- Pet coke prices raised again in Sep on tight supply

- Portside coal inventories declined as arrivals slow

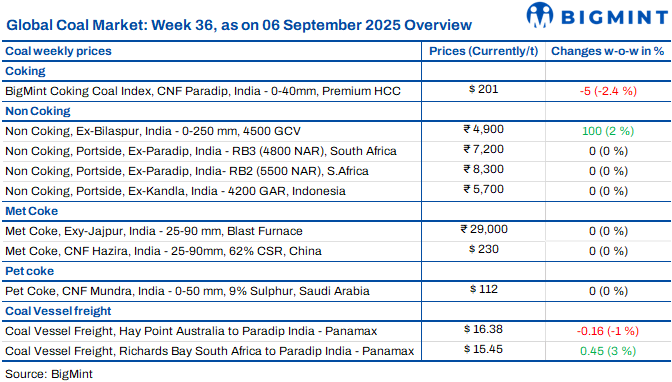

This week, India’s coal market showed a cautious undertone. Domestic coal prices edged higher for key grades, but the impact of GST revision to 18% and INR 400/t cess removal remained uneven across segments. South African and Indonesian portside markets stayed mostly steady, with sellers focusing on stock liquidation before the 22 September GST deadline. Imported pet coke offers held stable as buyers waited for clarity post-tax change. Dry bulk freight trends stayed mixed, with firm bunker costs supporting short-haul routes. Overall, market activity stayed subdued amid muted demand, with trade participants adopting a wait-and-watch approach.

Indonesian coal market steady; GST deadline keeps trades subdued

The Indian portside Indonesian coal market stayed cautious this week as sellers focused on liquidating stocks ahead of the 22 September GST shift. Prices eased INR 50/t for 5000 GAR at Kandla and Vizag, while 4200 GAR held firm and 3400 GAR softened at Navlakhi. Market activity was muted, with buyers waiting for clarity. Rupee weakness and higher freights added pressure, while international prices saw minor declines.

South African coal prices steady; GST changes keep buyers cautious

South African RB2 and RB3 prices at Gangavaram stayed flat w-o-w at INR 8,300/t and INR 7,200/t. Sellers rushed to liquidate limited port stocks before the 22 September GST deadline, while buyers held back, awaiting fresh offers. The GST hike and cess removal kept the market in wait-and-watch mode, as participants awaited clarity on its impact on steelmaking. Portside inventories fell 5.4% w-o-w to 13 mnt, while sponge iron prices improved on stronger demand.

Domestic coal prices stable; GST impact remains grade-specific

Domestic coal prices in India held steady this week, with 5,000 GCV assessed at INR 5,750/t ex-Bilaspur and 4,500 GCV at INR 4,900/t, both unchanged w-o-w. Market focus remained on GST changes. The effect stayed mixed — lower grades showed slight relief, while mid- to higher-grade coal turned relatively costlier, keeping overall market sentiment cautious.

Met coke market steady as demand stays cautious

The Indian met coke market held steady this week, with BF-grade prices at INR 29,000/t in Jajpur and INR 30,000/t in Gandhidham, while foundry-grade stood at INR 35,600/t in Rajkot. Offers remained firm as coking coal costs provided little relief, but buyers showed resistance amid weak steel demand. Pig iron auctions saw some improvement, yet overall demand stayed muted. Chinese coke sentiment softened on weak steel outlook. In the near term, India’s met coke market is expected to track global coking coal trends with a cautious tone.

Imported pet coke offers unchanged; buyers await tax impact

Imported pet coke offers in India stayed steady w-o-w, with US-origin assessed at $114-116/t CFR and Saudi-origin at $112-114/t. Market activity remained limited as participants held back from fresh bookings. Traders and buyers continued to adopt a wait-and-watch stance to gauge the effect of the GST increase alongside the removal of cess, with the real impact likely to emerge in the coming weeks.

Domestic refiners raise pet coke prices for Sep’25 on tighter supply

Nayara Energy, BPCL, and CPCL raised their pet coke prices for September, reflecting tighter supply conditions. Nayara hiked prices by INR 560/t m-o-m to INR 14,290/t, while BPCL increased rates at Bina by INR 541/t to INR 14,176/t (road offers INR 50/t lower) and at Kochi by INR 657/t to INR 12,080/t. CPCL also lifted prices by INR 560/t m-o-m to INR 14,000/t, with dispatches averaging 40-45 kt/month via road, mainly in Tamil Nadu and Andhra Pradesh. With RIL absent from the market since Apr’25, these refiners remain the key suppliers.

Dry bulk coal freights mixed, outlook remains cautious

Dry bulk coal freights showed mixed movements this week, with the Australia-India route easing while South Africa-India and Indonesia-India firmed. Limited cargo demand and abundant tonnage weighed on Pacific sentiment, though Indonesian freights rose on tighter vessel supply and firmer bunker costs. Market activity stayed muted, as high ocean freights restricted bookings and industrial demand remained subdued. In the near term, rates are expected to stay range-bound to soft amid weak Asian demand and oversupply of vessels.

Leave a Reply