- Iran’s absence in export market adds uncertainty to regional flows

- Asian billet export prices soften on weakening rebar futures

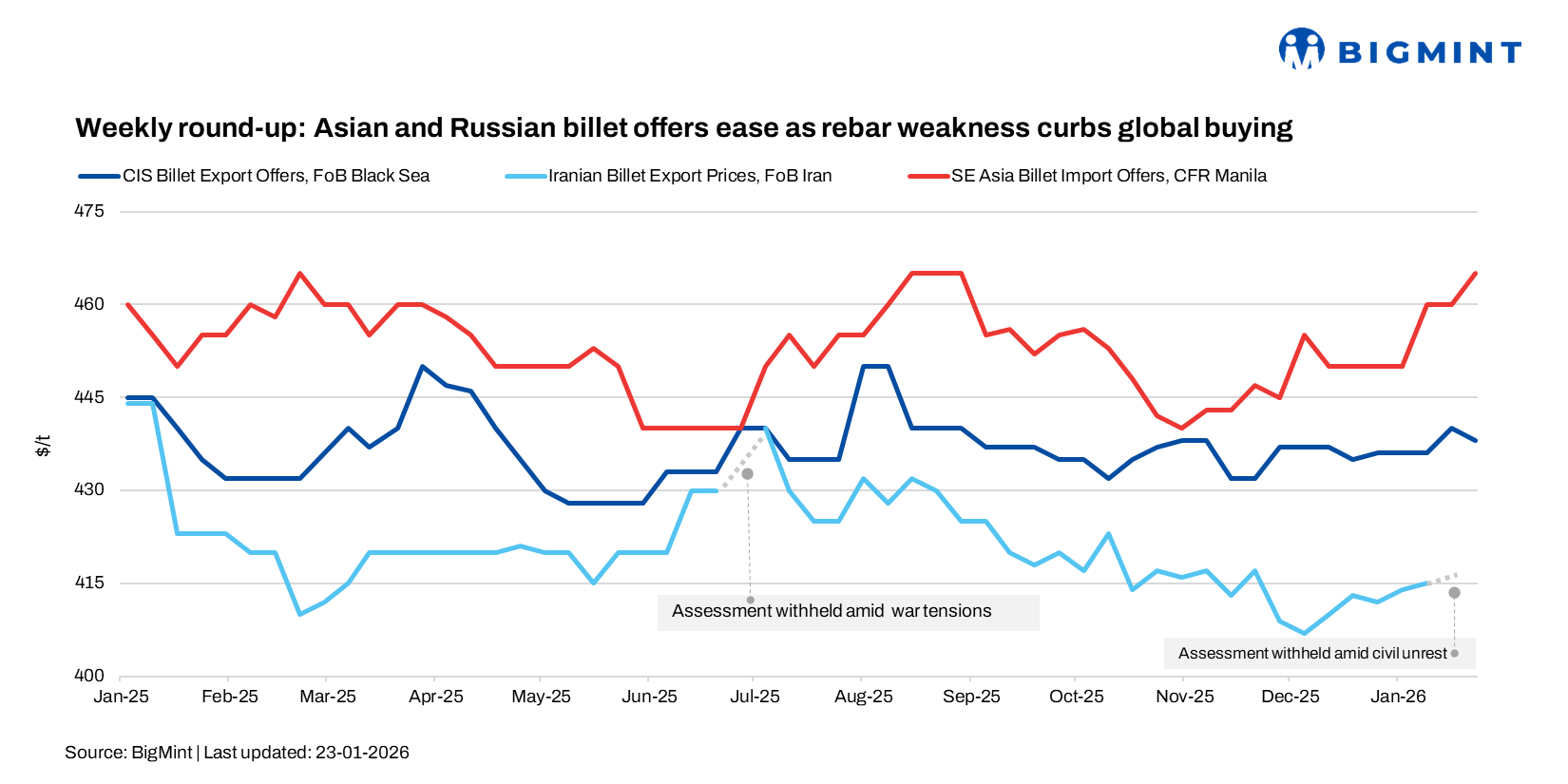

Global billet prices showed a mixed trend in the week ended 23 January 2026, with Chinese and Russian export offers softening, while the absence of Iranian export activity was noticeable. In contrast, the Middle Eastern markets remained firm, supported by elevated raw material costs. This encouraged some sellers to test higher price levels, although buyers stayed cautious and selective amid lingering demand uncertainty.

Meanwhile, deep-sea scrap prices in Turkiye stabilised after the recent sharp rise underpinned by tight seasonal supply, strong US domestic demand, limited export availability, high European collection costs, and a firmer euro. Trading activity was limited, though a few deals were concluded toward the weekend.

Around six-seven deep-sea scrap deals were reported at $369-381/t CFR. US-origin HMS 80:20 was mostly heard at $375-379/t CFR, while EU-origin material traded slightly lower at $369-373/t CFR. Sellers targeted $380/t CFR, but mills resisted higher levels.

Asian billet market

Asian billet export prices softened after last week’s sharp rise, largely tracking weaker rebar futures rather than demand. Chinese mills lowered 3SP billet offers to around $445/t FOB, down from $450-455/t FOB, with some offers heard at $438-440/t FOB China. No fresh sales to the Philippines were reported. Chinese billet offers eased to $465-470/t CFR Turkiye, with no deals concluded.

In the domestic market, Chinese billet prices fell RMB 30/t w-o-w to RMB 2,940/t ($422/t) on 23 January, pressured by weak downstream demand, winter disruptions, and high pre-holiday inventories. SHFE rebar futures declined RMB 49/t w-o-w to RMB 3,092/t ($444/t), keeping sentiment cautious ahead of the Lunar New Year despite limited late-week stabilisation.

CIS & Black Sea market

CIS: Both domestic and overseas suppliers remained active with billet offers in Turkiye, but buying interest stayed extremely weak due to the absence of rebar demand. Market participants said poor semis demand is being driven less by pricing and more by weak purchasing power, compounded by winter conditions and seasonal slowdown.

Domestic billet producers continued to offer material at $500-510/t exw, unchanged for two weeks, though sales remained minimal. “Billet needs to be capped near $505/t exw, given current rebar levels. There are virtually no rebar sales, and liquidity is tight,” a trader said. Several mills are planning maintenance shutdowns during this low-demand period.

In the import market, Malaysian billet for the March shipment was offered at $505-510/t CFR, while Indonesian material was heard around $495/t CFR. CIS-origin billet was not actively offered, though indicative levels were estimated at $460-465/t CFR.

Black Sea: Overall sentiment remained weak, with mills and traders largely sidelined, although activity in the Black Sea basin picked up as suppliers returned after the winter holidays, providing alternative sourcing options.

Middle East market

UAE: Emirates Steel Arkan (ESA) kept rebar prices unchanged for February sales at AED 2,648/t ($721/t) exw Abu Dhabi, excluding 5% VAT. Prices have now remained stable for four consecutive months. Market sentiment is cautiously steady, supported by consistent construction demand, with mills preferring selective price adjustments over broad hikes.

Saudi Arabia: Ferrous scrap prices rose again, tightening steelmaker margins as rebar prices stayed flat. A major Eastern Province mill raised its HMS 80:20 buy price by SAR 40-45/t ($11-12/t) to SAR 1,410-1,420/t ($376-378/t), following an earlier hike this month. The increase comes despite domestic rebar prices holding at SAR 2,020-2,220/t ($539-592/t) delivered. Mills cited firmer international scrap benchmarks and pre-Ramadan stocking, though uneven buying and greater DRI usage underline ongoing margin pressure.

Iraq: Rebar demand remained firm in late January, supported by tight domestic supply and reduced Iranian inflows, despite a weakening dinar. EAF-based mills adjusted prices to $620-665/t exw, while billet-based mills held offers near IQD 875,000/t exw (around $589/t). Limited Iranian rebar was available at $570/t ex-warehouse, while Turkish material remained uncompetitive near $800/t ex-warehouse.

Iran: Iranian billet export prices were heard at $410-415/t FOB, unchanged w-o-w, with minimal trade amid geopolitical tensions, intermittent internet access, currency weakness, and broader economic disruption. Despite these challenges, exporters expect no immediate price impact, with the market largely in wait-and-watch mode as conditions stabilise.

Leave a Reply