- Firmer Australia, Canada flows offset weaker Brazil, Peru shipments

- Weak steel output, high iron ore port stocks in China keep outlook muted

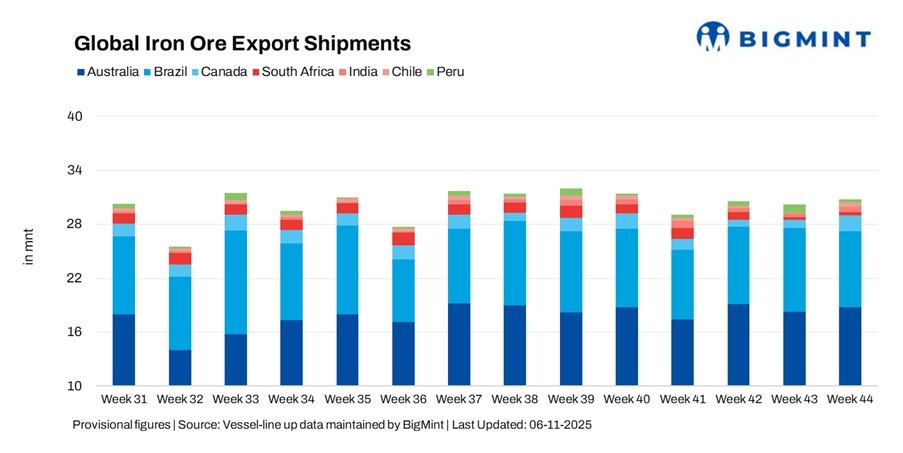

Global iron ore exports rose 2% w-o-w to 30.74 mnt in week 44 (25-31 October 2025), compared with 30.14 mnt in week 43 (18-24 October). The week saw a modest rebound, driven mainly by stronger shipments from Australia and a sharp recovery in Canada, which partially offset softer volumes from Brazil and Peru.

Despite the rise, overall momentum remained subdued as weaker Chinese restocking and high port inventories limited cargo pull. Lower freights offered some cost relief to miners, aiding loading activity at key ports.

In the broader context, China’s steel output remained weak, and portside iron ore inventories reached recent highs — signalling that unless steel demand strengthens, export growth could stay range-bound through early November.

Australia’s iron ore exports climbed 2.7% w-o-w to 18.82 mnt, from 18.33 mnt in week 43. Miners marginally stepped up shipments from the Pilbara region, supported by steady loading activity across key ports — Port Hedland (10.98 mnt), Walcott (4.25 mnt), and Dampier (3.19 mnt). The easing of voyage rates encouraged miners to fix vessels promptly, resulting in improved throughput.

Among major shippers, Rio Tinto exported 7.44 mnt, BHP 6.24 mnt, and FMG 3.01 mnt, together accounting for over 85% of Australia’s total shipments. On the destination side, China remained the dominant buyer at 16.12 mnt, followed by Japan (1.18 mnt) and South Korea (0.82 mnt).

Meanwhile, fresh reports indicated that China Mineral Resources Group (CMRG) has instructed mills to pause spot purchases from BHP amid ongoing pricing negotiations — a move that could influence future scheduling and miner strategies if tensions persist.

Brazil’s exports fell sharply by 9.8% w-o-w to 8.35 mnt from 9.26 mnt in week 43. Reduced shipments from Ponta da Madeira (3.54 mnt), Itaguai (1.86 mnt) and Tubarao (1.46 mnt) contributed to the decline, reflecting maintenance-related disruptions and weaker loading performance. Vale, the country’s largest exporter (4.20 mnt), curtailed loadings amid lower chartering activity and subdued Chinese demand.

Shipments to China dropped notably with 4 mnt, while flows to Europe and the Middle East remained broadly stable. The slowdown also aligned with weaker Capesize freight levels on the Brazil-China route, discouraging fresh fixtures.

The near-term outlook remains soft as weather-related disruptions and limited mining throughput continue to weigh on weekly volumes.

Canadian iron ore exports doubled, rising 110% w-o-w to 1.79 mnt from 0.85 mnt in the prior week, marking a strong rebound after logistical delays earlier in October. Improved rail connectivity to Quebec’s loading terminals — Sept Iles (1.20 mnt) and Port Cartier (0.59 mnt) — enabled miners to clear accumulated cargoes.

IOC led shipments with 0.66 mnt, followed by AMNS (0.59 mnt) and Guinea and Nimba mines (0.54 mnt), together accounting for the bulk of total exports.

Exports were primarily directed to European destinations (0.44 mnt), while interest from South Korean mills (0.19 mnt) also showed signs of improvement. The recovery in Canadian flows proved timely, as declining freights made long-haul shipments more competitive and encouraged exporters to capitalise on the softer freight environment.

South Africa’s iron ore exports rose modestly to 0.38 mnt in week 44 from 0.29 mnt a week earlier, marking a slight recovery after several weeks of subdued activity. The uptick was supported by improved loading performance at Saldanha Bay (0.19 mnt) and Richards Bay (0.18 mnt), although overall volumes stayed constrained amid ongoing rail bottlenecks that continue to limit cargo movement from inland mines to ports.

China remained the primary destination, taking around 0.17 mnt, while Indian mills showed renewed buying interest in low-grade fines amid lower freight costs. Despite the mild rebound, persistent operational disruptions and vessel congestion at Saldanha could cap further recovery through November, keeping South Africa’s export outlook cautious in the near term.

India’s iron ore exports increased by 12% w-o-w to 0.47 mnt in week 44, up from 0.42 mnt in the previous week, aided by improved loading activity at Paradip (0.13 mnt) and Dhamra (0.11 mnt) ports. The rebound was driven by greater participation from eastern India-based miners, particularly in Odisha, who resumed shipments following the recent holiday lull and improved vessel turnaround at loading terminals.

China remained the primary destination, receiving around 0.23 mnt, while other Asian buyers showed limited interest amid weaker steel margins. Exporters benefited from easing Supramax freights, which helped offset narrowing profit margins caused by softer iron ore prices and cautious overseas demand.

Chile’s iron ore exports surged to 0.49 mnt in week 44, rebounding sharply from a recent low of 0.10 mnt in week 43. The recovery was supported by renewed loading activity at Totoralillo (0.20 mnt) and Huasco (0.17 mnt) ports, as improved weather and steady mine dispatches helped normalise operations.

China (0.25 mnt) and South Korea (0.20 mnt) were the leading importers, reflecting revived demand for medium-grade cargoes amid lower freight costs and opportunistic restocking.

In contrast, Peru’s iron ore exports declined sharply by 50% w-o-w to 0.44 mnt from 0.89 mnt, primarily due to weather-related disruptions along the Pacific coast and reduced loading activity at San Nicolas (0.33 mnt) and Matarani (0.12 mnt). Although buying interest from China (0.17 mnt) and Japan (0.16 mnt) remained steady, logistical challenges and port delays restricted overall shipments. Shipper Shougang Hierro led export activity, contributing 0.33 mnt, but the operational slowdown curbed the country’s total outbound volumes for the week.

Freight market slips on weak demand

Dry bulk iron ore freights fell w-o-w as vessel earnings declined across both the Pacific and Atlantic basins. The market was weighed down by muted cargo demand, ample tonnage availability, and subdued chartering activity.

Weak Chinese restocking and high inventories with buyers curtailed miner interest in prompt fixtures, leading to lower rates on key routes such as Australia-China, Brazil-China, and South Africa-China.

The overall tone stayed bearish through the week, reinforced by falling FFA values and softer bunker prices. While reduced freights offered marginal cost benefits to miners, they also reflected tepid trading sentiment, hinting at slower shipment momentum into early November.

Outlook

The near-term outlook for the iron ore trade remains cautiously soft. While Australian and Canadian loadings may continue to support headline export volumes, weaker Chinese demand, elevated port stocks, and freight market oversupply could restrain any sustained gains.

Some seasonal demand recovery may emerge as charterers return post-holiday and weather disruptions affect vessel schedules in November. However, meaningful upside will hinge on steel output recovery in China and consistent miner-level shipment scheduling across key exporting regions.

Leave a Reply