In Vietnam, imported bulk ferrous scrap offers from the US and Japan remain range-bound amid uncertainty in market trends reflecting passive buying interest amidst prevailing uncertainty, particularly in the downstream steel sector.

Vietnamese mills remained cautious, staying on the sidelines for imported scrap as they await clearer pricing signals amid ongoing uncertainties in the steel market.

Current offers, assessments: BigMint’s weekly assessment of US bulk HMS (80:20) stood at around $382-385/t CFR Vietnam, witnessing a range-bound trend w-o-w. Since the beginning of the year, the assessment has witnessed a decline of $30/t.

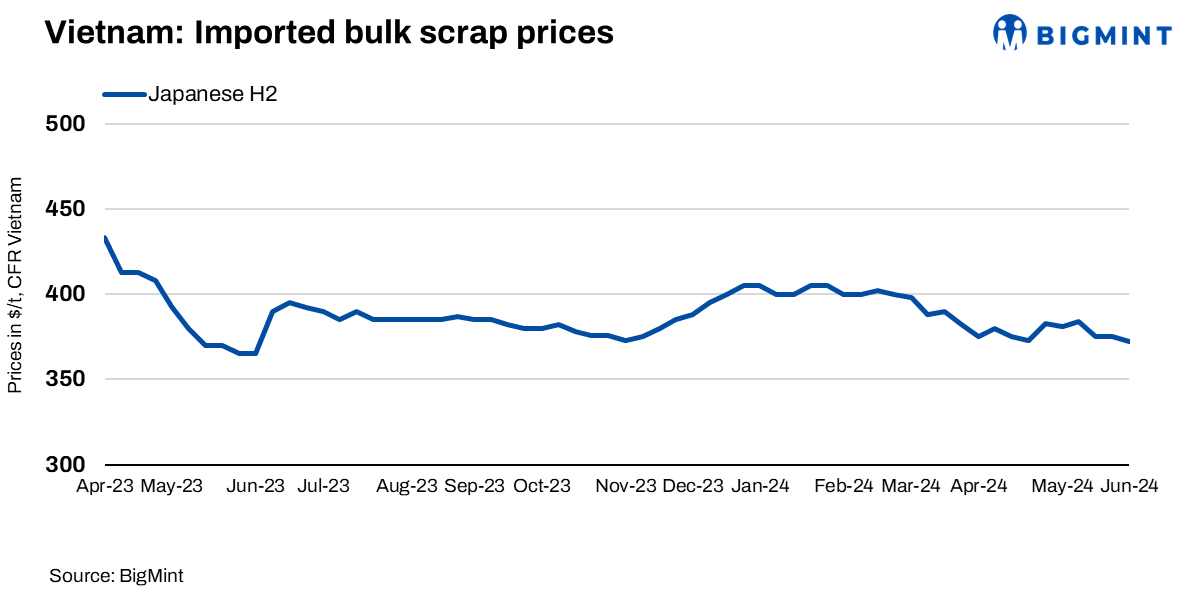

BigMint’s weekly assessment for Japanese H2 scrap was reportedly in the range of $372-374/t CFR Vietnam, largely stable w-o-w as buyer enquiries were still below $365/t and workable levels were $370/t CFR.

- Chinese market impact: The Chinese steel market experienced a downturn this week due to concerns over the sustainability of downstream steel demand. Despite government stimulus efforts aimed at the real estate sector and crude steel production control, competitive offers from Chinese steel products pressured prices downward.

- Vietnamese mills adjust: In response to competitive pressures, a leading Vietnamese mill reduced its hot-rolled coil offer to $565/t CIF Vietnam, down from $595-610/t CIF earlier in May.

- Procurement caution: With limited upside seen in steel prices, Vietnamese mills exercised caution in scrap procurements, according to local traders. Limited trading activity was observed this week, with small volumes of containerised HMS (80:20) changing hands at $350-355/t CFR Vietnam.

Domestic scrap market: Vietnam’s domestic scrap prices experienced a decline in the week ending 30 May attributed to several factors including subdued steel demand, heightened competition between electric arc furnaces (EAFs) and blast furnaces (BFs), and the impending onset of the monsoon season. In contrast, South Korean local scrap prices remained stable albeit amidst limited activity.

Price movements: Domestic Type 1 or H2-equivalent 3-6 mm scrap prices in north Vietnam dropped VND 100/kg ($4/t) to VND 9,500-9,600/kg ($372-$376/t). Southern prices for the same grade also fell by VND 100/kg to VND 8,350-8,650/kg. Market sources attribute the decline to an unsustainable increase in scrap prices in early May, prompting a necessary correction.

Weak steel demand persists in Vietnam, exacerbated by the imminent monsoon season. Blast furnaces hold a cost advantage over electric arc furnaces due to low iron ore and coke prices, leading to diminished competitiveness for EAFs and consequently lower scrap demand. Intense competition from blast furnaces, highlighted by a significant billet sale by a major Vietnamese BF-based mill to both the domestic and seaborne markets, put further pressure on downstream prices.

Outlook: Vietnam’s steel demand is poised to remain subdued as the monsoon season begins, exerting continued downward pressure on domestic scrap prices. This decline underscores a multifaceted environment shaped by weakened steel consumption, intensified competition between blast furnaces and electric arc furnaces, and seasonal factors. Conversely, South Korea’s scrap market is expected to remain stable with limited activity in the near term, as any increase in demand may materialise post-summer.