- Australian shipments rise, Brazil, South Africa see declines

- Freight softness in Pacific basin limits upside momentum

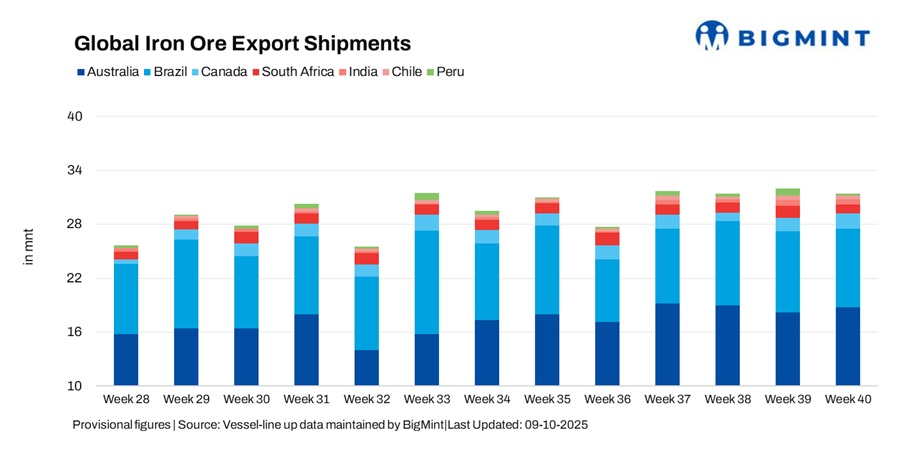

Global iron ore exports edged lower in Week 40 (27 September-3 October 2025), falling 2.3% w-o-w to 31.32 million tonnes (mnt) from 32.07 mnt in Week 39. The marginal decline came despite a rebound in exports from Australia and Canada, as sharper drops in Brazil, South Africa, Chile, and Peru pulled the global total lower.

Market participants highlighted that Pacific freight weakness and subdued Chinese demand continued to limit upside potential, even as operational recovery and restocking support lifted shipments from Australia. Meanwhile, Atlantic basin flows softened amid cautious chartering sentiment and weather-linked disruptions.

Country-wise trends

Australia: Australia’s iron ore exports rose 3.1% w-o-w to 18.76 mnt in Week 40, supported by smoother port operations, cargo clearance, and slightly stronger restocking demand from Chinese mills ahead of Golden Week. Port Hedland handled 11.23 mnt, Dampier 3.54 mnt, and Walcott 3.58 mnt. Rio Tinto led exports at 7.11 mnt, followed by BHP 5.74 mnt and FMG 4.54 mnt. While flows improved, market sentiment remained cautious due to softer Pacific freight rates and the ongoing China-BHP pricing dispute.

The standoff with China Mineral Resources Group (CMRG) could drag into early 2026. So far, BHP’s shipments remain largely unaffected, as most November-December cargoes were already sold. Around 50 cargoes offered post-suspension have gone to international traders and at least one Chinese buyer, with any major impact expected from January-delivery sales.

CMRG, set up to negotiate long-term contracts for China’s steel mills, has taken a tougher approach to secure better prices and discounts from BHP, Rio Tinto, and Vale, showing Beijing’s push for more bargaining power in the world’s largest iron ore market.

Brazil: Brazil’s iron ore exports fell 3.4% w-o-w to 8.68 mnt in Week 40 from 8.98 mnt in Week 39, primarily due to slower fixture activity and softer chartering sentiment in the Atlantic. While loadings at key ports – Ponta da Madeira (3.32 mnt), Itaguai (2.16 mnt), and Tubarao (1.46 mnt) remained stable, shipment volumes were capped by freight-related delays and weaker buying from Chinese mills.

Vale led exports with 4.22 mnt, although some cargoes were postponed because of limited vessel availability. Market sources noted that, despite a slight improvement in Atlantic freight rates, restricted fixture activity prevented Brazil from converting the rate gains into higher export volumes. China continued to dominate as the main buyer, lifting around 3.95 mnt of Brazilian cargoes.

Canada: Canada’s iron ore exports rose 13.3% w-o-w to 1.71 mnt from 1.51 mnt in Week 40, driven largely by improved weather conditions and smoother port operations, which eased logistical bottlenecks. Port Cartier handled 1.03 mnt while Sept-Iles recorded 0.68 mnt, reflecting more efficient vessel turnaround and reduced operational delays compared with the previous week. AMNS India was the leading shipper, contributing nearly 1.03 mnt, followed by Guinea and Nimba Mines (0.4 mnt) and IOC (0.3 mnt).

Market sources noted that although the week’s rebound was substantial, it was primarily technical in nature rather than driven by stronger underlying demand. While the weekly increase provided a temporary boost to overall Canadian exports, sustained growth will depend on stronger demand fundamentals in key markets.

South Africa: South Africa’s iron ore exports declined sharply by 29.5% w-o-w to 0.98 mnt from 1.39 mnt, as logistical bottlenecks and limited vessel availability constrained shipments. Saldanha Bay accounted for 0.81 mnt and Richards Bay 0.17 mnt, but ongoing rail disruptions and a shortage of available tonnage significantly curtailed overall export volumes.

South Korea (0.29 mnt) and Japan (0.17 mnt) were the main destinations, although volumes to Asia were notably lower compared with previous weeks. While Chinese demand remained steady, persistent infrastructural challenges, coupled with elevated freight costs, restricted throughput and prevented South Africa from fully capitalizing on market opportunities. Market participants noted that unless rail and port operations stabilize, the country’s export performance is likely to remain under pressure in the near term.

India: India’s iron ore exports slipped 5.1% w-o-w to 0.56 mnt from 0.59 mnt, as uncertainty over a potential export duty continued to weigh on market sentiment. Paradip led shipments with 0.27 mnt, while smaller volumes moved from Mormugao and Dhamra. Market sources noted that softer Supramax freight rates on the India-China route further discouraged new bookings. China remained the primary destination, lifting around 0.30 mnt of Indian cargoes, while minor parcels were shipped to Southeast Asian buyers.

Additionally, with China observing Golden Week holidays, shipments may temporarily slow as mills adjust restocking and port operations pause. Overall, the combination of policy uncertainty, subdued freight conditions, and the holiday period constrained export activity, limiting India’s ability to capitalize on regional demand.

Chile: Chile’s iron ore exports fell 22.5% w-o-w to 0.43 mnt from 0.55 mnt, following a week of strong catch-up loadings. Shipments from Huasco (0.20 mnt) and Totoralillo (0.17 mnt) eased as operational schedules returned to normal.

Despite continued demand from China (0.20 mnt) and South Korea (0.17 mnt), limited cargo availability and weaker short-term freight economics constrained export volumes, slowing overall momentum.

Peru: Peru’s shipments dropped 75.3% w-o-w to 0.21 mnt from 0.85 mnt, as earlier backlog clearances gave way to reduced port activity. San Nicolas (0.17 mnt) and Matarani (0.04 mnt) saw limited movement, with all volumes destined for South Korea at 0.17 mnt.

Shougang Hierro led exports with around 0.17 mnt, though operations were constrained by infrastructure issues and vessel scheduling gaps.

Freight market trends

Dry bulk iron ore freight markets displayed mixed trends during Week 40. Rates in the Pacific basin weakened, particularly on the Australia-China route, where chartering activity slowed following China’s reported pause on BHP cargo purchases. Reduced fixture levels and softer bidding weighed on sentiment; even as Australian shipments rose modestly on improved operational conditions.

In contrast, Atlantic basin rates for the Brazil-China and South Africa-China routes edged higher, supported by limited fixtures and tight vessel supply. However, overall sentiment stayed cautious, with the Baltic index falling and Dalian iron ore futures easing on weak Chinese macro data.

Outlook

Global iron ore exports are expected to remain range-bound in the near term, as freight volatility and cautious Chinese procurement continue to shape market activity. Australia’s rebound signals operational normalisation, but shipments may fluctuate with ongoing uncertainty over BHP’s pricing negotiations. Brazil’s flows could stabilise if Atlantic fixture activity holds, while Canada’s export momentum may ease after clearing delayed volumes.

India’s flows may stay muted amid weak Supramax sentiment. Smaller South American exporters such as Chile and Peru are expected to see intermittent volumes. Freight trends will remain the key driver-Pacific softness may constrain upside, while Atlantic resilience could provide limited balance to global iron ore trade.

Leave a Reply