- Asian billet slips amid subdued exports during Chinese holidays

- Iranian exporters staying out of market due to sanctions

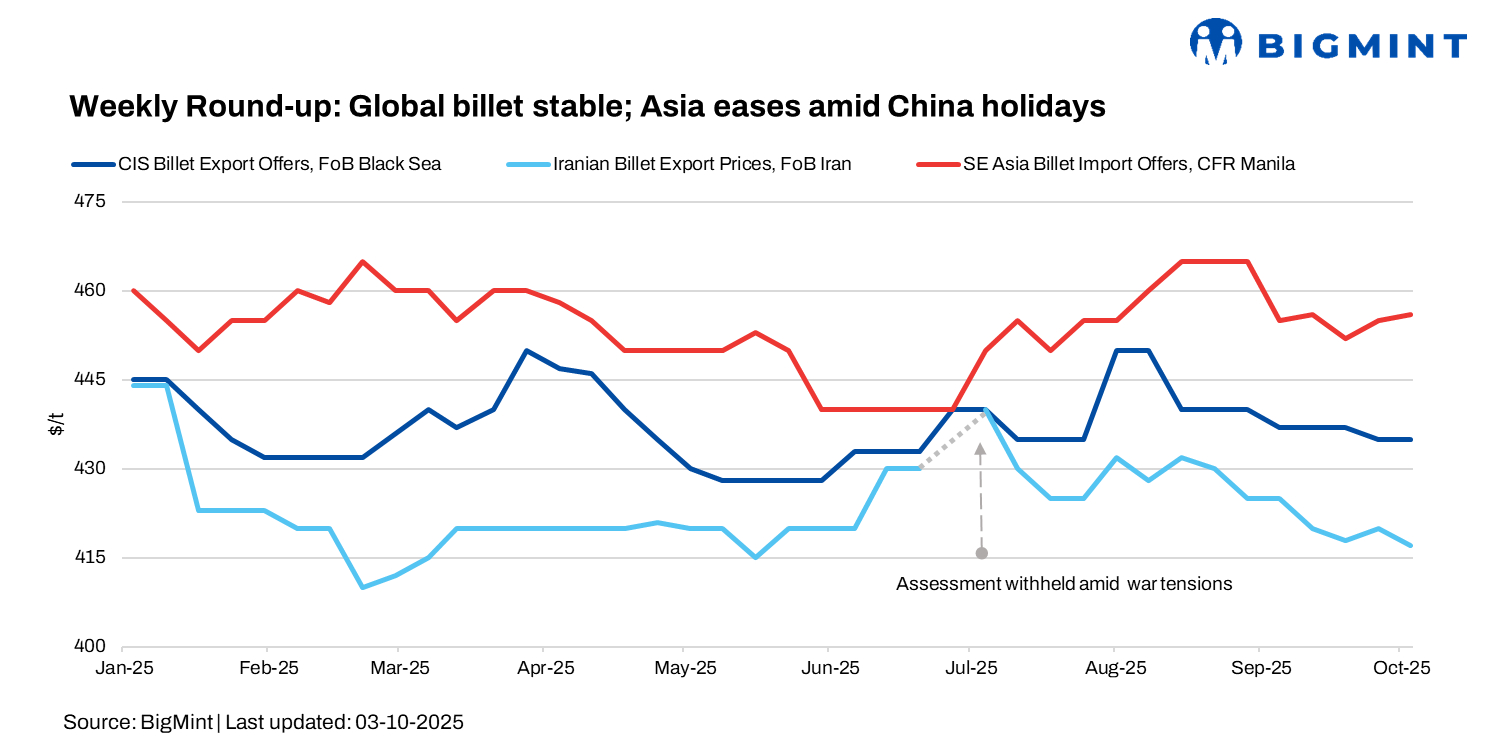

In week 40 of 2025, global billet prices softened across regions, while Turkiye and Russia witnessed stable prices. Asian export billet prices on the other side eased as buying interest remained weak amid China’s October holidays.

In Turkiye, deep-sea scrap prices edged up despite mills’ attempts to push them lower amid sluggish steel demand. Suppliers held firm, supported by reduced inbound flows, high freight costs, and expensive European scrap collection. While most October cargoes were already booked, limited late-October demand, tighter supply, and rising freight helped sustain offers, balancing the market despite muted downstream activity.

Asian billet export prices slip

Asian export billet prices fell over the week due to sluggish buying interest ahead of China’s October holidays. Chinese mills offered 3sp billet at $435-440/t FOB, down from $440-445/t FOB last week, reflecting weaker domestic and export demand.

In the Philippines, Chinese 5sp billet workable levels dropped to $452-455/t CFR w-o-w, and Thai buyers remained inactive after recent purchases at $450-452/t CFR. Overall, regional market sentiment remained subdued.

Indonesia’s major steel mill reduced base grade billet offers by $10/t to $435/t FOB, while focusing on slab production at $455/t FOB. Domestic 3sp material in Indonesia was available at $450-452/t CFR but saw limited buying.

China domestic prices: Billet prices declined by RMB 40/t ($6/t) w-o-w to RMB 2,950/t ($414/t) in Tangshan, while SHFE Jan’26 rebar fell RMB 42/t ($6/t) to RMB 3,072/t ($431/t). Ahead of the Golden Week holidays, market sentiment turned cautious as weak post-restocking demand and subdued exports pushed steel to three-week lows. Falling raw material costs and speculation over tariffs on EU imports further weighed on prices. Mills and traders largely paused fresh bookings, awaiting clearer demand signals after the holidays.

Iran’s steel exports face uncertainty amid sanctions

Iran is under renewed international pressure as the UN re-imposed sanctions under six Security Council resolutions, citing its “significant non-performance” on nuclear commitments. The EU has also reinstated measures, including travel bans, asset freezes, and trade restrictions on crude oil, natural gas, petrochemicals, gold, precious metals, diamonds, naval equipment, and key energy machinery. European allies emphasized that these sanctions “are not the end of diplomacy” and urged Iran to avoid escalatory actions.

This has heightened uncertainty in Iran’s steel sector, particularly semis exports. Many sellers are staying out of the market, with official offers and tenders largely absent. Iranian billets can still be booked at $415-420/t FOB, though some traders are offering $370-380/t FOB, down from $380-390/t last week. The sanctions have also affected the local currency.

While immediate impacts are mixed, industry players expect greater challenges in the coming months. Stricter shipment inspections have pushed bulk freight to northern China higher, with further increases likely after China’s public holidays.

Russia: FOB Black Sea billet prices have held steady over the past couple of weeks. Construction activity continues to slow, and housing completions are still declining in the country. Despite a slight uptick in demand, no meaningful recovery in completions is expected before year-end. Russian authorities have no plans to bail out developers facing bankruptcy.

Leave a Reply