- Met coke market remains steady yet cautious

- Coal freights on key routes firm despite thin trades

Coal market sentiment in India remained largely subdued this week. Portside activity was slow, with traders hesitant due to weak industrial buying and cautious steel sector demand. Domestic coal held steady, while South African and Indonesian markets showed little movement, reflecting limited appetite for fresh bookings. Higher freights added pressure, but adequate stock levels at ports and plants kept supply balanced, leaving the overall market stable yet directionless.

Indonesian coal prices steady as freights climb

Portside Indonesian thermal coal prices in India remained steady w-o-w, with 5000 GAR at INR 7,150/t (Kandla) and INR 7,050/t (Vizag), and 4200 GAR unchanged at INR 5,700/t and INR 5,600/t, respectively. The 3400 GAR grade held at INR 4,450/t at Navlakhi. Power plant stocks declined to 50.57 mnt, though system comfort stayed at 17 days. Meanwhile, supramax freights East Kalimantan–Navlakhi rose to $16.95/dmt. International Indonesian coal eased.

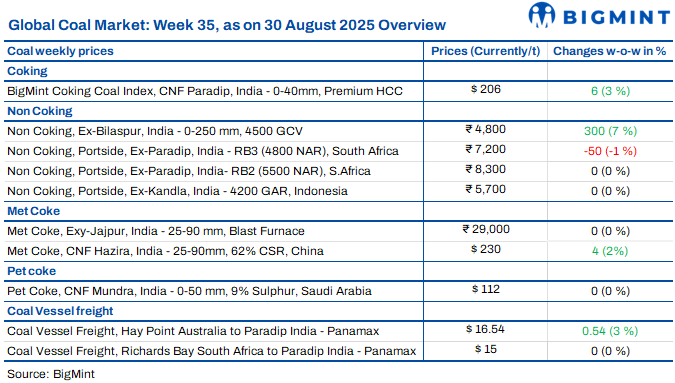

South African coal trade muted as demand stays weak

South African RB2 and RB3 coal prices held steady at Gangavaram this week, though some eastern ports saw offers ease by INR 100-200/t on weak buying. Two RB2 deals were heard – 12,000 t at INR 8,000/t ex-Paradip and 7,000 t at INR 8,325/t ex-Krishnapatnam – but overall market activity stayed low amid uncertain offers and thin trader stocks. Portside inventories dipped slightly to 13.78 mnt, while sponge iron prices weakened further. Export offers stayed mixed, with RB2 stable at $74/t FOB and RB3 edging down $1/t to $61/t.

Domestic coal prices firm w-o-w on tighter supply

Domestic coal prices in India rose this week, supported by lower stock availability. BigMint assessed 5,000 GCV at INR 5,700/t ex-Bilaspur, up INR 450 w-o-w, while 4,500 GCV increased INR 300 to INR 4,800/t. Tight inventories pushed prices higher, while SECL auctions also drew stronger bids despite muted interest from sponge iron players.

BigMint’s coking coal index edges higher, trade muted

BigMint’s PHCC index rose by $6/t w-o-w to $206/t CNF Paradip on 29 Aug’25, even as trade remained thin. Australian offers eased by $5/t, with market chatter placing quotes at $215-218/t CFR India, while buyers view $200-205/t as workable. A miner reportedly sold 75,000 t GYC cargo at $189/t FOB Australia, though Indian participants pegged tradable levels closer to $185-186/t FOB. Met coke prices in India held steady amid tight domestic supply, while Chinese curbs kept regional sentiment mixed. With steel under pressure, coking coal tags may face resistance despite limited supply support.

Met coke prices steady on tight supply

Met coke prices in India stayed stable w-o-w, with BF-grade assessed at INR 29,000/t ex-Jajpur and INR 30,000/t ex-Gandhidham, while foundry-grade held at INR 35,600/t ex-Rajkot. Supplies remained limited, and imports stayed muted as buyers resisted high-cost cargoes above $300/t CFR. Indonesian offers near $235/t CFR drew stronger interest. Softer coking coal costs eased some pressure, though demand from the steel sector stayed weak. Market outlook remains steady in the short term, with caution over potential corrections if mills rely on inventories instead of new purchases.

Imported pet coke offers stay steady

Imported pet coke offers in India held stable w-o-w, with US-origin at $114-115.5/t CFR and Saudi-origin at $112-114/t. Offers above $115/t kept trades on hold as buyers stayed cautious. Market activity remained subdued, with participants preferring a wait-and-watch stance. Demand is expected to revive gradually after the monsoon, led by infrastructure and construction sector consumption.

Dry bulk coal freights firm w-o-w

Dry bulk coal freights to India stayed firm w-o-w across Australia, South Africa, and Indonesia routes, despite thin trading. Hay Point-Paradip Panamax freights rose to $16.54/dmt, while Richards Bay-Paradip held steady at $15/dmt. Supramax rates from East Kalimantan to Navlakhi climbed sharply to $16.95/dmt. However, muted demand, wide bid-offer spreads, and steady domestic coal supply curbed fresh bookings. With vessel supply comfortable and Asian demand easing, freights may remain rangebound in the near term.

Leave a Reply