- Tet holidays dampen scrap import activity

- Foreign exchange volatility, freight costs hurt buying sentiment

In Q1CY’25, Vietnam’s ferrous scrap imports fell by 11% y-o-y to 1.25 million tonnes (mnt), down from 1.4 mnt recorded in Q1CY’24.

On a quarterly basis, imports edged down 3% from 1.29 mnt in Q4CY’24.

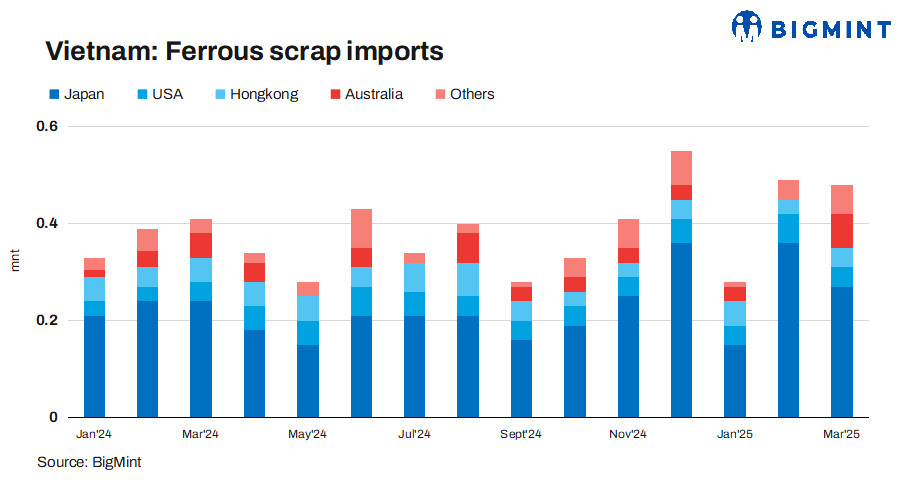

Ferrous scrap imports in March

In March, Japan maintained its position as the top bulk exporter to Vietnam, shipping 274,750 t, reflecting a 14% increase from 240,161 t in March 2024. Australia followed with 72,700 t but saw a 20% decline compared to 47,945 t last year.

The United States exported 44,408 t, marking a slight 5% y-o-y decrease from 46,690 t in March last year.

Meanwhile, Hong Kong experienced a significant surge, with exports rising 85% to 38,454 t, up from 39,359 t.

Vietnam’s crude steel production reached 5.56 mnt in Q1CY’25, up by 0.83% compared to 5.51 mnt recorded in Q1CY’24.

Quarterly price average

US-origin HMS 80:20 deep-sea bulk cargoes CFR Vietnam averaged $351/t in Q1CY’25, down $56/t from $407/t in Q1CY’24.

Japanese H2 scrap CFR Vietnam averaged $323/t in Q1CY’25, down $74/t from $397/t in Q1CY’24.

Factors behind reduced scrap imports in Q1

Vietnam’s ferrous scrap imports stayed low in Q1CY’25 due to weak steel demand, Tet holiday slowdowns, and cautious restocking. Mills operated at reduced rates with sufficient inventories.

US-origin HMS 80:20 moved from $340/t to $363/t CFR within the first quarter, while Japanese H2 stayed around $315/t, later rising to $322/t CFR, which partially reduced trade volumes.

Buyers preferred domestic scrap amid bid-offer gaps and high import costs. In Vietnam’s domestic market, mills in the northern region lowered their purchasing price for 1.5 mm scrap by VND 100-500/kg ($4-20/t) to VND 8,600-8,900/kg ($351-363/t) DDP. Construction in the north was slow due to rain, with rebar and wire rod offers stable and billet prices at VND 11,400-11,650/kg ($447-457/t) DDP.

Market sentiment remained cautious with freight and foreign exchange volatility implied through currency fluctuation-driven bid changes and import cost concerns, plus HRC anti-dumping duties of 19.38-27.83% on Chinese imports from 7 March.

Country wise

Japan: Scrap imports dropped 6.02% to 0.78 mnt in Q1 from 0.83 mnt in Q1CY’24, due to weak demand, sufficient inventories, and limited restocking.

Hong Kong: Scrap imports declined significantly by 36.84% to 0.12 mnt in Q1 from 0.19 mnt in Q1CY’24 because of high prices and preference for domestic scrap over regional supplies.

United States: Scrap imports surged 7.69% to 0.14 mnt in Q1 from 0.13 mnt in Q1CY’24, reflecting higher intake.

Australia: Scrap imports dropped 9.09% to 0.10 mnt in Q1 from 0.11 mnt in Q1CY’24, due to higher freight costs, lower availability of scrap from Australia, and Vietnam’s preference for other markets like Japan and Hong Kong.

Leave a Reply