- Wide bid-offer gaps keep imported scrap trade thin

- Heavy rains, flooding slow construction demand

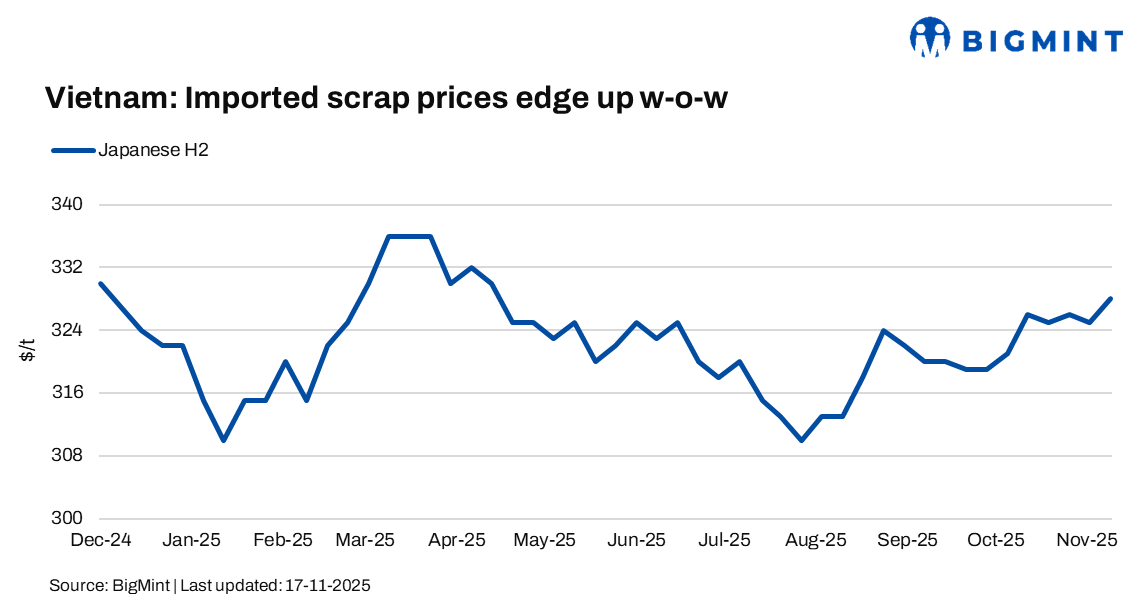

Vietnam’s imported ferrous scrap prices inched up w-o-w, supported by intermittent restocking in the north. However, widespread flooding and persistent storms disrupted logistics and stalled construction activity, keeping mills cautious and limiting bulk bookings.

The November 2025 Kanto export tender posted a moderate m-o-m rise of JPY 644/t ($4/t). A 20,000-t H2 cargo was reportedly awarded to a Vietnam-based mill at JPY 44,960/t ($291/t) FAS Japan. This increase in the Kanto tender bids also contributed to the rise in Vietnam’s imported scrap prices.

Weekly assessments

- Japanese H2 scrap was at $328/t CFR, up by $3/t w-o-w.

- US-origin HMS 80:20 bulk stood at $348/t CFR Vietnam, up by $3/t w-o-w.

Market updates

H2 offers mostly ranged between $326-333/t CFR, with a few suppliers reducing quotes to around $328/t amid soft liquidity. Bids improved slightly to around $325/t CFR, compared with $320-325/t CFR last week, marking a steady trend for the third consecutive week.

Wide bid-offer gaps kept imported scrap trade thin. Deep-sea HMS 80:20 bulk offers remained firm at $350/t CFR, while bids held at $335-340/t. Containerised US-origin HMS remained at $300-305/t CFR, though some southern mills bid $285-290/t due to weak procurement needs.

A trader noted that while H2 prices received some support from a weaker JPY, Vietnamese mills continued to prefer small-volume or containerised scrap because domestic steel demand remained weak, and inventory levels were comfortable.

Domestic updates

Finished steel and semis prices remained largely stable, yet mills continued buying only in small lots to replenish near-term requirements. Domestic HMS (3-6 mm) was heard at $303-346/t in the south and $329-362/t in the north (ex-VAT). Mills leaned towards local scrap due to quicker delivery and lower cost, especially as flooding delayed the handling of imported vessels.

Outlook

Market conditions are expected to remain stable but subdued in the near term. Flooding, vessel delays, and weak construction activity will likely cap any immediate price upside. While a softer yen may lend some support to Japanese offers, Vietnamese mills are expected to remain selective, focusing on small-volume purchases while navigating slow steel demand and ample inventories.

Leave a Reply