- Asian and Middle Eastern markets stay subdued

- Turkish scrap inches up despite cautious market sentiment

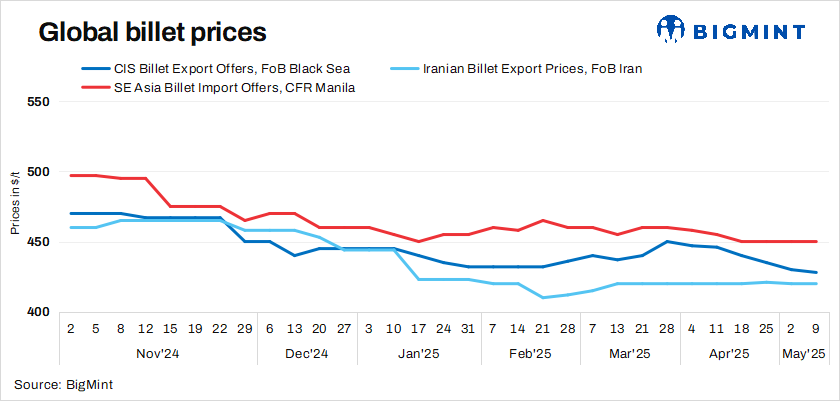

In the 19th week of CY’25, global billet prices across Southeast Asia held largely steady, reflecting a market still in search of stronger direction. While there are early signs of recovery in downstream sectors and some pickup in trading interest, overall activity remains measured. Market participants appear cautiously optimistic but are holding back from major commitments as they await clearer signals on demand strength and pricing momentum. This wait-and-see approach continues to shape sentiment, keeping the market in a state of cautious equilibrium.

The Turkish deep-sea imported scrap market saw a modest rebound. The uptick in prices is being driven by rising collection costs in both Europe and the US coupled with improving sentiment in the rebar market. US-origin HMS 80:20 bulk scrap was assessed at $340/t CFR Turkiye, reflecting a $12/t w-o-w increase. Market participants signalled expectations of further price gains, citing ongoing supply constraints and strategic restocking efforts as potential catalysts.

Asian markets showed mixed trends this week, with Vietnam seeing a modest boost in longs demand driven by upcoming projects and construction activity. In contrast, China’s billet market opened post-holiday with brief optimism, but prices soon lost momentum amid weak demand and rising inventories.

Market highlights

- Billet prices in the Philippines remained stable w-o-w at $450/t CFR Manila for 5sp grade as of 9 May, unchanged from the previous week, sources informed BigMint. Despite the steady pricing, buying interest continues to remain weak in the market. BigMint’s Russian billet index, FOB Black Sea, Russia dipped w-o-w by $2/t to $428/t.

- The Vietnamese billet market remained subdued, with no major bulk deals reported, although some export offers emerged at around $440/t in week 19. On the domestic front, demand for longs saw a marked increase following the recent holidays, largely driven by renewed construction activity. This recovery in downstream demand is expected to prompt scrap importers to resume restocking, as mills signal a gradual return to the market after a period of caution. However, the export outlook remains under pressure, with recent U.S. tariffs casting a shadow over Vietnam’s outbound billet trade.

- Iran’s semi-finished steel market remained stable at $420/t FOB, w-o-w. No major new tenders have been heard followed KSC and Arfa. Domestic demand improved mid-week, but regional instability post-April blast continues to disrupt port operations.

Leave a Reply