Market activities in Vietnam have improved after the prolonged Tet festival holidays. Steel producers and workers are returning to the production facilities after the holidays.

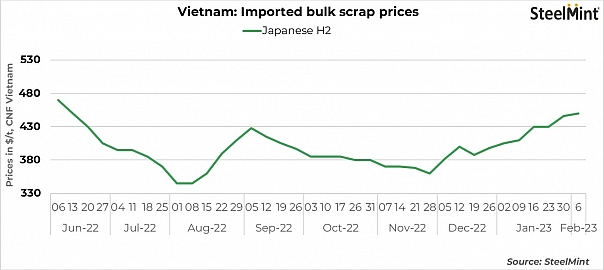

Imported scrap prices in the country increased for the second week in a row. Rumours abounded of some deals being concluded towards last weekend but no confirmation was available with end-users. Prices are likely to rise further ahead of the release of Japan’s Kanto scrap export tender results on 9 February. Most suppliers are waiting to see the price direction after the tender.

Market participants anticipate that the tender will end higher than on 23 January at JPY 50,932/t.

- Indicative offers for Japanese bulk H2 scrap surged to $450/t, up $5/t w-o-w.

- Meanwhile, bulk offers for US-origin HMS 1&2 (80:20) were heard at $460/t CFR, up $5/t w-o-w.

Domestic steelmakers continued to increase rebar prices. After the resumption of market activity late last month, major steelmakers, including Hoa Phat, have announced a hike in rebar prices.

Export offers resume: Vietnam’s BF-grade billet export offers resumed at higher levels post holidays, followed by a hike in the country’s scrap offers. Current offers are at around $610/t FOB. However, no active deals have been reported so far at current offers.

Overview of other South Asian scrap markets

- Thailand: Thailand’s scrap prices for Central American shredded material are at $435-440/t, while 1,000 t HMS (80:20) ex-Caribbean was sold at $425/t CFR LCB basis towards the weekend.

- Indonesia: Offers for imported blue steel/PNS mixed were heard at $455-460/t CFR JKT, up $10/t w-o-w, while HMS (90:10) was quoted at $420/t CFR JKT, up $10/t w-o-w.

Leave a Reply