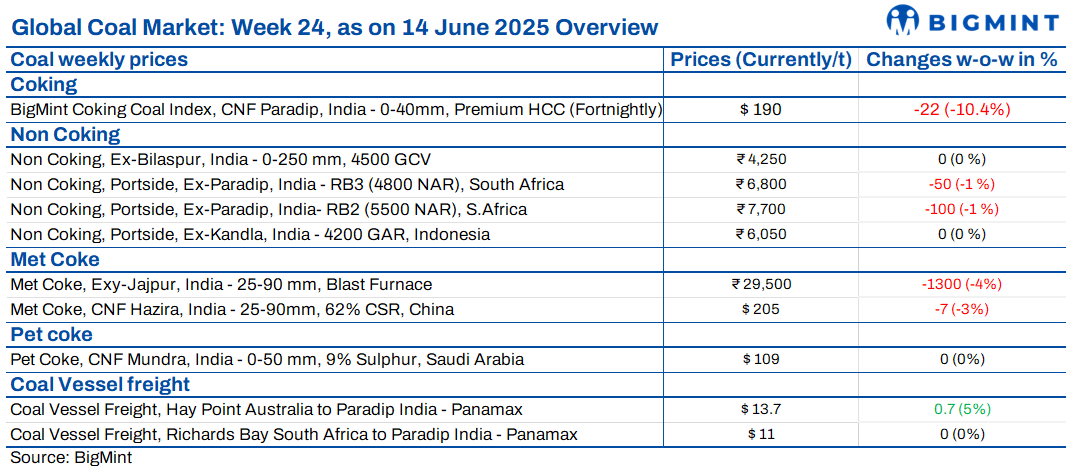

- BigMint coking coal index drops to three-month low

- South African prices drop on sustained weak demand

The Indian coal market continued to show sluggish activity this week as buyers remained cautious. Ample supply, weak industrial demand, and monsoon-related disruptions kept market sentiment subdued. Traders are refraining from aggressive bookings, with price corrections and limited restocking interest reflecting the overall bearish tone across both domestic and imported coal segments.

BigMint’s coking coal index drops to 3-month low

BigMint’s premium hard coking coal (PHCC) index was assessed at $189/tonne (t) CNF Paradip, India, on 14 June 2025, down by $23/t against the last index released on 31 May. The index has fallen to a three-month low, as per data maintained with BigMint.`Demand has been quite weak in the Indian market lately, with most buyers either staying away or showing preference for Canadian premium mid-vol coals.

Portside Indonesian prices steady amid weak demand

Indonesian thermal coal prices at Indian ports remained flat this week, pressured by weak industrial demand, better domestic coal availability, and higher vessel arrivals. BigMint’s 13 June 2025 assessment showed 5000 GAR prices at INR 7,700/t (Kandla) and INR 7,600/t (Vizag), while 4200 GAR stood at INR 6,050/t (Kandla) and INR 5,950/t (Vizag). The 3400 GAR grade was unchanged at INR 4,500/t (Navlakhi). Market activity remained limited despite rising port arrivals. Domestic coal stocks at power plants were at 60.96 mnt, enough for 21 days. Globally, Indonesian prices declined further amid oversupply and weak buying interest.

South African prices fall further on weak demand

South African thermal coal prices at Indian ports declined again this week due to weak demand, better domestic availability, and freight pressure from rising crude oil prices. RB2 (5500 NAR) fell by INR 100/t to INR 7,700/t at Gangavaram, while RB3 (4800 NAR) dropped by INR 50/t to INR 6,800/t. At Vizag, RB2 was assessed at INR 7,650/t and RB3 at INR 6,650/t. Around 55,000 t of RB2 was traded at INR 7,450–7,600/t at Dhamra and Gangavaram. Port stocks were steady w-o-w at 15.35 mnt. Sponge iron prices continued to drop amid sluggish billet and steel trends.

Domestic coal prices show mixed trends

India’s domestic coal prices came under pressure this week as demand remained weak and availability was sufficient. According to BigMint’s assessment, 5000 GCV grade prices dropped by INR 50/t to INR 4,700/t ex-Bilaspur, while 4500 GCV grades held firm at INR 4,250/t. Recent SECL auctions saw lower bids, indicating limited interest from buyers amid ongoing market sluggishness.

Met coke prices hit multi-year lows amid demand slump

Met coke prices in India dropped sharply this week, with the blast furnace grade down INR 1,300/t to INR 29,500/t ex-Jajpur — the lowest in five years. In western India’s Gandhidham, prices also fell by INR 1,100/t to INR 29,500/t, marking a five-month low. Sluggish steel demand, falling pig iron prices, and reduced procurement have weakened sentiment. Regulatory uncertainty regarding quota restrictions and anti-dumping duties further added to market caution. Meanwhile, China saw its third consecutive met coke price cut due to high inventories and poor demand. Prices are likely to stay weak, especially during the monsoon slowdown.

Imported pet coke prices stayed firm despite weak demand

Imported pet coke prices in India stayed largely unchanged last week. US-origin offers were reported at $106-108/t CFR, while Saudi-origin cargoes were offered at $109–111/t CFR. Although buying interest remained weak, firm offers were supported by limited supply and a rise in US freight rates. Looking ahead, the ongoing monsoon across many parts of India was expected to lower cement production, which could reduce pet coke demand from the cement industry – one of its key consumers.

IOC keeps pet coke prices unchanged for June

Indian Oil Corporation (IOC) held pet coke prices steady for June after reducing them twice in May by a total of INR 2,080/t. At Koyali, prices remained at INR 10,880/t for transportation via road and INR 10,680/t for via rake. Panipat stayed at INR 11,810/t. Eastern refineries like Paradip and Haldia also saw no change. Export prices to Nepal and Bhutan were rolled over too. Despite Nayara Energy cutting prices this month, IOC’s rollover reflects already competitive levels. Notably, IOC’s prices remain lower than Nayara’s, with Paradip showing the widest difference of INR 3,070/t.

Coal vessel freights down, except Australia route

Panamax vessel freight rates for coal shipments to India dropped w-o-w on most routes, except from Australia, due to reduced cargo flow. Weaker demand for coal and grains, along with monsoon-led slowdowns and ample port stocks, weighed on rates. In the Indian Ocean region, limited fresh bookings and high vessel availability pushed offers lower. Supramax’s competition remained stiff amid muted Asia activity. Baltic indices showed mixed trends: BDI rose to 1,633 points, BPI to 1,249 points, while BSI declined slightly to 933 points, reflecting inconsistent global chartering momentum despite some route-specific improvements.

Leave a Reply