- Global prices firm on balanced demand, tight vessel supply

- Chinese coke prices hint at modest rebound post-sustained cuts

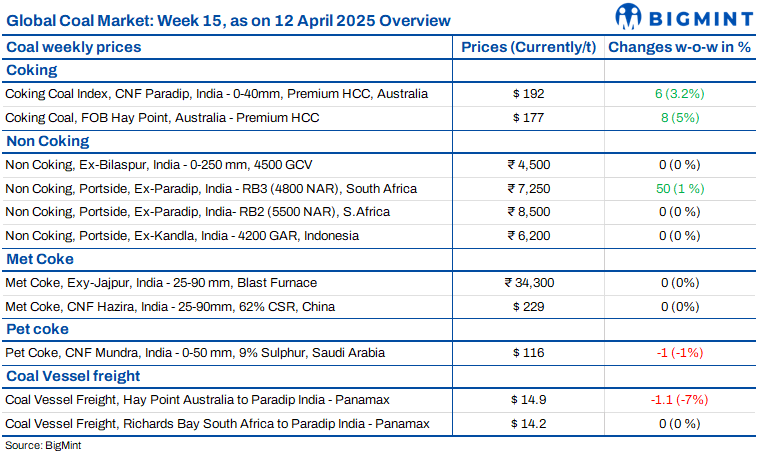

The overall sentiment across India’s coal and coke markets remained largely stable and cautious this week. Prices of Indonesian and South African coal held firm amid balanced demand, adequate stocks, and tight vessel availability. Domestic coal and met coke prices also remained unchanged as traders resisted cuts despite subdued demand. Pet coke markets mirrored this tren, refiners mostly maintained rates, and imports fell slightly on rising US supplies and soft buying interest. Freight rates declined on vessel surplus, adding to the muted tone. While Chinese coke markets hint at a modest rebound, Indian markets continue to adopt a wait-and-watch approach amid restricted bullish triggers.

India’s portside prices of Indonesian thermal coal steady

Portside prices of Indonesian thermal coal in India remained stable w-o-w, reflecting steady market sentiment. As of 11 April, prices of the 5000 GAR held at INR 7,800/t at Kandla, while the 3400 GAR was at INR 4,950/t at Navlakhi. The 4200 GAR remained steady at INR 6,200/t at Kandla and INR 6,100/t at Vizag. Despite modest demand recovery expectations, the market continues to exhibit balance with adequate portside inventories and subdued trading activity. Coal stocks at Indian ports rose slightly by 0.2% to 12.31 million tonnes (mnt), while power plant inventories declined slightly to around 58 mnt. In Indonesia, coal prices fluctuated slightly, with mid and low-CV grades becoming slightly more expensive.

South African prices in India stable

Portside South African thermal coal prices in India remained steady w-o-w amid weak steel market sentiments. RB2 (5500 NAR) was assessed at INR 8,450/t exw-Gangavaram and INR 8,500-8,600/t at Paradip, while RB3 (4800 NAR) held at INR 7,200-7,350/t across ports. Exw-Vizag RB2 offers stood firm at INR 8,200-8,300/t. Despite a decline of INR 450/t in sponge iron prices to INR 27,550/t exw-Rourkela, coal prices held up due to tight vessel availability and balanced cargo demand. Freight from RBCT to Paradip remained unchanged at $14.2/t. Internationally, RB2 offers stayed at $76/t FOB, while RB3 rose slightly to $63/t amid tighter supplies. Prices are likely to remain range-bound amid cautious demand.

India’s domestic coal prices stable

Domestic coal prices in India remained steady this week, with 4500 GCV and 5000 GCV grades assessed at INR 4,500/t and INR 4,950/t exw-Bilaspur, respectively. Traders held firm on their offers, citing that current prices have already touched base levels. While some buyer inquiries were noted in the market, most negotiations hovered around prevailing prices. No upward movement was observed in offer levels. Despite weak buying interest, sellers avoided further reductions to prevent margin compression. The market continues to adopt a wait-and-watch approach amid limited triggers for price fluctuations, maintaining a cautious tone on both the demand and supply sides.

Domestic met coke steady as market stays cautious

Domestic met coke prices in India remained stable w-o-w amid cautious market sentiments and rising global coking coal prices. As per BigMint, BF-grade coke (25-90 mm) was priced at INR 34,300/t exw-Jajpur and INR 32,300/t exw-Gandhidham. Indian mills booked Colombian cargoes at around $263-265/t CFR for June delivery, but a broader price hike is facing resistance. Chinese mills pushed back against the proposed RMB 50-55/t hikes, citing weak demand and low margins.

Meanwhile, Australian PHCC prices rose by $8/t to $177/t FOB due to supply concerns close on the heels of mine accidents. With pig iron prices falling and domestic coke output rising in eastern India, prices are expected to stay stable next week.

China met coke prices may rise in April

Chinese metallurgical coke prices are expected to rise slightly in April 2025, supported by a gradual pick-up in demand from steelmakers, as per Mysteel. Mills have resumed restocking as margins improve, providing room to absorb higher input costs. Coke producers, after facing 11 consecutive price cuts since October, are looking to raise their tags. Hot metal output has also climbed up, averaging 2.37 mnt/day over 21-27 March, up 93,400 t/d from a month earlier. Still, with inventories high and coking coal prices mostly stable, only limited price increases are likely. One or two modest hikes may occur this month, especially around the Qingming Festival, but any major rebound remains uncertain.

Indian refiners roll over Apr pet coke; RIL stays out

Indian refineries have mostly kept their pet coke prices unchanged for April 2025. Reliance Industries (RIL), however, skipped any offers again, continuing to channel all production to its gasification units and sourcing pet coke from IOCL’s Koyali refinery to meet internal needs. Nayara Energy maintained its premium, rolling over prices at INR 14,930/t – up 12.4% y-o-y. MRPL also held steady at INR 11,670/t (road) and INR 11,370/t (rake/barge), reflecting a 17.3% y-o-y increase. BPCL’s Bina refinery raised rake-supply prices by INR 853/t to INR 15,150/t, while Kochi hiked rates marginally to INR 12,800/t. The price gap between Bina and Kochi widened to INR 2,350/t this month.

India’s imported pet coke prices drop

Imported pet coke prices in India declined by $2-3/tonne w-o-w due to improved availability from the US and sluggish demand. West coast offers dropped to $115-116/t CFR, while east coast prices slipped to $116-118/t CFR. With US pet coke shipments to China halted by tariffs, excess volumes are now being diverted to India, increasing supply pressure. Indian buyers are leveraging this to negotiate lower prices. However, Saudi-origin pet coke remains more expensive, as Chinese demand continues to absorb those shipments. The overall pricing trend reflects a softening market, driven by oversupply and tepid buying interest from Indian end-users.

India’s coal freights fall w-o-w on vessel availability

Coal freight rates in India declined w-o-w due to an oversupply of vessels in the Pacific, especially around North Pacific and Australia. A lack of fresh cargo enquiries and weak coal shipment volumes have given charterers the upper hand in rate negotiations. Thermal coal inventories at Indian ports edged up slightly to 12.31 mnt. The Baltic Dry Index dropped 113 points w-o-w to 1,489, while the Panamax and Supramax indices also declined. Freight from Australia to Paradip fell by $1.10/t to $14.9/t. Rates from East Kalimantan to Paradip dipped $0.6/t to $13.3/t, while South Africa-India freights remained flat at $14.2/t due to limited vessel supply.

Leave a Reply