Imported ferrous scrap prices witnessed a downtrend w-o-w as local steelmakers have shown reluctance to restock amid the impending steel production cuts anticipated during the monsoon season. Nevertheless, constraints in scrap supply are expected to drive prices upward in the forthcoming week.

As per steel industry insiders, in Southeast Asia, steel mills typically curtail production during June and July due to the rainy season, resulting in a hesitancy to restock at present. Furthermore, the demand for finished steel has not exhibited significant growth on a w-o-w basis.

However, a trade source mentioned that, despite this, the limited availability of scrap from both the US and Europe could prompt an increase in prices soon. Consequently, mills may proceed with restocking as part of their regular monthly cycle.

According to a mill source, “Most EAF mills are still opting for cheaper domestic scrap for their restocking needs, while others are importing billets or reducing operating capacity.” It is estimated that EAF mills are generally operating at around 30% capacity.

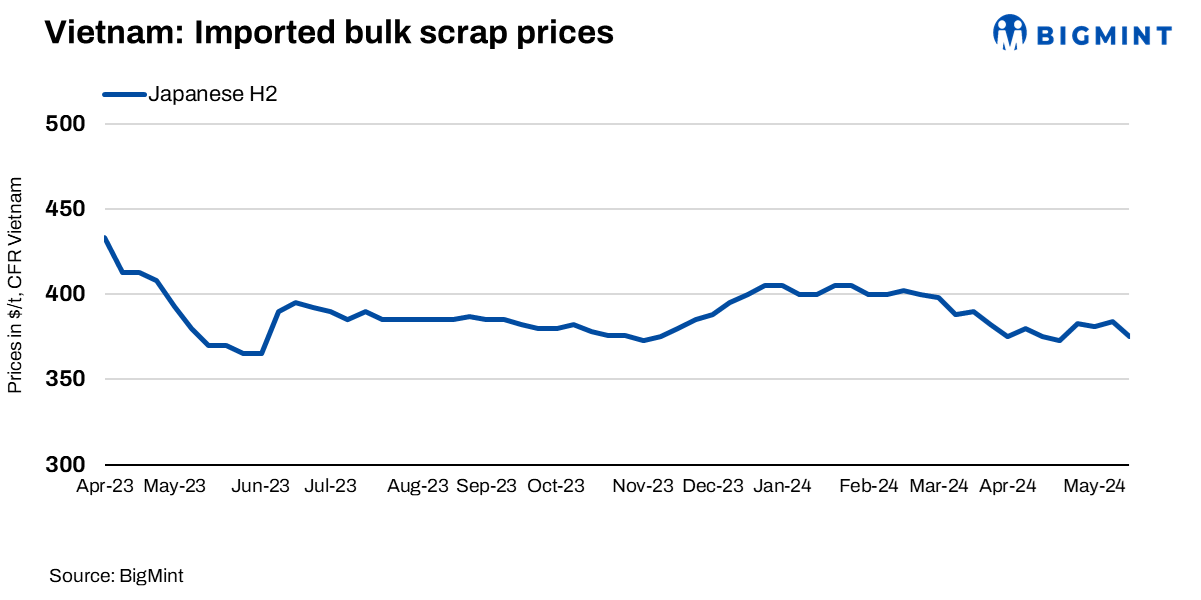

Offers for H2 scrap have softened to $370-380/t CFR Vietnam this week, widening from $375-380/t in the previous week.

Buyers are attempting to push prices down but acknowledge that sellers are unlikely to go below $370/t due to limited supply.

BigMint’s weekly assessment for Japanese H2 scrap was reportedly in the range of $370-375/t CFR Vietnam, down by $8/t w-o-w from last week’s $383/t, whereas buyers were aiming for $366-368/t CFR Vietnam.

BigMint’s weekly assessment for US bulk HMS (80:20) stood at around $385/t CFR Vietnam, which declined by $6/t w-o-w.

Domestic market: Vietnamese steel mills have adjusted scrap purchasing amid a sluggish seaborne market. Northern mills reduced prices for domestic “type 1” or H2-equivalent 3-6 mm scrap by VND 200/kg to VND 9,650-9,700/kg by last weekend and Southern region prices similarly fell by VND 100-200/kg to VND 8,800-9,000/kg.

Southern mill sources noted a shift towards buying induction furnace billets due to pricing factors. Blast furnace materials are closely tied to iron ore and coke prices. In Vietnam, a major northern mill reduced H1 grade scrap prices by VND 200/kg to VND 9,700/kg DDP from May 14, reacting to market shifts post Hyundai Steel’s EAF shutdowns potentially impacting future scrap imports from Japan.

Seaborne market sentiment remains cautious after a brief price surge post-Kanto tender results, with limited buying activity reported.

Outlook: Looking ahead, despite stable offers from the US at $385-390/t CFR Vietnam, there is sparse bidding interest. The market expects continued sensitivity to global steel dynamics, including currency fluctuations impacting scrap prices. Future trends hinge on demand recovery, particularly in key Asian markets, which could influence pricing strategies across Vietnam’s steel sector.