India’s coal market remained under pressure amid sluggish demand, early monsoon disruptions, and high inventories. Portside and domestic prices softened across grades, while vessel freight rates and met coke prices also declined. Subdued industrial activity, cautious procurement, and global headwinds contributed to bearish sentiment across both thermal and metallurgical coal segments.

Indonesian coal prices drop further

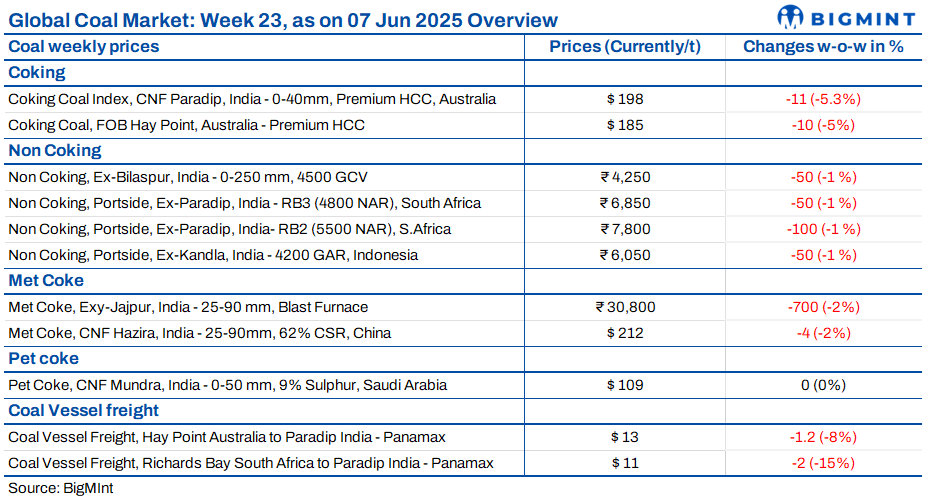

Portside Indonesian thermal coal prices in India fell again last week amid weak buying interest and sufficient domestic availability. The 5000 GAR grade slipped by INR 50/t to INR 7,700 at Kandla and INR 7,600 at Vizag, while 4200 GAR dropped to INR 6,050 and INR 5,950, respectively. Power plant coal stocks edged up to 61.17 mnt. Benchmark Indonesian coal prices also declined globally, with 4200 GAR falling by over $2/t. Demand stayed limited, with buyers restricting procurement to near-term needs due to market and economic uncertainty. Indonesia’s Ministry of Energy and Mineral Resources (ESDM) has revised its benchmark thermal coal prices (Harga Batubara Acuan or HBA) for the first half of June 2025, showing a sharp drop for high-calorific value coal and mixed trends across other grades.

South African coal prices drop as demand weakens

South African coal prices at Indian ports declined by INR 50–100/t last week amid weak buying and monsoon disruptions. RB2 was assessed at INR 7,800/t exw-Gangavaram and RB3 at INR 6,850/t, though trades remained scarce. Buyers placed unrealistic bids, especially for lower-NAR grades. Portside coal stocks rose 3% w-o-w to 15.40 mnt. May imports reached 4 mnt, up 12% m-o-m and 58% y-o-y. Export offers dropped, with RB2 offered at $71/t FOB. Sponge iron prices also weakened, with CDRI down INR 100/t at INR 24,400/t exw-Rourkela. Market outlook remains bearish unless demand revives or offers drop significantly.

India: Domestic coal prices ease on weak industrial demand

Domestic coal prices fell again this week due to subdued industrial offtake and steady supply. The 4500 and 5000 GCV grades dropped by INR 50/t to INR 4,250/t and INR 4,750/t exw-Bilaspur, respectively. In recent trades, 5000 GCV coal was booked for West Bengal at INR 6,900/t exw-Raipur. Additionally, an ECL G4 grade cargo of 6,000 t was sold at INR 6,650/t, reflecting selective restocking.

Met coke prices continue to head south

Metallurgical coke prices in India extended downtrend last week, with 25-90 mm BF grade falling by INR 700/t to INR 30,800/t ex-Jajpur and INR 200/t to INR 30,600/t ex-Gandhidham. Poor steel sector demand and cautious procurement led to reduced enquiries. Chinese coke markets also softened, with a third price cut likely. Outlook remains bearish amid policy uncertainty and tepid global cues.

Imported pet coke prices steady amid weak demand, tight supply

Imported pet coke prices in India remained unchanged week-on-week as subdued demand was offset by tighter supply due to delivery delays. US-origin offers held at $106–108/t CFR, while Saudi-origin material was quoted at $109–111/t CFR. No major deals were reported, market sources cited that higher freight rates from the US also contributed to sustaining current offer levels, despite limited spot activity. Overall, the pet coke market stayed in a wait-and-watch mode amid cautious procurement and limited inventory availability.

Mixed pet coke price trends in Jun’25

Refinery pet coke offers in India showed mixed movement in Jun’25. MRPL raised prices by INR 140/t m-o-m, quoting INR 10,570/t for road and INR 10,270/t for rake/barge supplies. Nayara slashed rates by INR 690/t to INR 13,170/t, down 5% m-o-m but 2.6% higher y-o-y. BPCL cut prices at both refineries — Bina rail supply dropped by INR 1,022/t to INR 14,120/t, and Kochi tags declined INR 951/t to INR 10,917/t. RIL continued withholding its price declaration, prioritising internal use, while Nayara remained the largest external supplier among single-unit refiners.

Coal freight rates fall amid vessel oversupply, weak demand

Coal freight rates to India declined this week as ample vessel availability in the Asia-Pacific clashed with subdued cargo demand. The Panamax and Supramax segments weakened due to cautious chartering and delayed fixtures, despite steady coal shipments from Australia and Indonesia. The Indian Ocean trade remained muted amid weak commodity prices. The Baltic Panamax Index fell by 127 points w-o-w to 1,119, while Supramax dropped by 32 points to 951.

Leave a Reply