Indonesian non-coking coal prices fall at Indian ports

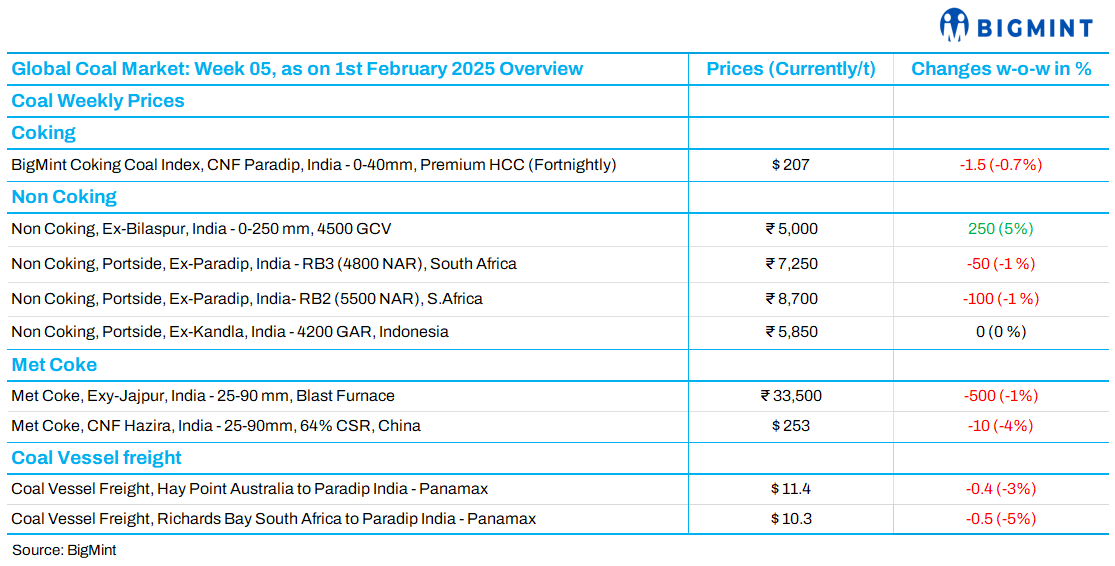

Portside prices of Indonesian non-coking coal in India declined by INR 100-200/t w-o-w due to weak demand and sufficient inventory. Prices for 3400 GAR at Navlakhi dropped to INR 4,450/t, while 5000 GAR at Kandla fell to INR 7,600/t. Prices for 4200 GAR at Kandla and Vizag remained unchanged at INR 5,850/t and INR 5,750/t, respectively. Global prices also fell, with 5800 GAR coal down by $0.48/t to $86/t FOB. Mid-CV (4200 GAR) coal dropped by $0.20/t to $48.56/t, while 3400 GAR declined by $0.12/t to $29.70/t. With ample supply and weak demand due to the Chinese New Year holidays, both portside and imported coal prices are expected to remain under pressure in the near term.

South African thermal coal prices decline at Indian ports

Portside prices of South African thermal coal in India declined as weak demand and selling pressure persisted. RB2 (5500 NAR) coal prices fell by INR 100/t to INR 8,700/t, while RB3 (4800 NAR) declined by INR 50/t to INR 7,250/t at Gangavaram. South African RB2 export offers dropped by $1/t to $81/t FOB, while RB3 remained steady at $61.5/t FOB. Thermal coal inventories at Indian ports fell by 4% to 13.34 mnt in week 4 of 2025. Despite lower stocks, limited inquiries and availability of domestic alternatives pressured prices. Domestic 5000 GCV coal rose to INR 5,900/t, up INR 350/t, but buying remained slow. Portside prices are expected to remain weak amid subdued demand and selling pressure from traders.

Domestic thermal coal prices increase after SECL auction

Domestic thermal coal prices in India rose week-on-week following the recent SECL auction. Prices for 4500 GCV coal increased by INR 250/t to INR 5,000/t, while 5000 GCV coal rose by INR 350/t to INR 5,900/t, both exw-Bilaspur. Despite the price hike, trading activity remained sluggish as buyers avoided bulk purchases, anticipating market stability. Sponge iron prices saw an uptick, but limited demand kept coal trades muted. Buyers are closely monitoring price movements before making further procurement decisions.

Indian met coke prices remain stable

India’s domestic met coke prices held steady this week, with 25-90 mm blast furnace (BF) grade coke assessed at INR 33,500/t exw-Jajpur and INR 31,500/t exw-Gandhidham. Around 40,000 t of BF-grade coke were traded at INR 32,000-33,000/t exw-Jajpur, while another 25,000 t changed hands at INR 34,000/t exw-Jajpur. Market sentiment remained firm due to declining port stocks and limited fresh import bookings. Polish coke remained viable at $300/t FOB, while Colombian coke stood at $350/t CFR India. Australian PHCC prices dipped $2/t w-o-w to $186/t FOB amid thin liquidity. Indian pig iron prices recovered by INR 300/t w-o-w to INR 33,300/t exw-Durgapur, supported by improved trades and stronger steel market conditions.

Bigmint’s coking coal index declines amid weak global sentiment

BigMint’s premium hard coking coal (PHCC) index dropped to $207/t CNF Paradip on 31 January, down from $208.5/t on 15 January, as weak global sentiment and bid-offer disparities limited trade. Sellers offered at $215/t CFR India, while buyers sought $205-210/t. An Indian mill booked 40,000 t of Australian PHCC at $205/t CFR for early February loading. Australian PHCC prices fell by $8/t to $186/t FOB, pressured by low liquidity and weak Chinese demand. India’s domestic met coke prices remained stable, with BF-grade at INR 33,500/t exw-Jajpur. Coking coal prices may stay under pressure due to the Lunar New Year holidays, while Indian demand trends will become clearer post-Budget 2025.

RIL begins sourcing pet coke from IOCL Koyali

Reliance Industries Limited (RIL) has started sourcing pet coke from Indian Oil Corporation Limited’s (IOCL) Koyali refinery from January 2025, lifting around 22,000 t this month. This accounts for one-third of Koyali’s 70,000 t monthly production. Meanwhile, RIL has halted its own pet coke sales since December 2024 to prioritise gasification unit operations. To meet demand, RIL is procuring pet coke from multiple sources, including imports. Its 10 gasifiers, consuming up to 2,900 tpd each, require more pet coke than RIL’s total production of 7.2 mnt. RIL has dynamically adjusted its pet coke production, imports, and sales based on gasification unit operations, even exporting small volumes when pricing was favourable.

India: Coal freight rates decline

Coal freight rates in India softened w-o-w due to muted market activity and weak cargo inquiries. Despite lower vessel supply, time-charter rates remained under pressure. Freight derivatives and declining bunker prices further impacted market sentiment. Baltic indices fell sharply, with the Baltic Dry Index dropping 209 points to 778 on 27 January. Freight rates from Australia to Paradip fell by $0.4/t to $11.4/t, South Africa to Paradip declined by $0.5/t to $10.3/t, and Indonesia to Paradip dropped by $0.6/t to $8.3/t. Some traders reported even lower rates for South African shipments at $9-9.5/t. Limited demand and weak chartering activity may keep freight rates subdued in the near term.

Leave a Reply