Vietnamese scrap importers remained inactive during the previous week, opting to focus on procuring local scrap, and this trend underscored Vietnamese mills’ preference for domestic scrap over imported volumes, driven by factors such as convenience and inventory levels.

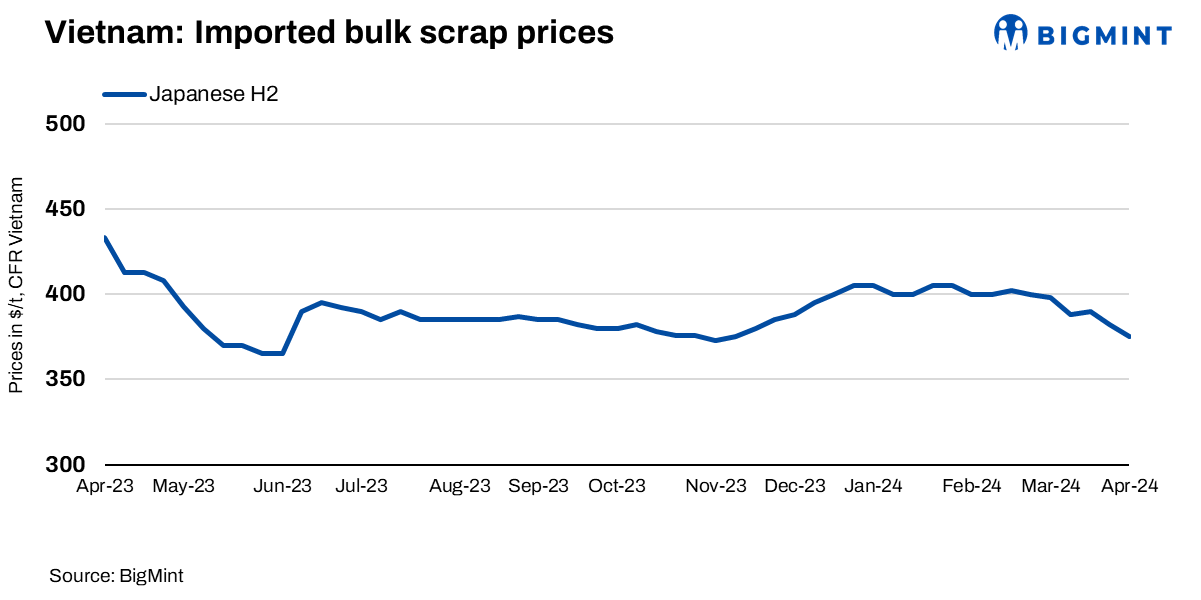

- BigMint’s weekly assessment for Japanese H2 scrap was reportedly in the range of $375-380/t CFR Vietnam, down by $7/t w-o-w from last week’s $382/t, whereas buyers were aiming for $365-368/t CFR Vietnam.

- BigMint’s weekly assessment for US bulk HMS (80:20) stood at a range of $390-392/t CFR Vietnam, which declined by $2/t w-o-w, and offers for Australian HMS were around $380/t CFR.

Regarding specific offers, a few HS offers were heard at $395-400/t CFR Vietnam, although no deals were concluded due to discrepancies in sellers’ and buyers’ expectations. Additionally, H2 offers were observed at $373-378/t CFR Vietnam, while a bid was reported at $364-368/t CFR Vietnam, reflecting thin liquidity in the market.

Market participants explained the challenge of purchasing large volumes of HMS (80:20) containers due to sellers’ reluctance to offload significant cargo. Nevertheless, some traders anticipate potential price increases in the short term, with close monitoring of factors such as iron ore price trends and the situation in Turkiye.

Domestic market: In Vietnam, the domestic scrap market remained relatively stable in the week leading up to 28 March. Prices of type 1 or H2-equivalent 3-6 mm scrap in northern Vietnam hovered around dong 9,000-9,100/kg ($362-366/t), while prices in the southern region remained steady at dong 8,600-8,700/kg ($346-350/t), as reported by mill and trade sources. Despite this stability, Vietnamese mills were observed actively procuring local scrap instead of relying on imported volumes, citing reasons such as competitive pricing and quicker delivery schedules.

As per steelmakers from Vietnam, a few advantages of domestic scrap include its cost-effectiveness, cleanliness, and quicker delivery. However, limited availability posed a challenge. Moreover, industry observers suggested that demand for domestic scrap might correlate with weak overall demand for finished products.

Mills request AD investigations: Vietnam’s leading flat-rolled steel producers, Hoa Phat Group (HPG) and Formosa Ha Tinh Steel Corporation (FHS), have filed a dumping investigation petition with the Ministry of Industry and Trade (MOIT) against carbon steel hot-rolled coils (HRC) imported from China and India. HPG’s general director, Nguyen Viet Thang, expressed concerns over Chinese steel competition, with Vietnam importing 1.8 million tonnes (mnt) from China in January-February, comprising 70% of total imports. However, nine downstream steel manufacturers opposed the investigation, fearing negative impacts on their businesses. HPG and FHS account for 80% of Vietnam’s HRC industry. Critics argued against the investigation, citing minimal dumping margins and positive performance in recent years for HPG and FHS.

Additionally, Hoa Phat Group (HPG) advanced construction at the Dung Quat 2 complex, achieving 50% progress compared to 40% in December 2023. The complex aimed to enhance the production of high-quality hot-rolled coils (HRC), with plans to finalise a 5.5 million-tpy hot strip mill by the end of 2024. Asset commissioning will occur in two stages, commencing from early 2025. The site will include two blast furnaces (2.5-2.8 million tpy each) and a BOF-based melt shop with two slab casters (6 million tpy total). Upon completion, HPG’s crude steel capacity will rise by 5.6 million tpy to approximately 14 million tpy. The project entails a total investment of VND 85,000 billion (around $3.4 billion).

Outside of Vietnam, demand for deep-sea bulk cargoes across South Korea remained muted, influenced by bearish construction and property outlooks. Despite these external factors, the domestic scrap market in Vietnam continued to attract attention, with local mills actively purchasing scrap and closely monitoring market developments.

Outlook: Looking ahead, while some sources suggested that scrap prices may have bottomed out two weeks prior and could be gradually increasing, others advised caution due to lingering uncertainties. Despite this, market participants with sufficient inventory levels are keeping a close watch on developments from the sidelines.