- US-origin HMS 80:20 fails to attract Vietnam buyers

- Longs market steady on mild construction support

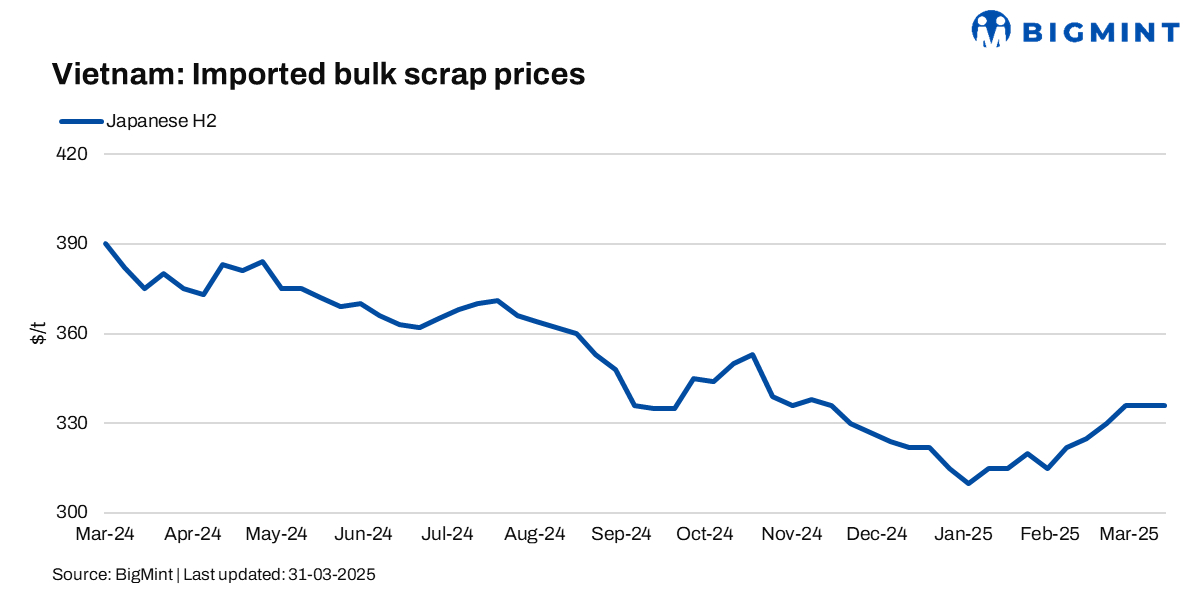

Vietnam’s imported scrap prices remained unchanged last week amid moderate demand. Despite slightly improved finished product sales, mills preferred domestic scrap due to its attractive pricing.

Japanese bulk H2 scrap offers stood at $335-340/t CFR, unchanged w-o-w, supported by a stronger Japanese domestic market. However, Vietnamese buyers were only willing to pay $325-330/t CFR. Meanwhile, US-origin bulk HMS 80:20 was offered at around $370-374/t CFR but failed to attract interest.

A local source noted that high import prices and exchange rate challenges pushed mills to prioritise domestic procurement.

A Vietnamese trader noted that with stable finished product prices, cheaper freight, and a weakening yen, there was little support for Japanese scrap export prices. Meanwhile, for HS and Shindachi, Vietnam bids were lower at JPY 47,000-48,000/t ($315-322/t) FOB.

Vietnam lowers bids for low-grade Japanese scrap

Japanese H2 scrap export offers held steady at JPY 43,000-45,000/t ($288-302/t) FOB, equivalent to $335-340/t CFR Vietnam. However, bids retreated to JPY 42,000-44,000/t ($281-295/t) FOB, down by JPY 1,000/t ($7/t) w-o-w, as Vietnamese mills lowered their bid levels to $320-325/t CFR for lower-grade scrap. This translates to JPY 42,000-42,700/t ($281-286/t) FOB Japan.

CFR assessments

- US-origin HMS 80:20 deep-sea bulk cargoes were assessed at $368/t CFR, stable w-o-w.

- Japanese H2 scrap remained stable w-o-w at $336/t CFR Vietnam.

Vietnam’s domestic scrap prices

In the domestic market, H1-grade scrap traded at VND 8,300-9,100/kg ($325-356/t) DDP, stable w-o-w.

By the last weekend, Type 1 scrap (3-6 mm) was bid at VND 8,700-9,200/kg ($340-360/t) delivered to northern mills (excluding VAT), up VND 100/kg ($4/t) w-o-w, while southern bids fell to VND 8,200/kg ($320/t), down VND 100/kg ($4/t) w-o-w.

Vietnam longs market inches up amid tepid demand

Rebar prices averaged VND 13,450/kg ($526/t) exw, up VND 100/kg ($4/t) from early March. A local trader noted that while long sales improved, rising production kept supply ample, with construction sector demand remaining moderate.

Vietnam books low-priced Japanese, Chinese HRCs; Indonesian offers drop

Vietnamese buyers booked 50,000 t of Japanese SAE1006 HRCs at $508/t CFR for May shipment, significantly below the week’s Japanese offers of $520-530/t CFR. This pressured a major Indonesian mill to cut its June SAE1006 HRC offers to $510-515/t CFR, down from $532/t CFR mid-week.

Meanwhile, buyers secured 20,000-30,000 t of Chinese Q235 HRCs at $470-475/t CFR for May shipment. However, Chinese SAE1006 HRCs remained out of favour due to higher processing costs, coil edge defect risks, and Vietnam’s anti-dumping duty on re-rolling grade HRC with widths up to 1,880 mm, despite stable offers at $490-495/t CFR.

HPG targets stronger financials in 2025

Vietnam’s Hoa Phat Group (HPG) forecasts a 24.7% y-o-y net profit rise to VND 15 trillion ($587 mn) and 21% revenue growth to VND 170 trillion ($6.65 bn) in 2025. Its Dung Quat 2 Complex will add 5.6 mnt HRC capacity, making HPG Vietnam’s largest flats producer (8.6 mnt/year) by 2026.

Outlook

Vietnam’s market is likely to remain stable, supported by improved construction activity, while scrap offers are expected to stay range-bound amid cautious bids.

Leave a Reply