- Indonesian demand average, mostly from textiles, ceramics

- SA RB2 prices firm amid sluggish sponge iron demand

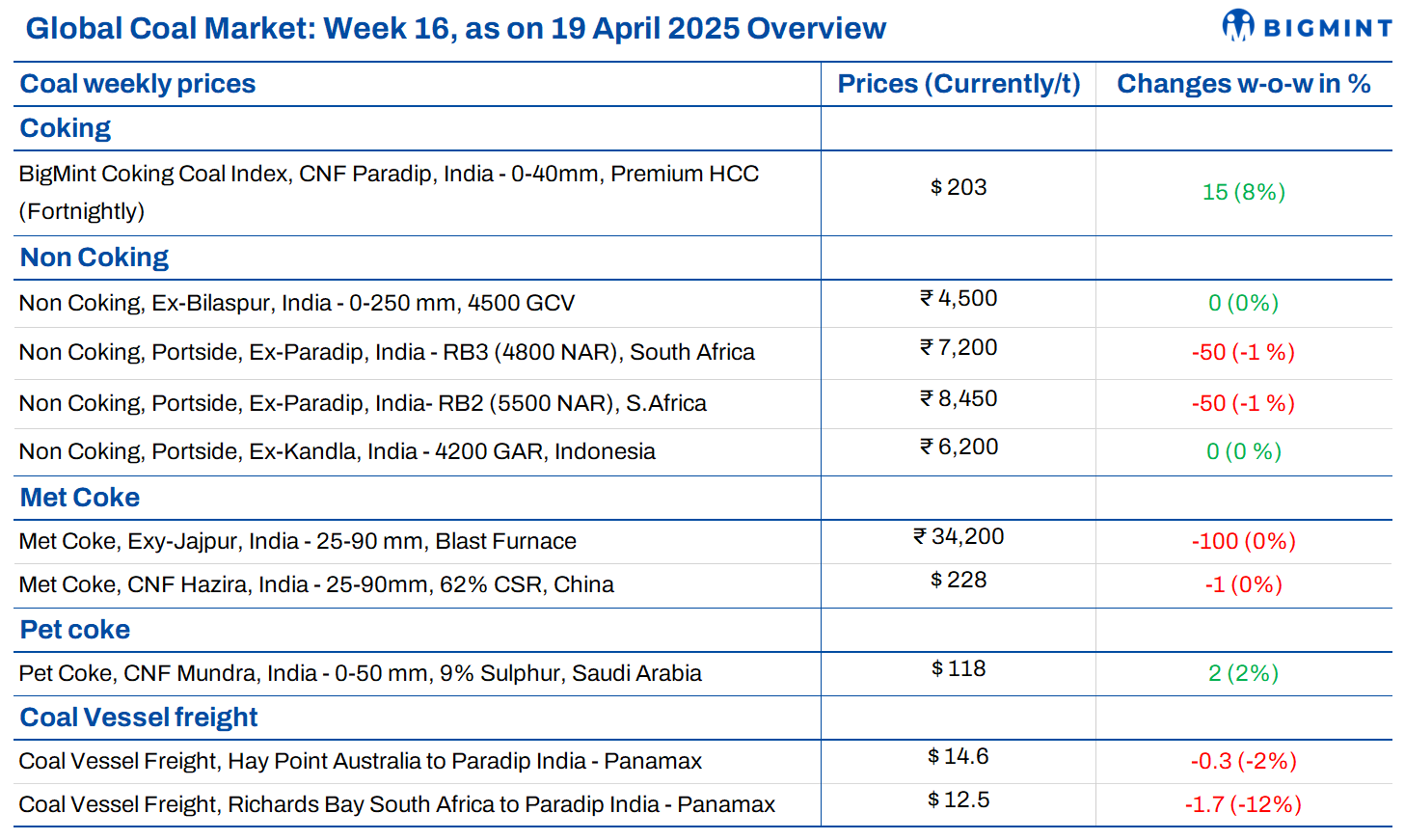

The overall sentiment in India’s coal markets remained largely steady amid cautious demand. Portside Indonesian thermal coal prices showed no weekly change, reflecting balanced supply-demand conditions. Coal stocks at ports and power plants edged up slightly, offering some buffer. South African RB2 and RB3 prices remained mostly stable amid weak sponge iron demand. Internationally, Indonesian low-CV coal prices firmed up, while high-CV grades dipped. India’s domestic met coke and pet coke prices held flat despite rising input costs. However, coking coal prices surged on tighter supplies.

0.23 mnt coal sold in SECL auction – South Eastern Coalfields Limited (SECL) conducted a spot e-auction on 10 April 2025, allocating 232,600 tonnes (0.23 mnt) of non-coking coal across six grades. G6 emerged as the most allocated grade, forming 62% of the total volume, with strong buyer interest pushing bid premiums up to 44% above the notified prices.

Portside Indonesian prices steady w-o-w; power plants stocks up

The Indian portside market for Indonesian thermal coal remained stable w-o-w, with moderate need-based demand from sectors like ceramics and textiles. Prices were unchanged, with the 5000 GAR at Kandla at INR 7,800/t. The 4200 GAR was at INR 6,200/t (Kandla) and INR 6,100/t (Vizag), while the 3400 GAR at Navlakhi hovered at INR 4,900/t. Portside stocks inched up 0.2% to 12.33 mnt, while coal inventory at power plants rose to 58.36 mnt, enough for 20 days. However, 22 plants still face critically low stocks. Meanwhile, Indonesian index prices showed mixed trends, with 5800 GAR falling $0.93/t to $81.59/t, while 3400 GAR gained slightly to $33.15/t.

SA RB2 holds firm in east coast; demand weak

Portside prices of South African (SA) coals in India remained mostly stable this week. RB2 (5500 NAR) offers were unchanged at INR 8,450/t ex-Gangavaram, while RB3 (4800 NAR) held at INR 7,200/t. At Paradip, RB2 slipped slightly to INR 8,350/t, and RB3 remained flat. In Vizag, RB2 stood at INR 8,300/t and RB3 at INR 7,150/t. Two RB2 deals, totalling 54,000 t were reported at INR 8,400/t ex-Dhamra. Weak buying due to sluggish sponge iron demand continued to weigh on prices. Export offers from South Africa moved up slightly with RB2 at $76.5/t FOB and RB3 at $63.5/t. Domestic coal rates remained steady, while sponge iron dropped by INR 400/t to INR 27,150/t exw-Rourkela.

Met coke holds steady even as coal costs climb

Domestic met coke prices in India stayed unchanged w-o-w despite a notable surge in coking coal costs. BigMint assessed blast furnace grade (25-90 mm) coke at INR 34,200/t exw-Jajpur and INR 32,200/t exw-Gandhidham. Buyers remained cautious amid volatile coal prices. The imported met coke market stayed inactive, with only two recent Colombian cargo deals at $263-265/t CFR. Meanwhile, Australian coking coal rose to $183/t FOB mid-April, up from the March low of $166/t, due to mine disruptions. China’s met coke prices also saw their first hike since October.

BigMint PHCC index-rebounds $15/t on tight Aussie supply

BigMint’s premium hard coking coal (PHCC) index rose by $15/t m-o-m, assessed at $203/t CNF Paradip on 15 April 2025, up from $188/t on 31 March. The hike came amid global supply tightness, especially from Australia, where spot market availability remains low. Australian PHCC prices bounced back from a four-year low of $166/t FOB in March to $182/t FOB by mid-April, driven by disruptions at Moranbah North and Appin mines. Where India’s demand is concerned, March 2025 coking coal imports rose to 4.9 million tonnes (mnt), up 23% from 4.0 mnt in February. Meanwhile, Chinese met coke prices edged up by RMB 50-55/t for the first time since October 2024.

Pet coke rates steady in Apr; no change across IOCL refineries

Indian Oil Corporation Ltd (IOCL) has kept petroleum coke prices unchanged for April 2025 deliveries across all its refineries. At the Koyali refinery, road supply was priced at INR 12,960/tonne and rake at INR 12,760/tonne. Panipat maintained a higher price of INR 13,900/tonne. Both road and rake prices at Paradip and Haldia stayed steady. Export rates to Nepal and Bhutan also saw no m-o-m movement – with Paradip at INR 13,490/tonne and Haldia at INR 13,360/tonne. The flat pricing reflects stability in the domestic and nearby export markets for the month

Mixed trends in imported pet coke: US drops, Saudi holds for Apr

Imported pet coke prices in India moved in opposite directions this week. On the east coast, US-origin offers were at $112/t CFR, while Saudi-origin remained firm at $120/t CFR, with sellers continuing to prioritise Chinese buyers. On the west coast, offers for both origins dropped by $2-3/t w-o-w. US cargoes saw a sharper fall of $4-5/t due to better availability. In contrast, Saudi offers held steady, supported by limited supply.

Coal freights decline on muted demand, vessel oversupply

Coal shipping freights to India fell w-o-w amid sluggish demand and thin cargo activity in the Pacific. Oversupply of vessels and limited bookings for prompt shipments dragged rates down, while easing bunker fuel costs offered only marginal relief. BigMint assessed Australia-India rates at $14.6/t, down $0.3/t w-o-w, with SAIL fixing two vessels to Vizag at $14.75/t for May. Meanwhile, thermal coal inventories at Indian ports rose slightly to 12.33 mnt. Baltic indices also declined, with the Panamax Index falling 239 points w-o-w, reflecting waning vessel demand.

Leave a Reply