- CIS billets rise as freight hikes lift Turkiye offers

- SE Asian billet bids slide on weak Chinese sentiment

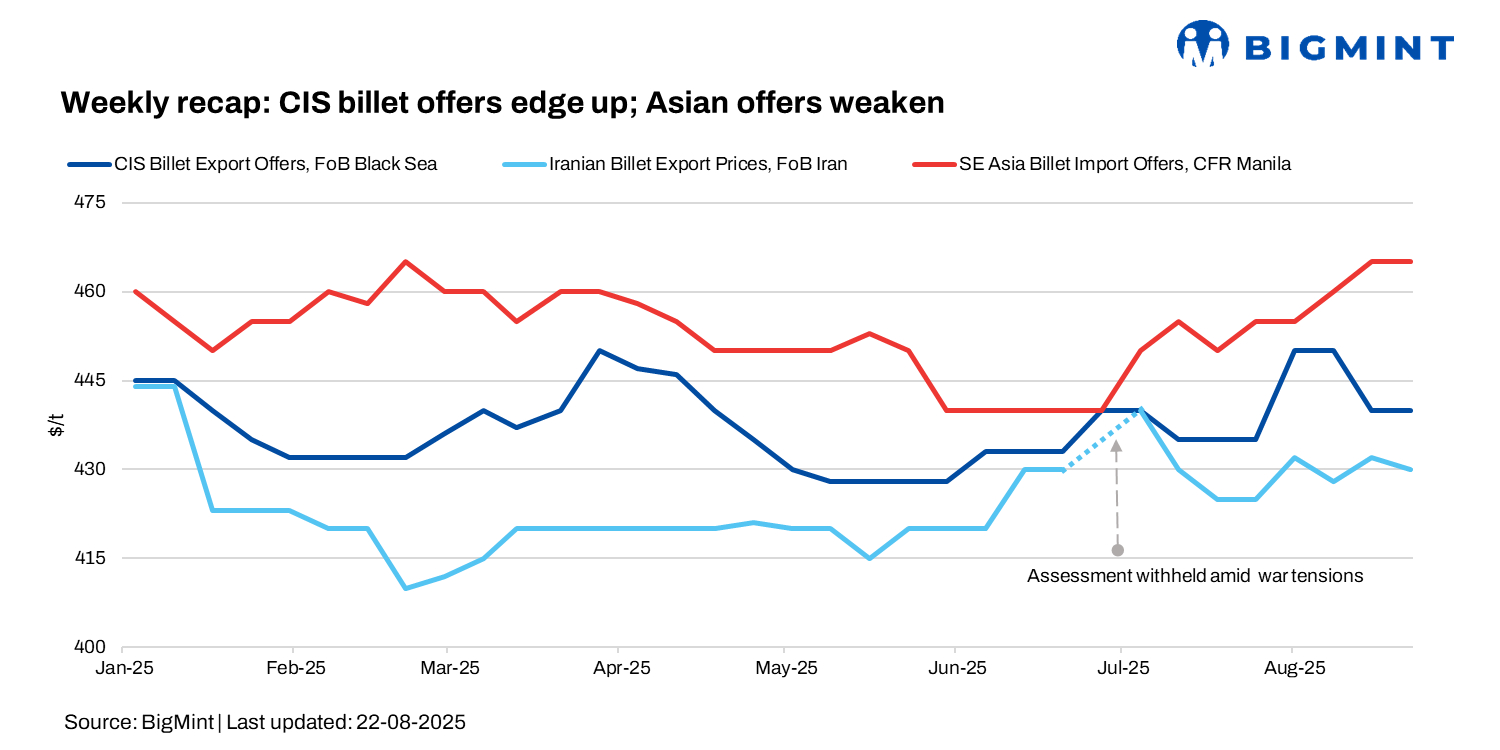

Global billet prices moved unevenly in the 34th week of 2025. CIS export activity remained quiet, though FOB Black Sea prices inched up to $445-450/t for October shipments from $440-445/t last week.

In Turkiye, rare CIS offers emerged at $460-470/t CFR ($435-440/t FOB), higher w-o-w as freight to Turkish ports rose to $28-30/t from $20/t, but buyers remained sidelined.

Asian billet prices slipped as weak Chinese sentiment prompted Southeast Asian buyers to pause.

Meanwhile, Turkiye’s deep-sea scrap market held steady. US/Baltic HMS 80:20 was assessed at $345-348/t CFR, and EU-origin scrap at $342-344/t CFR. Weak rebar demand and rising costs kept mills from making fresh bookings, with most waiting until September amid thin activity and tight supply.

Market highlights

Asian billet prices ease as buyers stay on the sidelines

Asian markets softened on weak demand. Chinese mills lowered October shipment billets to $440-445/t FOB from $450/t last week, while CIS imports from China ($475-480/t CFR) and Malaysia ($485-490/t CFR) attracted little interest amid high freight. Turkish domestic billet offers stayed stable at $510-515/t exw, but trades were limited.

Traders sought $430-435/t FOB, while mills held firmer; SE Asian bids hovered at $440-445/t CFR, and Indonesian importers targeted $450-455/t CFR. Exporters saw limited downside ahead of China’s production restrictions and the September-October peak season.

Indonesia’s major steelmaker kept November billets at $450/t FOB, focusing on local steel amid government projects.

In the Philippines, Chinese 5sp billets eased to the $460s CFR, while Vietnamese cargoes remained steady at $455-460/t CFR.

Iran billet holds firm, rebar softens

Iran’s steel market stayed cautious last week. Billets rose 500 rial/kg to 326,500 rial/kg on 18 Aug and then held steady as of 20 Aug, while rebar eased to 383,000 rial/kg by 20 Aug from 390,000 rial/kg on 13 Aug.

Political uncertainty, sanctions risk, and power/water shortages limited production. Domestic demand remained muted, with prices driven mainly by currency movements. Exports saw billet offers at $425/t FOB and slab at $405-410/t FOB.

China billet prices inch down by RMB 30/t ($4/t)

Tangshan billet prices fell RMB 30/t ($4/t) to RMB 3,030/t, while SHFE Oct’25 rebar futures dropped RMB 125/t ($17/t) to RMB 3,119/t, hitting a 3-month low before stabilizing. HRC/flat products stayed above RMB 3,400/t.

Rising inventories reflected weak domestic demand, though Northern China’s maintenance eased supply pressure. Exports were muted, but billet shipments may rise to offset soft rebar. Iron ore eased to a 2-week low, while coke prices attempted a 7th hike amid fragile demand. US tariffs and weak global trade further dampened sentiment. September demand recovery could provide support, though near-term pressure remains.

Leave a Reply