 400-800/t this week. As per BigMint’s assessment, the 25-90 mm blast furnace (BF) grade stood at INR 32,800/t exw-Jajpur, while Gandhidham’s prices were at INR 28,800/t. Steelmakers in northern China, including Xingtai, Tangshan, Shijiazhuang, and Tianjin, cut met coke tags by RMB 50-55/t, starting 8 January, their sixth consecutive round of price reductions.

Ferro scrap

- India’s imported scrap market remained sluggish this week due to weak domestic demand, bid-offer mismatches, and a depreciating rupee, which raised import costs. Shredded offers from the UK stood at $383/t CFR Nhava Sheva, down 1% from $387/t last week, while HMS (80:20) offers ranged within $355-370/t CFR.

- Buyers favoured domestic procurement over imports, citing competitive local prices and concerns over safeguard duties on finished steel imports. Minimal deal activity was reported, with a $10/t bid-offer gap and cautious sentiment keeping market movement limited.

- Approximately 3,800-4,500 t of scrap were booked, including 2,300-2,500 t of HMS (80:20) scrap from South Africa, South America, West Africa, and the UAE at $355-375/t. Additionally, 1,000-1,500 t of shredded scrap were booked from Australia at $380/t and HMS (90:10) from the UAE at $360-365/t.

Ferro alloys

- Silico manganese: India’s domestic silico manganese prices experienced a significant surge w-o-w, with tags having risen for three consecutive weeks. This uptrend is attributed to a constrained supply and a market heavily influenced by sellers’ offers, resulting in heightened demand from buyers eager to secure material. Prices of the 60-14 grade scaled up by INR 1,450/t ($17/t) w-o-w to INR 69,600-70,800/t ($807-821/t) exw in Raipur, Durgapur, and Visakhapatnam.

- Ferro manganese: Indian ferro manganese (HC 70%) prices increased by INR 1,000/t ($12/t) to INR 73,900/t ($857/t) exw in Raipur and by INR 600/t ($7/t) to INR 73,500/t ($853/t) exw in Durgapur. The price rise can be attributed to improved steel demand and limited supplies in the region.

- Ferro silicon: Indian ferro silicon (FeSi: 70%) prices remained unchanged w-o-w at INR 104,000/t ($1,207/t) exw-Guwahati on 10 January. BigMint’s assessment of Bhutan’s prices edged down by INR 100/t ($1/t) to INR 104,000/t ($1,207/t) exw. Prices were stable, as Bhutanese sellers kept their January offers unchanged m-o-m.

- Ferro chrome: Indian high-carbon ferro chrome (HC60%, Si: 4%) prices declined by INR 3,000/t ($35/t) to INR 99,100/t ($1,150/t) exw-Jajpur. Prices plunged to their lowest point since July 2023, mainly due to reduced bids at Vedanta-FACOR’s latest auction and diminished realisations in the export segment.

- The latest auction by Vedanta-FACOR on 6 January saw the larger lot of 10-150 mm material booked at INR 99,200/t ($1,155/t) exw. A significant drop of INR 4,400/t ($51/t) was observed as compared to the previous auction on 20 December 2024.

Semi-finished

- Indian semi-finished steel prices witnessed a downtrend this week, as per BigMint’s assessment. Domestic billet prices across the country dropped by INR 300-1,300/t, with the highest decline of INR 1,300/t recorded in the Ahmedabad region. Meanwhile, sponge iron prices also showed a downtrend, with prices decreasing by INR 250-750/t across key locations. A major decrease of INR 700-750/t was observed in the Mandi Gobindgarh, Bellary, and Hyderabad markets.

- Indian direct reduced iron (DRI) export offers also witnessed a drop, with CPT Raxaul ones decreasing by $15/t w-o-w to $337/t and CPT Benapole offers falling by $14/t w-o-w to $340/t.

Finished long steel

- IF rebar: India’s induction furnace (IF) route finished long steel prices edged lower w-o-w. Limited trading activities were witnessed in the market, which varied region-wise. Buying interest remained subdued, owing to a lack of clarity on the market trend. Sellers offered attractive discounts to liquidate material. However, buyers opted for need-based procurement only. Market participants indicated liquidity issues in some regions, which exerted further strain. Suppliers in some clusters also highlighted inventory pressure, as current stock levels are expected to last more than 8-10 days, which is generally the average.

On a weekly basis, rebar prices fluctuated in the range of INR 200-1,000/t across regions, as per BigMint’s assessment. - The trade reference price of Fe 500 grade rebars manufactured via the IF route for 10-25 mm size was assessed at INR 41,300-41,700/t exw-Raipur and INR 45,800-46,400/t exw-Jalna.

- The trade reference price of heavy structural steel for the base size 150-mm channel stood at INR 43,700-44,100/t exw-Raipur.

- The trade reference price of wire rods hovered at INR 42,600-43,100/t ex-Raipur.

- BF-rebar: Indian tier-1 mills increased rebar list prices by up to INR 1,000/t for early-January 2025 sales. Post revision, list prices hovered at around INR 51,500-52,500/t on a landed basis.

- Meanwhile, trade-level blast furnace (BF) rebar prices witnessed a drop w-o-w across major markets, owing to slow demand in the domestic market. In the current week, rebar prices (12-32 mm) in the trade segment dropped by INR 100/t w-o-w to INR 52,500/t exy-Mumbai, excluding 18% GST.

- In the project segment, prices stood at around INR 49,500-50,500/t FOR Mumbai.

Flat steel

- Tier-I steel mills announced a price increase of INR 1,000-1,500/t compared to end-December 2024 prices for hot-rolled coils (HRCs) and cold-rolled coils (CRCs), applicable for January 2025 sales. Post revision, HRCs (2.5-8 mm, IS2062, Grade E250, Br.) were listed at INR 48,500-50,000/t ex-Mumbai and CRCs (0.9 mm, IS513 CR1) at INR 53,000-56,000/t. These prices are exclusive of 18% GST.

- BigMint’s bi-weekly benchmark assessment for HRCs (IS2062, Grade E250, 2.5-8 mm) and CRCs (IS513, Grade O, 0.9 mm) remained unchanged w-o-w on 7 January 2025, at INR 46,600/t ($576/t) and INR 53,400/t ($664/t), respectively. The prices are quoted ex-Mumbai, exclusive of 18% GST, and applicable for cut-to-length (CTL) deliveries.

- Despite a marginal price increase earlier, market sentiment remained subdued due to limited demand and continued low-priced transactions. As the week progressed, with supply normalising, prices in the northern region began to show slight corrections.

- India’s HRC export offers to Europe and the Middle East remained stable w-o-w, while Chinese offers declined across key markets, including the Middle East and Vietnam, due to weakening demand and pricing pressures.

Leave a Reply