- Imported fuel prices firm, domestic coal largely stable

- Freights strengthen but vessel availability caps upside

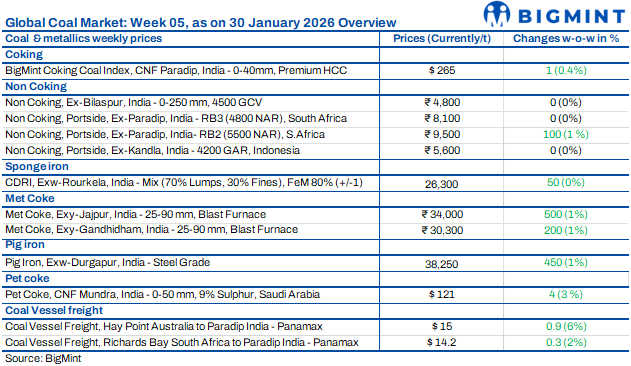

Coal market sentiment remained mixed, with firmness observed in imported fuels while domestic coal stayed stable. Tighter South African coal availability and rising global cost pressures supported imported prices, including metallurgical coke and petcoke. Indonesian grades saw muted trade amid adequate inventories and cautious procurement. Freight markets strengthened on higher bunker costs, though ample vessel supply limited sharp gains. Overall, buying remained requirement-based.

Indonesian coal prices stable

Indian portside prices of Indonesian thermal coal remained largely unchanged w-o-w in the week ended 30 January 2026 amid slower trades. As per BigMint, 5,000 GAR stood at INR 7,250/t at Kandla and INR 7,150/t at Vizag, while 4,200 GAR was steady at INR 5,600/t and INR 5,500/t, respectively. Lower-grade 3,400 GAR held at INR 4,500/t at Navlakhi. Supramax freight from East Kalimantan to Navlakhi rose $0.2/dmt to $11/dmt. Portside inventories increased 1% w-o-w to 12.95 mnt from 12.83 mnt. Indonesian benchmarks gained marginally, with 5,800 GAR up $0.49/t, 4,200 GAR up $0.39/t and 3,400 GAR up $0.33/t. Outlook had remained cautious.

South African coal prices rise

Portside South African thermal coal prices had increased in week 5 amid tightening stocks and selective deals. As per BigMint assessment, exw-Paradip 5,500 NAR rose by INR 100/t w-o-w to INR 9,500/t, while 4,800 NAR remained at INR 8,100/t. At Vizag, 5,500 NAR gained INR 150/t to INR 9,400/t and 4,800 NAR increased INR 50/t to INR 8,000/t. Indicative east coast levels were INR 9,400-9,500/t for 5,500 NAR and INR 8,100-8,200/t for 4,800 NAR. Offers stood at INR 9,700/t plus GST at Ennore and INR 9,450/t plus GST at Mangalore. Around 50,000 t were booked at $92/t CNF Paradip, while 75,000 t deals were concluded at $94-95/t CNF. Stocks at Dhamra, Gangavaram and Haldia were largely sold out, supporting firm near-term outlook.

Domestic coal prices stable

Domestic non-coking coal prices remained unchanged w-o-w, with 5,000 GCV assessed at INR 5,750/t and 4,500 GCV at INR 4,800/t. Market sentiment stayed stable, supported by steady supply through SECL auctions. On 27 January, SECL offered 1,716,050 t and allocated 915,200 t. Most bulk mid-CV grades had cleared close to floor prices, reflecting cautious and selective buying interest. Limited aggressive bidding was seen, as buyers largely focused on requirement-based procurement. The balanced allocation and adequate supply anchored the market, preventing any sharp movement in domestic prices during the week.

Met coke prices rise sharply

Indian BF and foundry grade metallurgical coke prices had risen sharply w-o-w on 28 January, driven by higher coking coal costs and tight foundry-grade supply. In east India, BF-grade (25-90 mm) increased by INR 500/t to INR 34,000/t ex-Jajpur, while in west India prices rose INR 200/t to INR 30,300/t ex-Gandhidham. Foundry-grade (+90 mm) jumped INR 900/t to INR 36,100/t ex-Rajkot amid limited availability. Australian PHCC climbed $14/t to $251/t FOB due to weather-led supply disruptions, while China remained stable. SAIL-Bhilai auctioned 4,940 t at INR 36,850/t ex-works, higher by INR 2,950/t m-o-m. Prices were expected to stay firm.

Imported petcoke prices rise

Imported petcoke prices in India had increased by $4-5 w-o-w, driven by firmer offers from the US and Saudi Arabia. As per BigMint assessment, US- and Saudi-origin material was assessed at $121/mt on the west coast and $124/mt on the east coast. Venezuelan petcoke prices had also strengthened, with CFR WCI levels at $117-118/mt compared with $116-117/mt in the previous week, marking a $1/mt rise. The upward movement had reflected steady buying interest and tighter seller offers in the global market.

Coal freights edge up

Dry bulk coal freight rates to India had risen in the week ended 30 January, supported by higher bunker prices and a stronger Baltic Dry Index (BDI). Geopolitical tensions, as the US deployed naval forces near Iran, had lifted oil and bunker costs, prompting owners to seek higher rates, while charterers had remained cautious. The BDI had jumped 241 points w-o-w to 2,002 on 29 January. Panamax increased 43 points to 1,062 and Supramax rose 56 points to 1,716. Route-wise, Australia-Paradip Panamax gained $0.9/dmt to $15.0/dmt. Richards Bay-Paradip rose $0.3/dmt to $14.2/dmt, while Indonesia-Navlakhi Supramax increased $0.2/dmt to $11/dmt. However, ample Indian Ocean tonnage capped sharper gains.

Leave a Reply