- Chinese policy boosts a stagnant billet market

- Turkish scrap prices edge up, buyers show caution

In the 28th week of 2025, the global billet market showed mixed sentiment, shaped by regional supply and demand dynamics. While some optimism emerged in Asia on expectations of policy support, cautious buying and weak downstream demand kept overall trade limited. Sellers held firm, and buyers stayed watchful amid uncertainty. The market remains stable, with a gradual recovery in activity anticipated as clearer signals on demand and policies emerge.

Recent Chinese policy support for the property sector and urban redevelopment has lifted sentiment. Anticipation around an upcoming conference on urban issues briefly boosted property prices, triggering a rally in iron ore swaps on hopes of stronger construction-led steel demand.

According to BigMint, Turkiye’s bulk deep-sea ferrous scrap prices edged up by $2/tonne (t) w-o-w to around $347/t CFR, although mills paused fresh purchases after securing significant volumes last week. Ongoing bearish sentiment in the rebar market kept buyers hesitant about paying above $345/t CFR for HMS 80:20.

Market highlights

The Asian billet market is steady and even exhibiting slight bullishness amid talks of China’s urban renewal plans and possible stimulus measures. Sellers are holding back offers, expecting prices to improve, while buyers remain cautious as demand stays moderate. Overall, the market is mildly optimistic but careful, with participants waiting for clearer signs of stronger demand and firm policies before making bigger moves. For now, the market is stable with a slight improvement in sentiment.

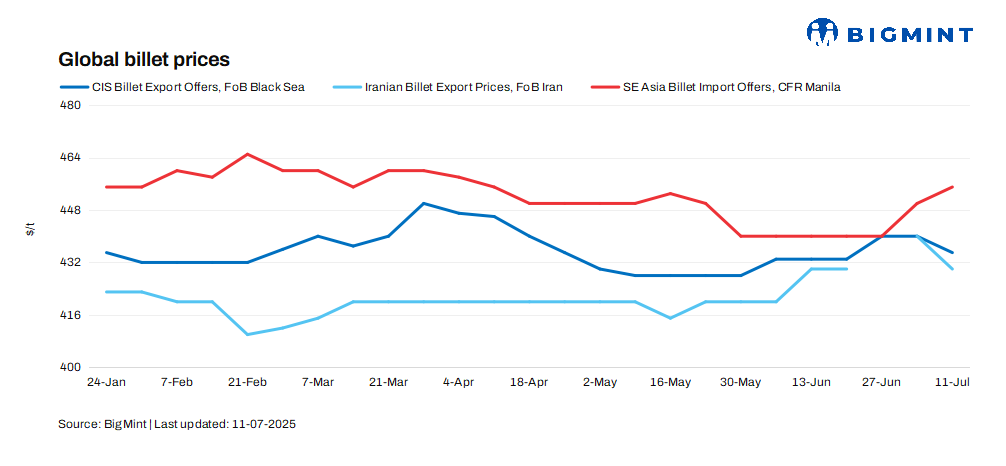

In the Philippines, offers for 150×150 mm 5sp billets rose by $5/t w-o-w to $455/t CFR Manila as of 11 July, as sellers withheld material amid rising prices. However, reports indicated that buyers’ bids had edged slightly lower, though market participants did not expect these lower bids to be workable in the current seller-driven market.

Iran’s billet market has resumed activity partially, with prices holding stable at $430/t w-o-w FOB Iran with Iranian long steel exporters proactively seeking new markets in response to ongoing electricity restrictions and changing demand in their traditional destinations. While no tenders have been announced yet, market players expect an open tender to be issued next week, however buyers are seen to be on edge with bargaining power.

BigMint’s Russian billet assessment, FOB Black Sea, inched down by $5 w-o-w to $435/t FOB for 125-150 mm square billet, with overall market activity remaining decent despite the slight dip. This was also driven by the current dip in the regional iron ore prices, adjusting the semi-finished segment prices. Meanwhile, the flats segment continues to perform well.

Chinese billet prices inched up by RMB 20/t ($3/t) w-o-w: Steel billet prices in Tangshan, China, surged by RMB 20/t ($3/t) w-o-w to RMB 2,960/t ($413/t), including 13% VAT, on 11 July 2025. Billet prices showed strength boosted by positive macroeconomic news, spike in raw material tags and a slight better demand in the finished segment. Meanwhile, SHFE rebar futures (October 2025 delivery) rose w-o-w by RMB 61/t ($9) to RMB 3,133/t ($437/t) on 11 July.

Leave a Reply