- Domestic coal continued replacing imports

- Petcoke regained cement sector interest

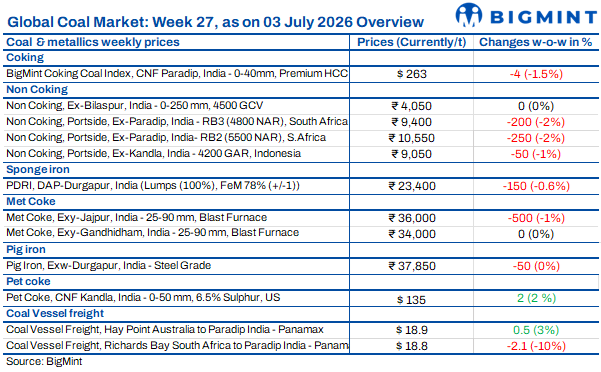

Coal markets remained subdued during the week ended 03 July’26 as weak steel and sponge iron demand, comfortable domestic coal availability and the monsoon continued to suppress buying interest. Imported thermal coal prices softened across most origins, while met coke and freight markets showed mixed trends. Buyers largely limited purchases to immediate requirements, preferring a wait-and-watch approach amid policy uncertainty and adequate inventories. Domestic coal continued to replace imports, whereas lower petcoke prices improved its competitiveness for cement producers without triggering aggressive procurement.

Indonesian coal prices softened further

Indian portside Indonesian thermal coal prices declined during the week ended 3 July’26 as weak buying and comfortable domestic coal availability reduced import demand. Prices of 5,000 GAR coal fell by around INR 50/t w-o-w to INR 10,950/t at Kandla and INR 10,850/t at Vizag. Meanwhile, 4,200 GAR eased to INR 9,050/t at Kandla and INR 8,950/t at Vizag, while 3,400 GAR slipped to INR 6,950/t at Navlakhi. Freight on the East Kalimantan-Navlakhi route declined by around $0.4/t w-o-w to $20.4/t. Thermal power plant coal stocks also fell 3% w-o-w to 43.4 mnt, although domestic coal supply remained comfortable.

HBA benchmarks extended gains

Indonesia’s HBA thermal coal benchmarks increased across all grades in the first half of July’26, supported by tightening spot availability, firm Asian utility demand and uncertainty over export policies. The 6,322 GAR benchmark rose 2% to $126.58/t, HBA-I (5,300 GAR) increased 3% to a record $90.94/t, HBA-II (4,100 GAR) climbed 4% to $62.59/t, and HBA-III (3,400 GAR) gained 2% to $41.91/t. Strong domestic supply obligations and limited export availability continued to support prices despite Indonesia approving over 600 mnt of coal production for 2026.

Portside coal prices extended decline

South African thermal coal prices at Indian ports declined as weak steel demand, sluggish sponge iron activity and ample domestic coal availability continued to weigh on buying. As per BigMint’s assessment, ex-Paradip RB2 (5,500 NAR) fell by INR 250/t w-o-w to INR 10,550/t, while RB3 (4,800 NAR) declined to INR 9,400/t. At Vizag, RB2 eased by INR 200/t to INR 10,400/t and RB3 dropped by INR 200/t to INR 9,300/t. Port inventories slipped 1.6% w-o-w to 14.83 mnt in Week 26. Spot buying remained limited despite lower prices, while PDRI Durgapur prices (DAP) fell by INR 100/t w-o-w to INR 23,500/t amid weak steel demand.

Domestic coal capped imports

Domestic coal continued to limit imported coal demand during the week as ample availability and competitive pricing encouraged requirement-based procurement. BigMint assessed 5,000 GCV coal stable at INR 5,500/t, while 4,500 GCV coal remained unchanged at INR 4,050/t w-o-w. Regular Coal India subsidiary auctions and comfortable supply kept the market well supplied, prompting some consumers to shift from imported to domestic coal amid high import costs and weak sponge iron and steel demand. Buying interest improved among large consumers, while SECL’s upcoming auctions were expected to attract steady participation despite lower monsoon-season offered quantities.

US NAPP coal stayed resilient

US Northern Appalachian (NAPP) coal retained steady demand from premium cement producers despite improving petcoke competitiveness. FOB Baltimore 6,900 NAR increased by $0.45/t w-o-w to $87.25/t, while FOB New Orleans 6,000 NAR rose by $0.45/t to $86.50/t. Meanwhile, Ex-Kandla, 6,900 NAR US-origin NAPP coal remained stable w-o-w at INR 13,450/t. Weekly retail lifting increased to 103,893 t in the week ended 29 June from 93,088 t a week earlier, while inventories at major western ports declined to 206,196 t from 406,155 t, reflecting healthy retail demand despite cautious buying by large cement producers.

Met coke market stayed cautious

India’s domestic met coke market remained cautious during the week ended 2 July’26 as buyers and sellers awaited clarity on the anti-dumping duty (ADD) on low-ash imports. BF-grade coke prices in eastern India fell by INR 500/t w-o-w to around INR 36,000/t ex-Jajpur due to weak spot demand, while western India remained stable at INR 34,000/t ex-Gandhidham. Foundry-grade coke also held steady at INR 36,400/t ex-Rajkot. Imported Indonesian BF-grade coke (65/63 CSR) eased by $1/t w-o-w to around $318/t CFR India, with FOB offers at $291-292/t. Chinese coke prices remained firm on tight coking coal supply, supporting global prices despite subdued Indian demand.

Petcoke regained cost advantage

Imported petcoke became more competitive after international prices corrected by over $20/t from May highs, improving fuel economics for Indian cement producers. As of 1 July’26, CFR India 6.5% sulphur increased marginally by $0.5/t w-o-w to $135/t, while CFR west coast India 8.5% sulphur rose by $1/t to $135/t. Despite the weekly increase, prices remained around $20-25/t below May levels. The lower prices were expected to reduce cement production costs by around INR 100/t from Q3 FY’27. However, comfortable domestic coal availability and the monsoon kept spot buying and discretionary imports subdued.

Refiners lowered petcoke prices

Indian refiners reduced domestic petcoke prices in July’26 following softer international market conditions. Nayara Energy cut its petcoke price by INR 1,680/t to INR 17,650/t, effective 1 July, after a similar reduction of INR 1,670/t in June. Meanwhile, CPCL reduced its petcoke price by INR 1,540/t to INR 17,760/t from INR 19,300/t. Despite the monthly corrections, Nayara’s price remained 31.4% higher y-o-y, while CPCL’s was up 35.2% y-o-y. The price decline reflected easing freight and supply concerns after improved US-Iran relations reduced pressure on the international petcoke market.

Coal freight market showed mixed trend

India’s dry bulk coal freight market recorded mixed trends during the week ended 3 July’26. Freight from Hay Point, Australia to Paradip increased by $0.5/t w-o-w to $18.9/t, supported by firm fixtures and tighter Panamax vessel availability. In contrast, the RBCT, South Africa-Paradip route declined by $2.1/t to $18.8/t amid weak cargo enquiries, while the East Kalimantan-Navlakhi Supramax route eased by $0.4/t to $20.4/t due to slower Indonesian coal movement. Meanwhile, the Baltic Dry Index (BDI) rose 2.3% w-o-w to 2,650, whereas bunker prices fell by $52/t to $661/t and Brent crude declined to $71.74/bbl.

Leave a Reply