Base metals prices on the London Metal Exchange (LME) majorly dropped with the highest fall recorded in zinc. However, the price of lead remained marginally up by 0.05%. Meanwhile, stocks on the LME registered warehouses witnessed varied trends for the week ending on 2 February 2024. Notably, the stocks of lead surged over 13% w-o-w to 125,775 t from 110,675 t.

In LME, three-month aluminium futures decreased by 1.8% to $2,233/tonne (t), while nickel settled at $16,235/t (down by 3.3%). Copper prices were at $8,482/t, zinc dipped by 5.3% to $2,451/t and lead prices gained marginally by 0.05% to $2,145/t.

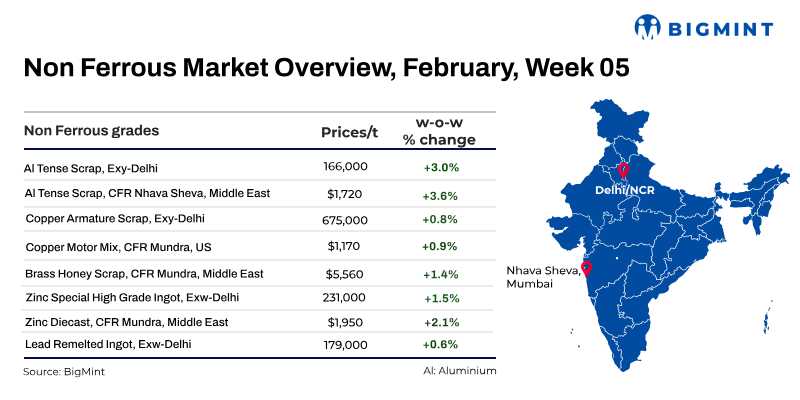

In the Indian non-ferrous metals sector, prices remained on the higher side diverging with the global trend. According to BigMint’s evaluation, non-ferrous metal prices in the imported as well as domestic segment witnessed gains w-o-w.

Market trade activities had gained momentum for the week, though concerns persisted about the increasing freight rates.

Aluminium

During the week, primary aluminium ingot (P1020) prices gained in the spot market, followed by price hikes by major primary players.

Aluminium ADC12 alloy ingot spot prices in India rose by INR 7,000/t w-o-w to INR 197,000/t, driven by surging local and imported tense scrap prices. India’s leading automobile manufacturer set February 2024 settlement prices at INR 199,500/t, up by INR 8,500/t m-o-m.

Raw material shortages, particularly tense scrap, caused elevated prices in northern India, while Chennai faced scarcity, impacting local manufacturers. Conversion spreads increased by INR 2,000-3,000/t, reflecting positive sentiments and improved capacity utilization.

The Indian imported aluminium scrap market witnessed a significant price surge, rising $60-70/t w-o-w. Factors such as increased futures, elevated freight rates due to Red Sea conflicts, limited material availability in the western region, and heightened demand contributed to this uptick.

In the domestic market, tense scrap scarcity kept prices high by 3% w-o-w to INR 166,000/t from INR 161,000/t in the previous week.

Copper

India’s domestic copper market prices gained up to 1% w-o-w amid a positive trend in finish market. Armature scrap prices stood at INR 675,000/t and secondary rods prices were at INR 715,000/t, both ex-Delhi. Supporting the market trend, a few deals for primary and secondary copper CCR were heard throughout the week.

In the imported segment, BigMint’s assessment for US-origin copper mix motor scrap stood at $1,170/t (up by 0.9%) and brass honey scrap (4%) from the Middle East gained 1.5% to $5,560/t, both CFR Mundra.

Zinc, lead

India’s domestic zinc and lead prices rose by up to 1.5% w-o-w, driven by a 2% increase in HZL’s ingot prices. BigMint’s assessment for zinc ingots were priced at INR 231,000/t (up 1.5%), and remelted lead ingots at INR 179,000/t (up 0.6%), exw-Delhi.

In the imported segment, zinc diecast (5%) from the Middle East was assessed at $1,950/t (up 2.1%), CFR Mundra.

Global updates

India’s manufacturing sector showed significant improvement in January, with the final Manufacturing PMI rising to 56.5, the highest in four months.

In December 2023, Japan’s industrial output increased by 1.8% from the previous month, driven by a surge in machinery production, according to data from the Ministry of Economy, Trade and Industries (METI).

Toyota Motor announced recently that it achieved a record-breaking sales figure of 11.2 million vehicles in 2023, securing its position as the world’s top-selling automaker for the fourth consecutive year.