- India’s domestic prices stable amid slow demand

- Indonesia raise HBA prices, China demand weak

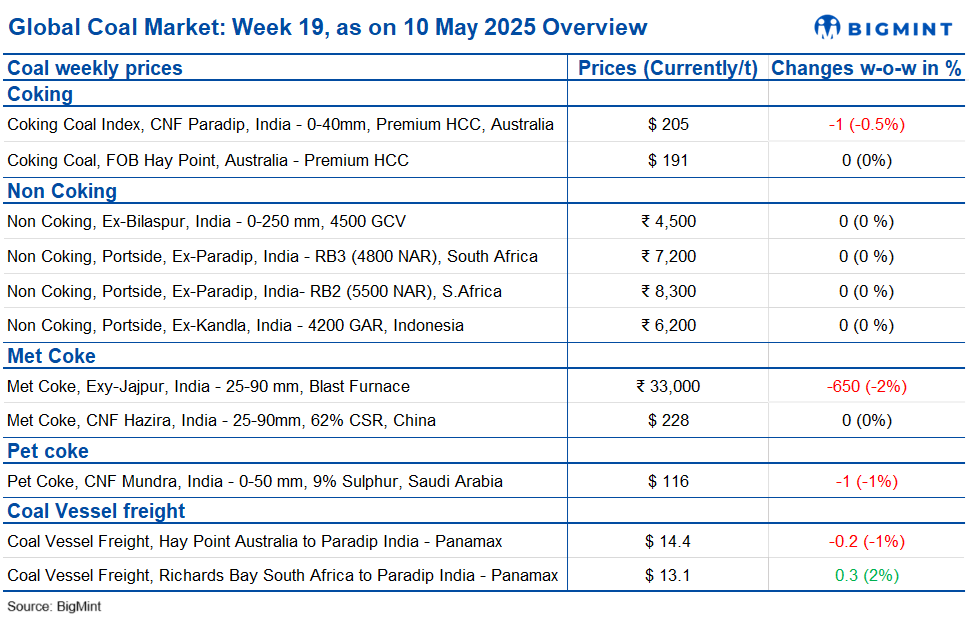

Sentiments in the Indian coal market remained weak, with limited buying interest and high stock levels across both domestic and imported materials. Market participants are holding off on fresh purchases due to sufficient inventories, leading to muted demand. The surplus availability from ongoing auctions by Coal India subsidiaries further dampened buying activity. Sluggish demand is mirrored in the softness in South African coal prices and stable domestic coal market. The overall outlook suggested lack of optimism, with prices remaining stable or experiencing minimal decline, reflecting cautious sentiment and limited market movement.

Indian portside coal market dull amid steady prices

The Indian portside market for Indonesian thermal coal stayed quiet this week, with limited buying and selling. Traders remained cautious due to global tensions and shifting supply patterns. Prices mostly stayed the same. At Kandla, 5000 GAR held at INR 7,800/tonne (t), while 4200 GAR stayed at INR 6,200/t, and INR 6,100/t at Vizag. The 3400 GAR dropped INR 200/t to INR 4,600/t at Navlakhi due to ample supply. Portside stocks rose by 7% to 14.22 million tonnes (mnt). Power plants’ coal stocks also improved. Global coal prices showed mixed movement, with lower-grades gaining slightly and higher ones slipping.

SA portside prices under pressure amid weak demand

South African coal prices continued to soften this week as demand remained sluggish and portside stocks remained high. RB2 prices dropped by INR 50/t to INR 8,300/t exw-Gangavaram, while RB3 held steady at INR 7,200/t. A deal for RB2 was done at INR 8,150/t at Ennore. Non-coking coal imports from South Africa decreased by 8% m-o-m to 3.24 mnt in April 2025. Sponge iron prices also fell, reflecting weak market sentiment. Export offers for RB2 and RB3 decreased further to $73.5/t and $61/t FOB, respectively. The outlook remains soft with limited spot trades and low demand.

Domestic coal prices stable amid low demand

Domestic coal prices remained steady this week, with 4500 GCV and 5000 GCV grades at INR 4,500/t and INR 4,950/t exw-Bilaspur respectively. Market sentiment was weak as buyers held adequate stocks and avoided new purchases. The surplus availability from ongoing Coal India auctions further dampened buying interest, resulting in subdued demand across the market.

Indonesia raises HBA prices, but China demand weak

Indonesia raised its thermal coal reference prices (HBA) for the first half of May, marking the biggest hike in mid-CV grade prices in two months. The 5,300 kcal/kg GAR HBA-I price rose by 3% to $80.8/t, while high-CV coal edged up 0.8% to $121.15/t. Lower grades also saw slight increases. The price rise reflected recent market recovery, but Indonesian cargoes were uncompetitive in China. As of 7 May, the price gap between Indonesian and Chinese 3,800 kcal/kg NAR coal narrowed to just RMB 15/t, limiting buying interest from Chinese traders despite improved pricing on the Indonesian side.

Met coke, pig iron prices drop further on weak steel demand

Domestic met coke prices fell again this week, with BF-grade coke at INR 33,000/t exw-Jajpur, down INR 650/t w-o-w. Gandhidham prices dropped INR 1,200/t to INR 31,000/t. Eastern India has seen a INR 1,100/t decline since 24 April. Pig iron prices in Durgapur also slipped further to INR 32,850/t, hit by weak finished steel demand. NMDC’s auctions are seeing poor response only 1,500 t out of 10,000 t were booked on 5 May. Meanwhile, Australian coking coal prices rose by $2/t to $192/t FOB. In China, coke prices held steady as mills slowed buying due to high inventories and sluggish downstream activity.

IOCL cuts pet coke prices by INR 1,000/t for May 2025

Indian Oil Corporation Ltd (IOCL) has reduced pet coke prices by INR 1,000/t m-o-m for May 2025. At Koyali refinery, the road price is INR 11,960/t and rake price INR 11,760/t. Panipat’s rate stood at INR 12,900/t. Prices at Paradip and Haldia were also cut for both road and rake deliveries. Export prices to Nepal and Bhutan saw a downward revision as well, with Paradip quoted at INR 12,490/t and Haldia at INR 12,360/t. The price drop reflected easing demand and better supply availability, offering cost relief to domestic and regional buyers.

US pet coke prices dip on weak demand, trade tension

US pet coke prices fell in both eastern and western India to $100-102/t CFR this week, amid ample supply and subdued demand from China. Ongoing trade tensions between the US and China, including high tariffs and counter-measures, have led to lower US pet coke exports. Meanwhile, offers for Saudi-origin material remained firm at $116-118/t CFR, supported by steady Chinese interest. The current price gap between US and Saudi cargoes is seen as unsustainable in the long term, as market forces may prompt a correction if demand shifts or trade dynamics ease.

Coal freight rates dip on most routes amid vessel oversupply

Coal freight rates for India declined w-o-w on key routes due to excess vessel availability and weak cargo volumes, especially in the Pacific basin. Freights from Australia to Paradip dropped $0.20/t to $14.4/t, while Indonesia-Paradip fell $0.6/t to $13.5/t. Only South Africa-India freights rose $0.3/t to $13.1/t, due to tighter vessel supply. Rising coal inventories at Indian ports (up 7% to 14.22 mnt) indicate subdued import demand. Baltic shipping indices showed mixed movement, with the Panamax and Supramax segments weakening slightly, suggesting ongoing pressure on global freight markets.

Leave a Reply