- Russian/CIS billet offers soften; Asian markets stay muted

- Iran and China billet prices edge higher despite weak demand

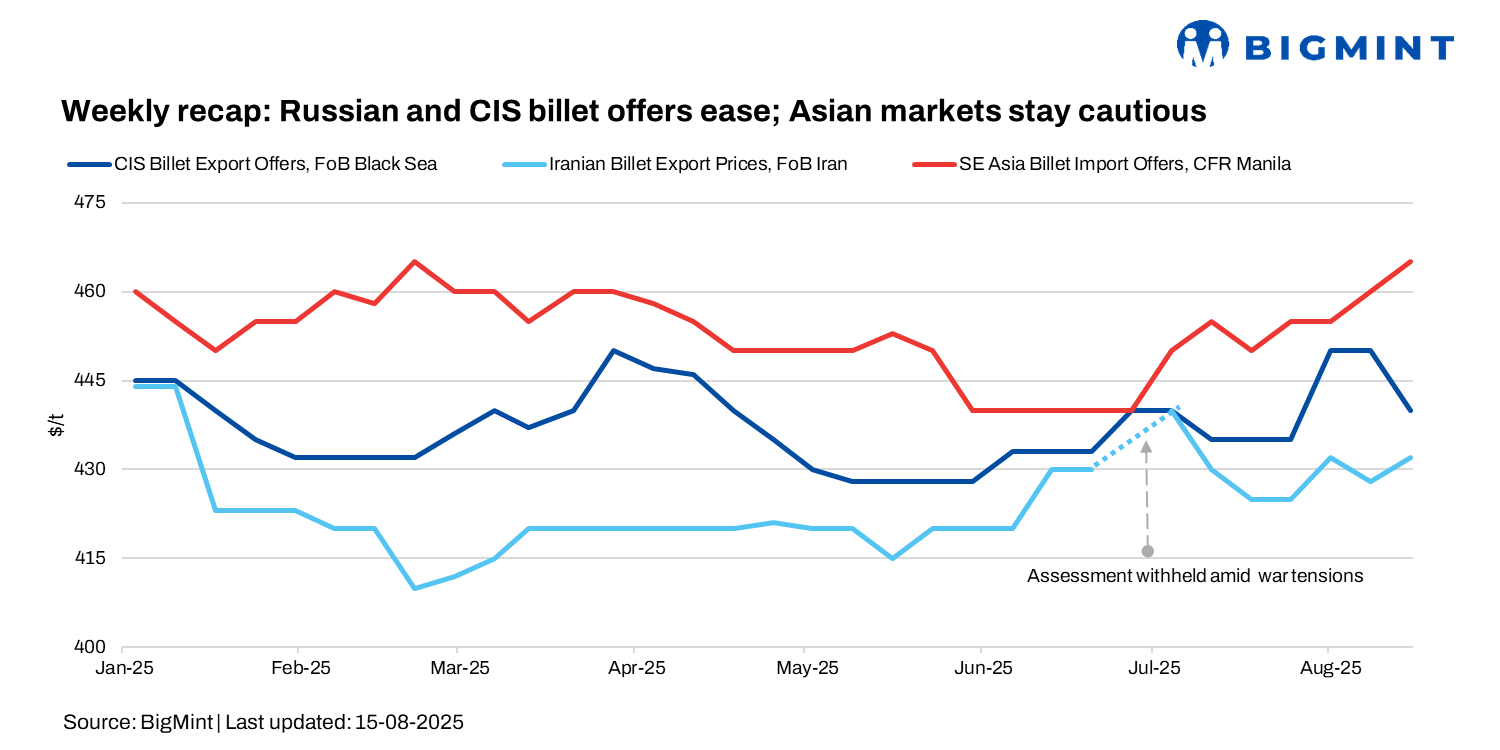

Billet prices showed a mixed trend in the 33rd week of 2025. Russian and CIS suppliers trimmed offers on weak demand, while Asian markets saw slight gains on tighter supply and steady regional buying.

Russian billet slipped to $445-450/t FOB Black Sea for late September shipment, pressured by higher freight and sluggish demand, though CIS mills avoided aggressive sales, banking on currency support. In Turkiye, Russian billet was quoted at $460-470/t CFR ($440-450/t FOB), with bids capped at $455-460/t CFR. Freight costs could keep prices closer to $465-470/t CFR.

BigMint assessed Turkiye’s imported scrap market as largely stable, with US/Baltic-origin HMS 80:20 at $345-350/t CFR and EU-origin near $340/t CFR. A few September-shipment deals were reported early in the week, but overall activity was muted as many participants remained on holiday.

Sentiment stayed weak, with sluggish finished steel sales and poor rebar demand limiting mills’ appetite for fresh cargoes. While sellers resisted deeper cuts, buyers remained cautious, expecting little movement until steel fundamentals improve.

Market highlights

Asian market remains sidelined

Market activity was muted with Japan’s Obon holiday curbing export flows, indirectly supporting US sellers. In Taiwan, traders raised offers to $470/t CFR, up from $460-465/t CFR last week, but buyers resisted.

Limited Russian supply kept sentiment subdued, with demand expected to pick up post-holiday.

Iran’s billet prices rise w-o-w

Billet prices rose 500 rial/kg w-o-w, reaching 326,000 rial/kg on 13 Aug from 325,500 rial/kg on 11 Aug. Rebar, however, held steady at 380,000 rial/kg after slipping 5,000 rial/kg earlier in the week.

On the supply side, production remained constrained due to power and water shortages, with a severe gas scarcity looming later this year. Utility costs have surged sharply, with water prices increasing 40-fold and electricity rates also higher, further squeezing mill operations. Added to this, currency volatility continues to weigh on market sentiment. Despite weak demand, these cost and supply-side pressures have kept domestic steel prices supported.

In the export market, billet offers were heard at $425/t FOB, while slab was quoted at $405–410/t FOB

BigMint assessed Russian billets at $440-445/t FOB Black Sea, down by $10/t w-o-w. CIS-origin offers held at $455-460/t CFR Turkiye.

China billet prices inch up by RMB 30/t ($4/t)

Tangshan billet opened at RMB 3,070/t ($427/t incl. VAT) in the early week, with SHFE Oct’25 rebar around RMB 3,213/t ($448/t). Market sentiment was cautious amid weak end-user demand.

Towards the last mid-week, Tangshan billet climbed RMB 30/t to RMB 3,100/t ($431/t incl. VAT), while SHFE rebar gained RMB 31/t to RMB 3,244/t ($452/t). Gains were supported by firmer raw materials, stable margins of around $70/t, and Baosteel’s expectations for a September hike.

Leave a Reply