- Japanese scrap offers firm, but bid-offer gap limits trade

- Domestic billets, long steel prices rise on higher scrap costs

Vietnam’s imported scrap prices rose by up to $3/tonne (t) w-o-w, supported by rising offers from the suppliers. However, overall market activity remained subdued due to a slow recovery in construction, delayed government spending, and tardy launch of new infrastructure projects.

Some Japanese suppliers kept their offers firm following the March Kanto tender price hike, though a clear bid-offer gap persisted as Vietnamese mills found the elevated prices difficult to accept in the near term.

CFR assessments

- US-origin HMS 80:20 deep-sea bulk cargoes were assessed at $368/t CFR, up $3/t w-o-w.

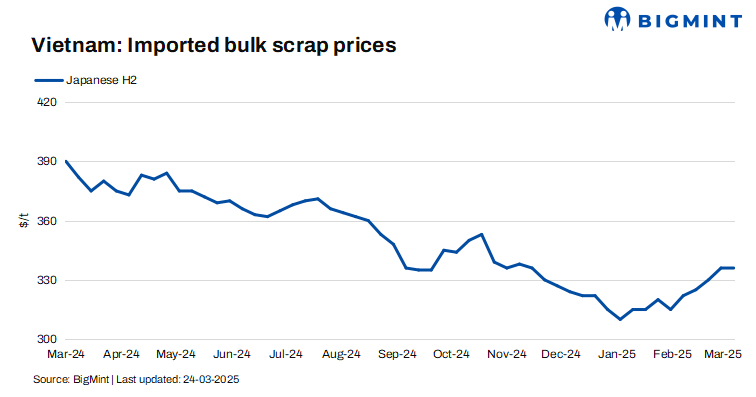

- Japanese H2 scrap remained stable w-o-w at $336/t CFR Vietnam.

Market comments

Indicative offers for Japanese H2 scrap to Vietnam climbed to $330-335/t CFR, largely stable from the previous $330-336/t range, while bids stayed steady at around $326-330/t CFR. US-origin deep-sea scrap offers rose slightly w-o-w to $365-370/t CFR Vietnam.

On the other hand, HS scrap offers from Japan were heard in the range of $368-370/t CFR, up by $3-4/t as compared to last week’s $362-364/t.

Market participants noted that demand for lower-grade scrap remains limited, as EAF-based mills continued to prefer imported billets which are turning out to be more cost-effective.

A Vietnamese mill source commented, “Construction demand usually picks up post-the Lunar New Year, and currently we are seeing a gradual recovery alongside some seasonal improvement.”

Spot liquidity remained thin, with weak interest in deep-sea cargoes. Some mills showed a preference for Japanese-origin scrap, given its competitive pricing compared to US offers.

Domestic steel market scenario

Billet and long steel product prices in the domestic market increased by VND 100-200/kg ($4-8/t) w-o-w, mainly driven by higher scrap input costs.

Vietnam’s ferrous scrap imports jump in Feb’25

Vietnam imported 492,877 t of ferrous scrap in February 2025, up 77% m-o-m and 26% y-o-y. Japan was the top exporter with 364,142 t, followed by the US and Hong Kong. However, January-February’25 imports fell 22% y-o-y to 771,609 t.

Outlook

The market is likely to remain range-bound in the near term, with any potential recovery depending on a pick up in construction activity and faster government project execution.

Leave a Reply