- CIS billet under pressure from weaker Turkish buying

- Southeast Asia demand capped by slow finished steel sales

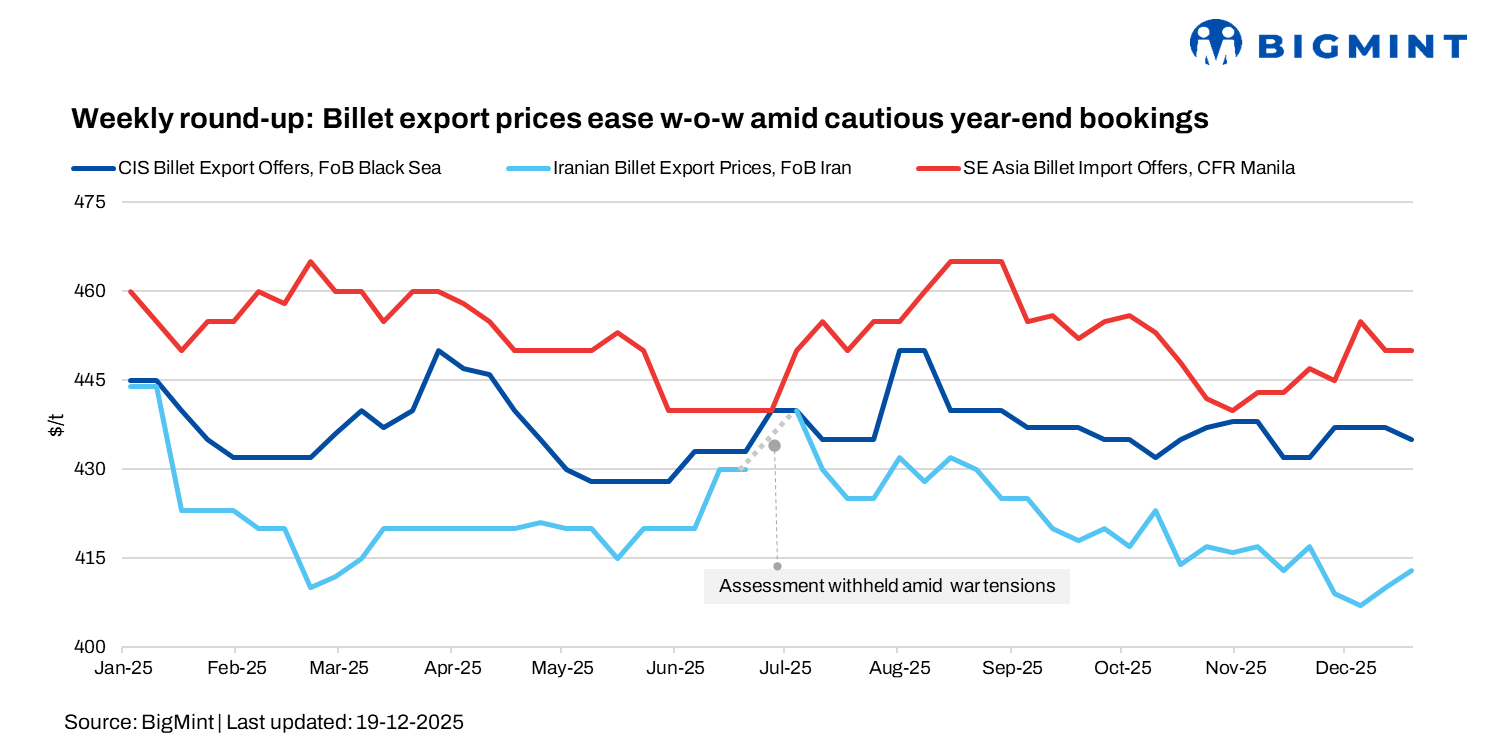

Global billet and scrap markets softened in the week ended 19 December, as buying interest remained subdued across Asia and the CIS-Black Sea region. Chinese billet export offers edged lower w-o-w, weighed down by weak domestic sentiment, while market participants described trade conditions as quiet, with wide bid-offer gaps restricting deal flow.

In contrast, deep-sea scrap import prices into Turkiye remained broadly stable despite limited transactions. Sentiment in Turkiye has turned cautious, with buyers largely covered for near-term requirements and pushing back against higher offers, amid persistently weak rebar demand.

CIS billet market

CIS billet prices moved lower this week as deteriorating market conditions in Turkiye forced suppliers to offer concessions to secure bookings. Kardemir concluded a fresh sales round at around $10/t lower, prompting Russian exporters to revise offers in tandem. At the same time, earlier support from the scrap market faded, limiting any upside for semi-finished products. A mild depreciation of the rouble, however, helped cushion margins and enabled some sales at revised levels.

By mid-week, the Russian square billet for February shipment slipped to $438-442/t FOB Black Sea, down from $445-450/t FOB last week. Market participants noted that firm bids could attract additional discounts of $1-2/t.

In the Turkish market, Russian billet was assessed at around $458-460/t CFR ($445-447/t FOB), slightly softer than last week’s $460-465/t CFR range. Several small January-shipment deals were concluded at $460/t CFR Black Sea ports, while a 15,000-t cargo reportedly traded near $458-460/t CFR Turkiye. Depending on the discharge port, workable FOB levels were seen closer to $435/t.

While some Turkish mills booked billet from Kardemir, finding it attractive versus scrap at current levels, most producers remain cautious amid a weak rebar market and are adopting a wait-and-watch approach.

Asian export billet market

Asian export billet prices were largely stable to slightly lower w-o-w, though trading activity remained muted as weak demand from the finished steel sector continued to cap buying interest across Southeast Asia. Market participants broadly described conditions as quiet, with wide bid-offer gaps limiting deal flow.

Chinese mills held 3sp billet offers at around $432-435/t FOB for February shipment, slightly down from mid-last week. Buyer interest, however, stayed below $430/t FOB. Recent signals around China’s export licensing framework for next year have not materially impacted the overseas billet market so far, as controls are largely aimed at non-VAT products, according to exporters.

In Indonesia, Dexin Steel lifted base-grade billet offers by $3/t w-o-w to $440/t FOB for April shipment. March cargoes were reportedly discussed at $430-435/t FOB, though deals were unconfirmed. Domestic offers rose to $458-460/t CFR, but demand remained absent amid oversupply in the longs market.

Elsewhere in Southeast Asia, open-origin 5sp billet was offered at $455-460/t CFR, while buyers capped bids below $450/t CFR. Thailand and Taiwan continued to see sizeable bid-offer mismatches, reinforcing the broadly cautious regional sentiment.

UAE steel market

The UAE rebar market has seen intermittent rainfall over the past week, mainly in northern and eastern regions, though the impact remains localised. Market participants said construction activity, logistics, and deliveries continue largely uninterrupted.

Prices remain stable as the market waits for the leading mill’s January 2026 announcement, with a rollover widely expected. Emirates Steel’s December rebar offer stands unchanged at AED 2,648/t ($721/t) exw, while non-benchmark trades are reported at AED 2,360–2,370/t ($642–645/t) delivered. Current market requirements are estimated at over 0.5 mnt.

Iranian billet export market

Iran’s semi-finished steel export market remains under pressure from regulatory changes and sharp currency volatility, keeping trade cautious despite firmer producer pricing. Mills are offering billet at $412-415/t FOB, up from $410-412/t last week, while traders remain closer to $410-412/t FOB, with some bids as low as $392-395/t FOB.

The widening gap between official and unofficial exchange rates has reduced export profitability, discouraging restocking. With the domestic market currently more attractive than exports, activity remains limited, even as producers launch new tenders for February shipments. Overall sentiment is cautious, with participants awaiting regulatory clarity and currency stability.

Leave a Reply